One of the hottest stocks of the COVID-19 pandemic was Opendoor Technologies (OPEN +4.09%). The real estate technology platform went public through a special purpose acquisition vehicle (SPAC) with a lot of hype around disrupting the buying and selling process in residential real estate. Since then, shares are down 97.5% from all-time highs. The stock is down 43% already in 2025.

And yet, in the last month, Opendoor stock has begun a comeback and is up 60% from the lows. Does this make the fallen angel a once-in-a-lifetime buy for investors today?

Image source: Getty Images.

A new homebuying model

Opendoor's business strategy is to offer all-cash buys for people selling their homes, speeding up the selling process and skipping the traditional layers of a residential real estate transaction. It then takes the inventory on its balance sheet and turns around and sells the home to another buyer. By speeding up the process, Opendoor is able to buy homes at a slight discount to the market price and then sell them for a small profit.

This is known as the home buying and selling spread, which is how Opendoor generates a profit on a home sale transaction. It used venture capital funding, the SPAC, and debt to fundraise for home buys, scaling across many cities in the United States. As it scaled, it aimed to achieve operating leverage across this small spread between its purchases and sales of homes.

NASDAQ: OPEN

Key Data Points

One problem remained: intelligently buying homes that were not going to fall in price. This was easier said than done. When the home-buying bubble during COVID-19 burst when mortgage rates began to rise in 2022, Opendoor was left with with homes that were depreciating in value on its balance sheet, leading to a weakening spread on home purchases. The stock market reacted negatively to this downturn and hasn't recovered since.

Low margins and debt financing

After this rough patch, Opendoor has emerged as a much smaller company, buying less than 4,000 homes every quarter but one since 2022 compared to 15,000 at the peak in the September quarter of 2021.

Another factor that presented a headwind to transactions is the frozen housing market. Home affordability is at an all-time low, which is pricing out a lot of potential homebuyers from making purchases. Existing home sales are down to 4 million a year in the United States compared to 6 million in 2021, which is a reduction in the addressable market for Opendoor to purchase homes.

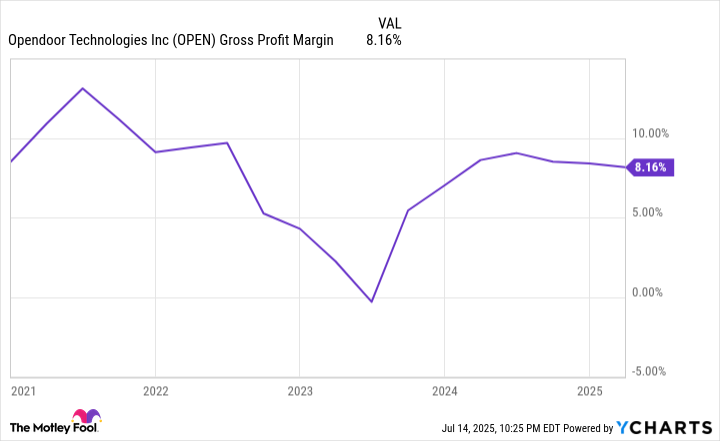

If homebuying activity reverses, Opendoor may see a slight tailwind to its business. However, this will not solve all of its issues. Gross margins are low -- 8% in the last 12 months -- which gives Opendoor a slim spread to cover its overhead costs and generate a profit. It finances a lot of its home purchases with debt, which adds interest costs that eat up a lot of its gross margins.

It is no surprise then to see Opendoor with a net income of negative $368 million over the last 12 months. The company has never generated a profit, not even during the COVID-19 pandemic boom.

OPEN Gross Profit Margin data by YCharts

Should you buy Opendoor stock?

At a market cap of $656 million, Opendoor looks like a potential cheap stock for a turnaround play, generating revenue of $5 billion over the last 12 months. Its stock price is around $1, another variable that might lead you to think it is a cheap buy.

None of these factors matter. Opendoor's business has extremely low margins, which is why the stock is valued at such a low multiple of its trailing revenue. It has to finance its growth with debt, which will lead to ballooning interest expenses if it starts to aggressively purchase homes again. The company has never proven it can generate a profit.

A stock that collapses 98% is not something you want to buy the dip on. Usually it collapses for a reason -- because it has a shaky business model with a chance of leading to bankruptcy. Avoid buying Opendoor stock right now, it is not a turnaround play you want in your portfolio.