Artificial intelligence (AI) stocks come in all shapes and sizes, which is what makes AI such an attractive investment field. There are several ways to profit from this buildout, but one of my favorites is through the chipmakers.

At the top of the list is Taiwan Semiconductor Manufacturing (TSM +2.31%), the world's leading contract chip manufacturer. TSMC, as it's known, dominates this space and looks to be getting stronger. Despite hitting a 52-week high, I still think it's undervalued and has room to run. It's one of my top stocks to buy now, and if you don't already own shares, it's not too late to pick some up.

Image source: Getty Images.

Taiwan Semiconductor is a critical supplier to many AI companies

Taiwan Semiconductor is a chip fabricator, but it doesn't sell its products on the open market. Instead, it acts as a foundry for fabless chip companies like Nvidia, Advanced Micro Devices, and Apple. Because of its customer base, it has massive exposure to the artificial intelligence buildout. AI hyperscalers are racing to construct data centers filled with massive processing power to train and run AI models. The chips within these data centers have to come from somewhere, and TSMC is the source of most of these chips.

While some may be concerned about TSMC's location, management is working to diversify its footprint and has plans to spend $165 billion to increase U.S. capacity. This will allow products like Nvidia's GPUs to have chips completely sourced from the U.S., which secures supply chains and sidesteps tariffs.

Taiwan Semiconductor has gone all-in on increasing chip production with heightened demand, and that will pay off for the company in the long term. It is the top partner of choice for many AI companies, and this trend is far from over.

However, the stock has risen 220% since the AI arms race began in 2023. So how does it have room for more?

Taiwan Semiconductor's growth and valuation make the stock look cheap

At the start of 2025, management gave a bold prediction that AI-related revenue would grow at a 45% compound annual growth rate (CAGR) over the next five years, with overall revenue increasing at a 20% CAGR. That's market-crushing growth, yet TSMC's stock trades at about the same valuation as the broader market.

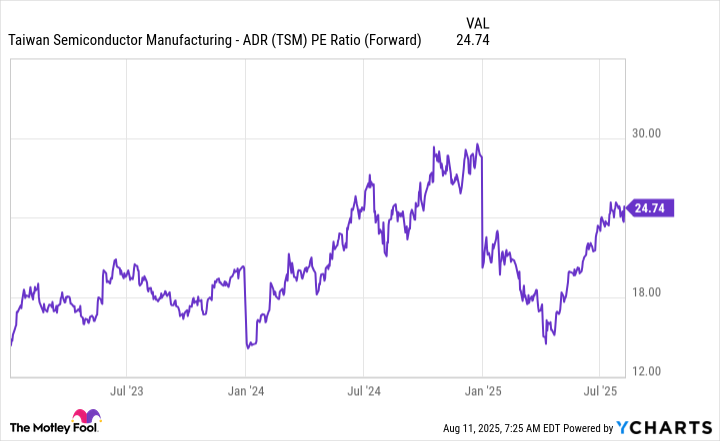

TSM PE Ratio (Forward) data by YCharts

At 24.7 times forward earnings, it's only slightly more expensive than the S&P 500, which trades for 23.7 times forward earnings.

However, with TSMC's faster-than-average growth rate, the two securities being valued at the same level suggests that it is still undervalued.

As a result, I think it's worth buying shares right now, as this mismatch may not stick around for long. TSMC is the second-fastest growing company that has a $1 trillion valuation or greater (besides Nvidia). However, compared to some of its big tech peers, it doesn't receive the same valuation.

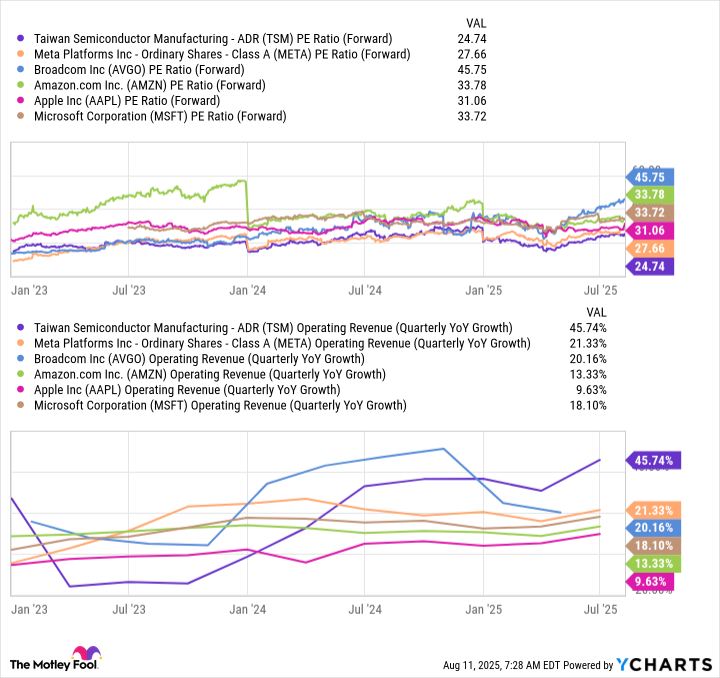

TSM PE Ratio (Forward) data by YCharts

Despite topping the revenue growth rate charts by a wide margin, it lags in the valuation department. As a result, TSMC's multiple could expand over the next few years or maintain its current price and have its market-crushing growth lead the way.

Regardless, I think TSMC is primed to continue rising on the back of increased chip demand, which will result in a winning investment.