The cruise industry is an interesting one from a stock market perspective. During the pandemic, these companies had to take on a huge amount of debt and sell equity, diluting their shareholders, to raise cash and ride out COVID-19.

But in the post-pandemic world, the cruise industry has been incredibly strong, initially due to "revenge" travel and the need for experiences. But even after inflation and interest rates spiked in 2022, the cruise industry held up very well, showing perhaps a longer-term growth trend. Cruising is also a more efficient form of travel than staying in hotels, which have gotten more expensive.

Despite the strong recent results, these companies are still digging themselves out of their debt holes, which could lead to further upside as they pay down debt and de-lever their balance sheets.

Two leaders in the space are Carnival (CCL 0.91%), the oldest publicly traded cruise stock, having been on the stock market since 1987, and Viking Holdings (VIK 0.98%), the newest public cruise stock, having just had its initial public offering (IPO) in June.

Which is the better buy today for those looking to play the continued recovery of cruise stocks? The experienced veteran or new kid on the block?

NYSE: CCL

Key Data Points

Both companies are hitting it out of the park

There appears to be great strength across the cruise industry, with both companies posting terrific recent numbers. Off of a very strong 2024, Carnival grew revenue 9.5% last quarter, but with a massive inflection in profitability as adjusted (non-GAAP) earnings per share more than tripled.

Not only that, Carnival CEO Josh Weinstein noted that Carnival had already achieved its 2026 SEA Change operational and financial targets it had set for itself two years ago, 18 months ahead of schedule. Those targets included operational goals around sustainability, the important profit-centered metrics of earnings before interest, taxes, depreciation, and amortization (EBITDA) per available lower berth day (ALBD), and return on invested capital (ROIC).

As of the second quarter of 2025, EBITDA per ALBD had grown 52%, and ROIC had more than doubled to 12.5% over just the past two years. That's really impressive, owing to Carnival's pricing actions, capacity restraint, and a focus on costs.

But Carnival isn't the only cruise company reporting impressive results. In its first quarter, Viking impressed investors with revenue growth of 24.9% on the back of a 7.1% increase in net yields and a 14.9% increase in capacity. Net yields are essentially the direct profits per customer, equaling net revenues per available passenger cruise day minus the costs of travel commissions, transportation, and onboard costs.

Viking's management also forecasted good times ahead, noting that it was basically sold out for 2025, and 37% of capacity was already booked for 2026 -- ahead of where the company was with forward bookings at this point last year.

Image source: Getty Images.

But Viking's debt picture looks much better than Carnival's

So, both companies appear to be on a good path operationally. But for the foreseeable future, these companies will be devoting most or all of their profits to paying down their COVID-era debt.

On that front, Viking appears to be in a much better position. Today, its debt sits at 2.0 times its trailing EBITDA as of March 31, while Carnival's debt-to-EBITDA ratio sat at a higher 3.7 times as of May 31.

It's not entirely clear why Viking came out of the pandemic with a lower debt load than Carnival. It could be that since Viking was a private company before 2020, it hadn't taken on the leverage to repurchase stock as aggressively as Carnival had done as a public company in the years leading up to the pandemic.

It could also have something to do with each company's business model. Carnival is largely in the business of ocean cruises all over the world across a number of brands. Viking is largely engaged in river cruises, mostly in Europe, and focuses on older cruise enthusiasts, who tend to be less economically sensitive. Viking also has ocean cruises, but those ships totaled only about 12% of its capacity last quarter.

But Viking's valuation has already taken off

On the back of strong results, both stocks have done well in recent months. However, Viking has done extraordinarily well, with the stock having appreciated 150% from its June $24 IPO price to $60 as of this writing. Carnival has also had a strong recent run, with the stock up nearly 23% on the year.

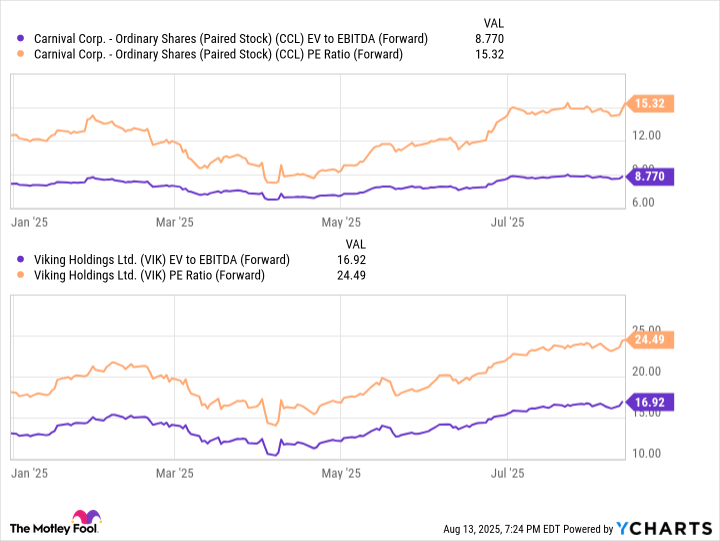

Still, Viking's run has caused its valuation to soar much higher than Carnival's, with a forward price-to-earnings (P/E) ratio and forward enterprise value-to-EBITDA (EV-to-EBITDA) ratio of 24.5 and 16.9, respectively. Meanwhile, Carnival is much cheaper, trading at a forward P/E ratio of 15.3. And while Carnival does sport a higher debt load, even its forward EV-to-EBITDA ratio, which accounts for debt, is much lower, at 8.8 times this year's EBITDA estimates.

CCL EV to EBITDA (Forward) data by YCharts. EV = enterprise value. EBITDA = earnings before interest, taxes, depreciation, and amortization. PE Ratio = price-to-earnings ratio.

Getting what you pay for

As it stands now, it appears that investors are paying fairly for what they're getting. Viking's less-risky business model and lower debt load have led to a much higher valuation. And since it's in a better balance sheet position, it's also able to expand capacity faster than Carnival, as evidenced by last quarter's growth rates.

Meanwhile, Carnival looks cheaper on all metrics, significantly so, but it also has a debt load nearly twice that of Viking's relative to each company's EBITDA. And because it has to pay down its debt, management isn't expanding capacity as fast as it probably would otherwise.

Thus, each stock could still be a buy if you believe in the continued strength of the cruise industry. Viking may be the better play for growth-oriented investors, with its near-25% growth rate and relatively lower risk. But for value investors, Carnival may be the better play here, as its lower valuation could get a rerating as the company continues to pay down its sizable COVID-era debt load, which would de-risk its story.