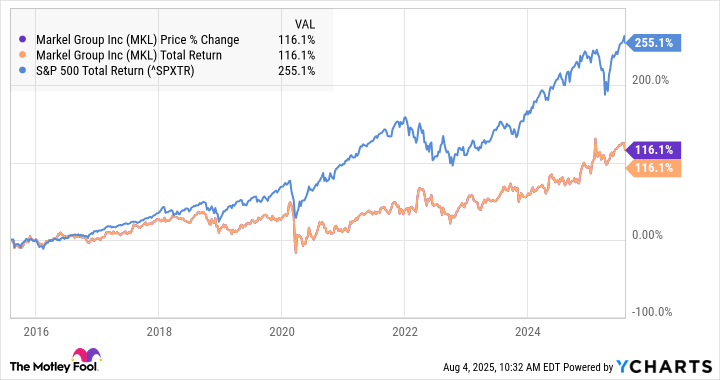

Over the past decade, Markel (MKL 0.79%) has delivered a 116% return for investors, or about 8.1% annualized. That isn't exactly terrible performance, but when you consider that the S&P 500 has produced a 255% total return over the same period, or 13.5% annually, it is less than impressive.

It's especially disappointing to investors, because Markel had established such a strong track record in its earlier days. In fact, even after the lackluster performance of the past decade, Markel has outperformed the S&P by more than 1,000 percentage points over the past 30 years.

Will Markel turn things around?

Markel is often referred to as a "baby Berkshire" for the similarities between its business model and that of Berkshire Hathaway (BRK.A 1.06%) (BRK.B 0.81%). Like Berkshire, Markel uses its insurance float to invest in a portfolio of common stocks, as well as in entire businesses. But given its sluggish performance, is the investment thesis still intact?

Image source: Getty Images.

Fortunately, the company's leadership is well aware of the problem and recently announced plans to unlock its intrinsic value, which management conservatively estimates at about $2,600 per share, about 35% above the current stock price.

Along with its year-end 2024 earnings report, Markel announced that it's conducting a thorough review of its business. Its goals are to optimize the insurance business, which quite frankly hasn't been as profitable as it should be, as well as to simplify the business structure and allocate capital as effectively as possible. If Markel can successfully execute on its plan, it could certainly create an inflection point in the stock that makes the next decade far more lucrative for shareholders.