The stock market is soaring, and the online meme-trading armies are back in style. One stock leading the charge is Opendoor Technologies (OPEN -3.87%), a real estate platform that went public in 2020. The stock was down over 95% from all-time highs before large investors and individual traders began purchasing shares en masse last quarter.

Opendoor is now up around 500% year to date and more than 10 times its lows in June. However, with a market cap of $7 billion and a price of $9.50 as of Sept. 15, the stock is still below its debut price after merging with a special purpose acquisition company (SPAC).

Does that make it a buy below $10?

A new CEO and cost-cutting

After the stock price surged, the company's board of directors began looking for changes to make at the struggling real estate platform. It ousted CEO Carrie Wheeler in August and announced a search for a new executive to lead the company's turnaround.

Now, it has found its successor: Kaz Nejatian, previously the chief operating officer (COO) of successful software company Shopify, giving him a strong track record in building technology businesses. Shopify has been a huge winner for long-term shareholders and has taken a ton of market share in e-commerce spending and digital payments.

Nejatian will soon begin at Opendoor, with plans to get rid of its work-from-home strategy to spice up innovation. He wants to use a similar playbook that worked well at Shopify.

Along with the new CEO, the company is bringing back Keith Rabois and Eric Wu to the board of directors. Both of them founded the company.

Rabois said on CNBC that Opendoor will look to cut costs by eliminating employee bloat, which he says is holding back the company from innovating. Time will tell what the exact changes will be, but expect major changes in the months to come.

Image source: Getty Images.

Can Opendoor return to growth and profitability?

Cost cuts will be necessary for Opendoor, which is highly unprofitable today. Last quarter, revenue was $1.6 billion. As a scaled-up buyer and seller of residential real estate, it has low gross profit margins (it only earns the spread between its homes' purchase and selling prices). Last quarter, its gross profit was just $128 million, or a margin of 8.2%.

From this gross profit, management spent $86 million on marketing, $28 million on general overhead, and $21 million on product development. Along with $36 million in interest expense last quarter, it posted a $29 million loss before considering taxes.

In fact, over a 12-month period, Opendoor has never generated positive net income.

In the short run, the company will cut costs to start earning a profit. In the long run, it aims to return to growth by expanding outside of the capital-intensive homebuying business, which could include title services, mortgages, and working with real estate agents. It wants to make home transactions better for both buyers and sellers, although it is unclear what the specific strategy is today.

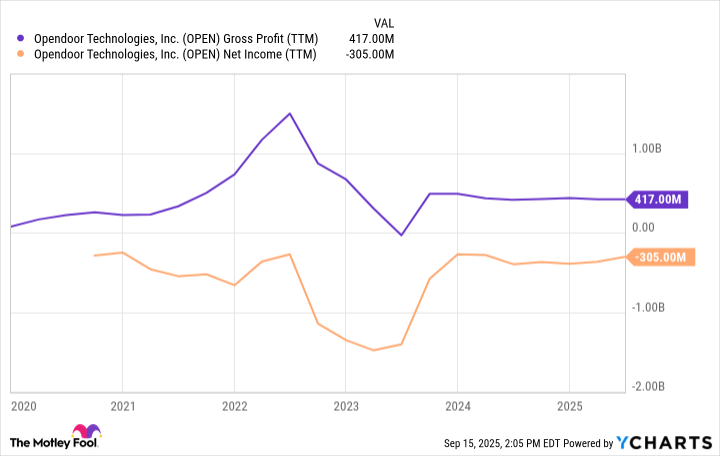

As a potential investor, keep track of Opendoor's growth in gross profit as well as its ability to turn gross profit into bottom-line net income. That will tell the true story over the long term.

OPEN Gross Profit (TTM) data by YCharts; TTM = trailing 12 months.

Opendoor's valuation at under $10 a share

With a blistering rise in the stock comes increased expectations for profit growth. At a market cap of $7 billion, expectations are sky high.

It is impossible to value Opendoor on a price-to-earnings ratio (P/E) due to the fact it loses money. But we can look at its trailing gross profit figure of $417 million, which gives the stock a price-to-gross-profit (P/GP) of close to 20. This is a premium valuation for a fast-growing company, let alone one in the midst of a turnaround.

It may have just hired a sharp CEO with plans to cut costs, but that does not automatically make the stock a buy. Expectations are high, and the company is competing with larger players such as Zillow that dominate the homebuying space. A steep valuation and poor historical performance mean that investors should avoid buying Opendoor stock right now.