Taiwan Semiconductor (TSM +0.34%) is currently valued at around $1.25 trillion, making it the ninth-largest company in the world. Normally, investors don't expect these large companies to produce outstanding growth, as the larger a business gets, the more difficult it becomes for it to grow. However, TSMC has monster growth projections on the table, as well as a new technology that could drive shares much higher.

Rising from today's $1.25 trillion valuation to a $3 trillion valuation would require a 140% return. However, management believes there's plenty of growth in store for Taiwan Semiconductor to meet this threshold.

Image source: Getty Images.

Taiwan Semiconductor's new chip technologies will push its stock higher

Taiwan Semiconductor is the world's leading semiconductor foundry. Its business strategy is to offer its clients best-in-class chip production technologies, and not compete against them. This business model has worked out incredibly well for TSMC, and its customer list ranges from Nvidia to Apple to Tesla. If you have a cutting-edge technology device, it's likely that it contains a chip manufactured by Taiwan Semiconductor.

One of the reasons TSMC established itself at the top of its industry is its dedication to driving the next greatest innovation. In recent chip launches, Taiwan Semiconductor outpaced its peers by offering the most advanced technology available first. That doesn't seem to be changing, as it has some promising technology in the pipeline.

NYSE: TSM

Key Data Points

Later this year, Taiwan Semiconductor is expected to launch its N2 chip node, indicating 2nm (nanometer) spacing between traces. The pre-launch demand for the N2 node exceeds that of the 3nm and 5nm offerings. This is big news for Taiwan Semiconductor, as the improvements this generation offers are substantial enough that many companies are designing their products around this new technology.

The biggest improvement the N2 offers its users is energy efficiency. This has implications for the smartphone industry, with longer-lasting phones being more desirable. Additionally, the energy consumption of AI computing devices to run generative AI prompts is becoming a front-and-center topic. When N2 chips are configured at the same processing speed as 3nm chips, they consume 25% to 30% less energy. That's a massive improvement, and the energy savings from these chips may warrant upgrading to new computing units.

Beyond its N2 launch, the company is slated to bring its A16 chip (1.6nm) to market in 2026. The A16 is expected to achieve an energy consumption improvement of 15% to 20% on top of the N2. A14 is the next technology TSMC is working on, but it won't reach production until 2028, so there's quite a bit of time between now and the scheduled launch date.

Still, these technologies will drive further growth for TSMC and potentially propel it to a $3 trillion valuation mark in a fairly short timeframe.

Taiwan Semi's management projects monster growth over the next five years

Management projects that, starting with 2025, its revenue will rise at nearly a 20% compound annual growth rate (CAGR) over the next five years. However, management has exceeded its own guidance every quarter this year, so it shouldn't surprise investors to see this projection increase.

Should TSMC grow its revenue at a 20% CAGR, that would indicate nearly 150% growth, above the threshold needed for TSMC to rise to a $3 trillion valuation point. Additionally, Taiwan Semiconductor isn't an expensive stock, at least compared to the broader market.

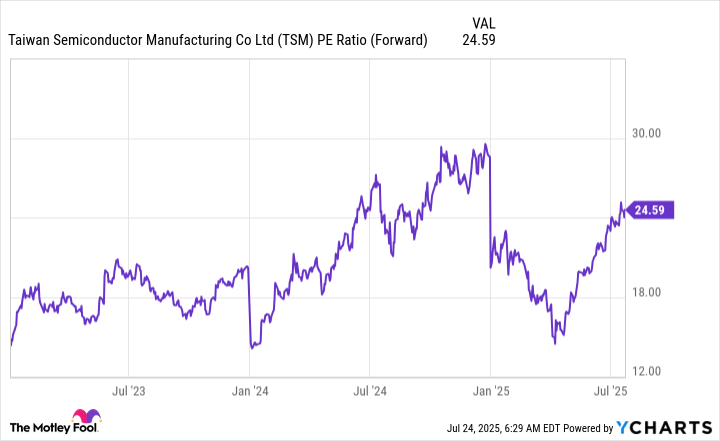

TSM PE Ratio (Forward) data by YCharts.

At 24.6 times forward earnings, TSMC is only slightly more expensive than the S&P 500, which trades at 23.8 times forward earnings.

With a reasonable price tag and a fairly clear growth strategy, I think Taiwan Semiconductor is about as no-brainer a stock pick as it gets in today's market.