Annaly Capital Management (NLY 0.56%) has an atrocious dividend track record. The mortgage REIT the week officially announced it was reducing its payout again -- as management telegraphed that it would last month -- continuing a steady decline that has been going on for the past decade.

While Annaly still offers a big-time yield, its payout could keep falling. Because of that, there are better options for those seeking to generate passive income. A more promising opportunity for those desiring an outsized yield is its fellow mortgage REIT, Arbor Realty Trust (ABR 1.33%).

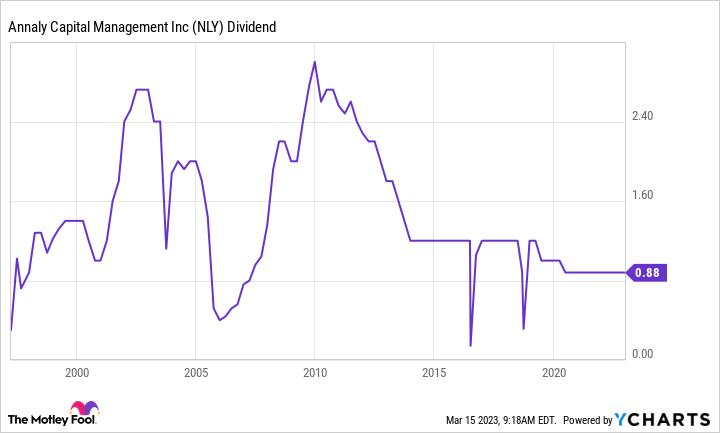

Death by a thousand cuts

Annaly has reset its quarterly dividend payment to $0.65 per share. That's a 26.1% reduction from the prior level of $0.88 per share. While that payout still gives the company an attractive dividend yield of around 12.5% at the recent stock price, it continued the steady downward trend in the dividend.

NLY Dividend data by YCharts.

Annaly's business model is the primary issue weighing on the dividend. It uses shareholder capital and other funding sources to buy residential mortgage-backed securities. It makes money on the spread between its cost of capital (the price it pays for funding) and the interest earned on its mortgage investments. Rising interest rates have cut into that spread, also known as the net interest margin:

|

Metric |

Q3 2022 |

Q4 2022 |

|---|---|---|

|

Average economic cost of funds |

1.54% |

2.11% |

|

Average yield on interest-earning assets |

3.24% |

3.82% |

|

Net interest margin |

1.98% |

1.90% |

Data source: Annaly Capital Management.

Because of that, Annaly is earning less money, which impacts its ability to pay dividends.

That earnings decline has put pressure on the company's stock price. Shares have lost a third of their value over the past year. Because of that, even with the big dividend yield, Annaly's total return over that time frame was negative 21%.

A better alternative

While Annaly's dividend has steadily declined, Arbor Realty's payout has been on the rise:

ABR Dividend data by YCharts.

The company recently broke a streak of 10 consecutive quarterly dividend increases. During that run, it boosted its payout by 33%. Its decade-long streak of annual dividend hikes remains intact, though. Arbor could have easily continued to grow its dividend because it has a huge cushion. The mortgage REIT's dividend payout ratio was a comfortable 67% last quarter, the lowest in the industry. That compares to a 99% payout ratio for Annaly last quarter before it cut its payout. At its current share price, Arbor's dividend has a 14.1% yield -- above Annaly's reset rate.

One big factor driving Arbor's steadily rising dividend is its business model. Whereas Annaly focuses on buying residential mortgage-backed securities, Arbor Realty concentrates on the rental market. It primarily originates and services bridge loans made to multifamily and single-family rental operators. Because of that, it has a more diversified income stream. It earns net interest income on the loans it holds, and also generates servicing and escrow revenue for loans it originates and sells to government-sponsored enterprises such as Fannie Mae, and agencies such as the Federal Housing Administration. Arbor primarily makes variable-rate loans, allowing it to benefit from rising interest rates.

There's no guarantee Arbor will continue growing (or even maintaining) its dividend. If a real estate downturn hits the multifamily sector, it could impact its interest income, affecting its earnings and ability to pay dividends. However, the company's more diversified business model, focus on originating variable rate loans, and low payout ratio put it in a better position to succeed over the long term. It has certainly done that over the last 10 years. Arbor has produced a total return of more than 250% for shareholders (13.6% annualized) compared to a negative 1% total return from Annaly.

Heading in different directions

Annaly's dividend has steadily drifted lower over the last decade due to the impact interest rate changes have on its income. Arbor's payout has headed in the opposite direction because its business model is less sensitive to interest rates. That makes it a better option for investors seeking a big-time dividend yield backed by real estate debt.