Artificial intelligence (AI) remains a top investment theme in the market and shows no signs of slowing down. While some investors may be wary of the AI trend, the reality is that companies are investing vast resources in this technology, and many are reaping the benefits.

One of the biggest areas where investors will continue to see amazing growth is in data centers. Data centers are proliferating across the country to house the computing hardware used to process AI, and it is primarily in these buildouts that companies generate profits from AI.

Three stocks that I like in this space are Nvidia (NVDA +2.06%), Taiwan Semiconductor Manufacturing (TSM +5.74%), and Digital Realty Trust (DLR +1.64%). I believe this trio is a no-brainer buy right now, and investors should consider these stocks first if they want to invest in the AI sector.

Image source: Getty Images.

All three companies are critical for AI

Nvidia's graphics processing units (GPUs) powered the AI arms race from the beginning. GPUs possess a key ability to process multiple calculations in parallel, making them ideal for complex workloads, such as AI. Additionally, they can be connected in clusters to further amplify this effect. Some companies have gone as far as connecting 100,000 GPUs, creating an ultimate computing machine focused on AI.

NASDAQ: NVDA

Key Data Points

Nvidia holds an impressive 90% market share in data centers and continually innovates to maintain its leadership position. This dominance has been evident in Nvidia's results, with revenue rising 69% year over year in Q1 and expected to increase at a 50% rate in the second quarter, although Nvidia's management has been known to exceed internal expectations regularly.

Nvidia can't fabricate chips itself, so it designs them and sends the production to Taiwan Semiconductor. This fabless design approach has become the leading technique among many major tech companies, with others, such as Apple and Broadcom, adopting the same mindset. These are all Taiwan Semiconductor customers, alongside countless others.

Taiwan Semiconductor has risen to become the world's top chip manufacturer, thanks to its best-in-class yields and continuous innovation. Although its 3nm (nanometer) chip node has been a huge hit among its client base, it's scheduled to launch a 2nm node later this year and a 1.6nm node in 2026. These two innovations will bring significant advancements in power consumption, which could help reduce the energy demand of data centers.

Digital Realty Trust is a unique approach to AI. It's a real estate investment trust (REIT) that's focused on building data centers and then renting them out to various clients. It's also well positioned to capture the massive data center buildout trend, as it has the land to build an additional 4,300 megawatts of capacity on top of the 2,800 megawatts it's already built.

Digital Realty expects both AI and non-AI workloads to increase data center demand by 350% between 2025 and 2030, making owning a stock like Digital Realty a savvy investment. Furthermore, it pays investors a handsome 2.9% dividend yield, which makes it a welcome change from typical tech stocks (although Nvidia and Taiwan Semiconductor also pay a small dividend).

NYSE: DLR

Key Data Points

This trio has a compelling investment case, but why are they smart buys now?

The stocks may not be cheap, but they're not expensive for the market opportunity

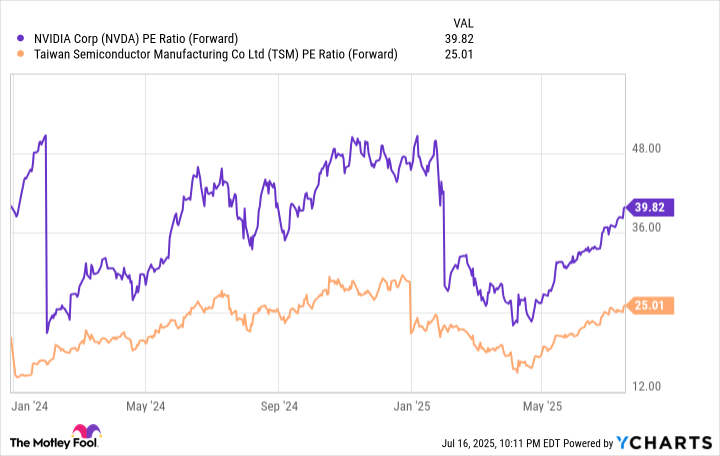

Both Nvidia and Taiwan Semiconductor have seen their shares recover sharply since the market bottomed in April, causing their valuations to rise substantially.

NVDA PE Ratio (Forward) data by YCharts

However, both stocks are still below the levels they traded at in the second half of 2024, making them not particularly expensive from a historical forward price-to-earnings (P/E) ratio standpoint. One important caveat with this valuation metric is that it only looks one year ahead. Both stocks are expected to experience multiple years of strong growth, and if that proves to be true, there is even more upside for these two.

Because Digital Realty is a REIT that incurs significant depreciation costs, using a metric like the P/E ratio is a flawed approach. Instead, REIT investors use a metric known as funds from operations (FFO) to value stocks. Digital Realty expects about $7.10 in core FFO per share for 2025, which would value the stock at 24 times forward FFO. That's not the cheapest REIT around, but for the market opportunity Digital Realty is tackling, I think it's a worthy price to pay.

All three of these stocks are excellent AI investments and make for solid stocks to buy right now.