Figma (FIG 0.69%) -- a recent initial public offering (IPO) stock -- was hot when it debuted on July 31. Its share price more than tripled that day from an initial $33 per share. After reaching a 52-week high of $142.92 in August, the shares have dropped back down to Earth in September.

This sudden share price reversal could signal an opportunity to pick up shares. Or it could mean investors should stay away from Figma. After all, something caused the sell-off. Discovering if now is a good time to buy Figma shares requires unpacking what's going on with the company today.

Here's a look into Figma and the factors affecting its stock.

Image source: Getty Images.

Figma's financial performance

Figma's share price dropped on the heels of its first earnings report as a public company on Sept. 3. Its results for the second quarter reveal clues as to why investors abruptly soured on the stock.

On the surface, Figma appears to have done well in Q2. It delivered impressive 41% year-over-year revenue growth to $249.6 million. In addition, the company's cost of revenue dropped year over year, which enabled Q2 gross profit to grow to $221.8 million compared to $137.6 million in 2024. This is a positive sign, since it means Figma is managing expenses effectively, and keeping more of the income it produces.

Its Q2 balance sheet was strong as well. Assets totaled $2 billion, including cash and equivalents of $621.6 million. Total liabilities were $607.4 million, but of that, $433.1 million was deferred revenue, which represents up-front customer payments that will be recognized as sales once services are delivered.

NYSE: FIG

Key Data Points

Why Figma stock fell

Despite the positives, one area that seemed to disappoint investors was Figma's outlook. The company expects Q3 sales to come in between $263 million and $265 million, up from $198.6 million in 2024. This represents 33% year-over-year growth at the midpoint, which is a drop from Q2's 41% gain.

Investors were disenchanted with this, since it suggests a sales slowdown. On top of the Q3 estimate, the company's full-year revenue forecast of $1 billion represented 37% year-over-year growth, further contributing to investor concerns, especially in light of Figma stock's elevated valuation.

Another factor affecting the stock is that insiders and employees can begin selling shares with the expiration of their lock-up period. This means more stock will be available for sale, putting downward pressure on the price.

To buy or not to buy Figma stock

The plunge in share price doesn't reflect any fundamental issues with Figma's business. The company's products are proving popular. The number of customers spending at least $10,000 in annual recurring revenue (ARR) reached nearly 12,000 in Q2, up from 9,000 in the prior year. Q2 customers with more than $100,000 in ARR rose to over 1,000 from 787 in 2024.

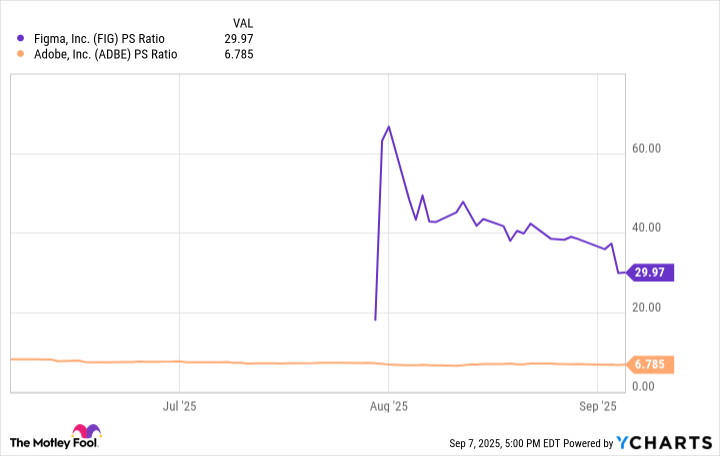

At this point, the biggest issue appears to be Figma's share price valuation. Comparing its price-to-sales (P/S) ratio, which measures how much investors are willing to pay for every dollar of revenue generated over the trailing 12 months, to digital design software competitor Adobe helps to illustrate the situation.

Data by YCharts.

As the chart shows, although Figma's P/S multiple has dropped from sky-high levels after its IPO, it's still quite lofty compared to Adobe. Figma is growing faster than its larger rival, which adds to its valuation, but a P/S ratio of about 30 is still high, indicating Figma stock remains pricey.

As a result, the prudent approach is to wait for the stock to drop further before deciding to buy. Because this is Figma's first earnings report, you may want to observe the company's performance over a few quarters while waiting for its shares to reach a reasonable valuation.