Nvidia (NVDA 0.32%) has been the top artificial intelligence (AI) stock to own for some time now, but with its latest rise, many investors are concerned that Nvidia's stock is too expensive to buy more shares at the current price. While I understand the hesitation, I think there is a compelling argument that Nvidia isn't expensive when you take a longer view than just a single year.

If you can commit to owning Nvidia stock for three to five years, I think there's a good reason to buy the stock right now. However, if you're only looking at a single year, the stock may appear somewhat pricey.

Image source: Getty Images.

Data center expansion will continue to be a massive source of growth

Nvidia is the global leader in graphics processing units (GPUs), and it has established this position through superior hardware and unmatched software that allow users to optimize GPUs for various workloads. One estimate pegs Nvidia's data center market share for GPUs at 90%, which underscores just how widely used Nvidia's products are.

GPUs aren't just popular for AI workloads; they're used whenever an arduous computing task is involved. Whether it's drug discovery, cryptocurrency mining, engineering simulations, or their original purpose, gaming graphics, GPUs excel at the task because of their ability to process multiple calculations in parallel. Combine that with the ability to connect GPUs in clusters, and their computing power can be quickly amplified.

NASDAQ: NVDA

Key Data Points

As more data centers are built, the demand for GPUs is expected to rise, which will likely benefit Nvidia's stock over the long term. For 2025, the AI hyperscalers all announced record capital expenditures, with most of the funds going toward data center construction. While this is impressive, the records are likely to be shattered again in 2026, as data center construction spans multiple years. This supports a third-party projection that Nvidia cited during its 2025 GTC conference, stating that 2024 global data center capital expenditures totaled $400 billion but are expected to rise to $1 trillion by 2028.

Should that occur, Nvidia's stock has plenty of room to run, as it captures a large portion of that spending. In the company's fiscal-year 2025 (which encompasses most of 2024), its data center revenue totaled $115 billion, which means Nvidia captures nearly 30% of total data center spending. If it can maintain that market share, it has the potential to generate $300 billion from data centers alone, provided the projection comes true.

That's a significant upside from today's totals, making today's stock price appear less expensive than it initially seems.

Nvidia's stock appears expensive, but so do many others in the market

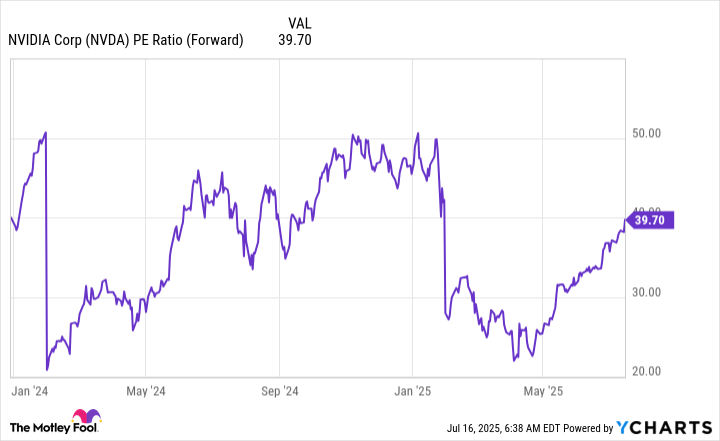

Currently, Nvidia's stock trades at about 40 times forward earnings.

NVDA PE Ratio (Forward) data by YCharts

That's historically quite expensive, but few companies have been able to sustainably grow as quickly as Nvidia. For Q2, Nvidia expects 50% revenue growth, which is far more than the majority of companies in the market.

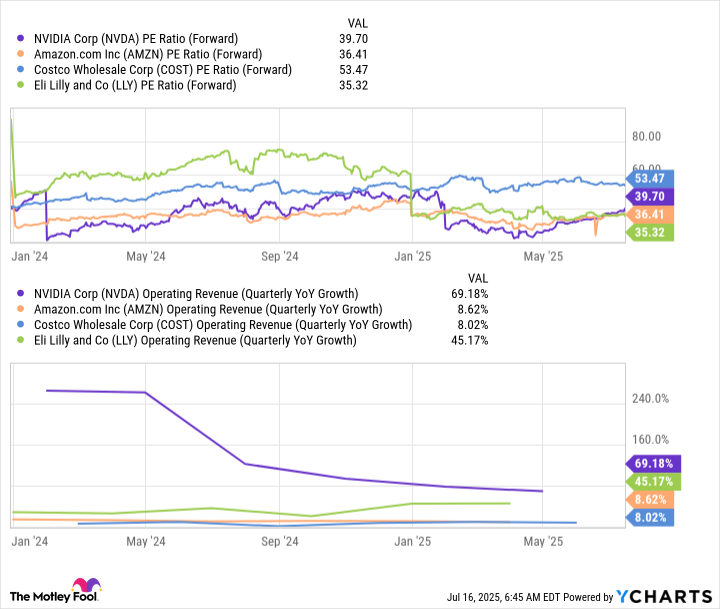

Furthermore, if you're going to call Nvidia expensive, then there are countless other stocks investors must be cautious with. Stocks like Amazon (AMZN +0.11%) (36 times forward earnings), Eli Lilly (LLY +0.50%) (35 times forward earnings), and Costco Wholesale (COST +2.03%) (53 times forward earnings) are just as expensive as Nvidia, yet don't have near the growth rate or upside.

NVDA PE Ratio (Forward) data by YCharts

I think it's safe to say that the broader market is rather expensive as a whole, but with how rapidly Nvidia is growing and how bright its long-term prospects are, I think investors are still safe to pick up shares here, as long as they have the mindset that they're holding for three to five years. If you can keep that time frame in mind, Nvidia is still a compelling investment.