BigBear.ai (BBAI 7.23%) is one of the more popular small-cap artificial intelligence (AI) stocks on the market, and with a market cap of just $2.6 billion, it has a ton of room to grow.

The dream for any AI stock is to duplicate the performance of Palantir (PLTR 2.95%), which has delivered impressive revenue growth and outstanding stock price appreciation. Palantir now has a market cap topping $400 billion, so for BigBear.ai to surpass it would require incredible returns over the next decade.

Are such gains feasible, or is BigBear.ai too far behind to catch up?

Image source: Getty Images.

The U.S. military is becoming a key customer for BigBear.ai

BigBear.ai and Palantir operate in similar industries. Palantir sells AI-powered data analytics software that it originally developed to meet the needs of government clients. BigBear.ai also makes software that is primarily intended for government use, although it provides custom solutions rather than a software platform.

BigBear.ai's biggest contract is with the U.S. Army, developing its Global Force Information Management system. This system will ensure that the U.S. Army is "properly manned, equipped, trained, and resourced" for whatever the current mission is.

Recently, BigBear.ai announced that it will be assisting the U.S. Navy to improve coordination and decision-making capabilities during a major multinational training exercise. This could open up a pathway for the company to win another military contract, which it desperately needs.

BigBear.ai's margins leave a lot to be desired

Unlike most of its AI peers, BigBear.ai isn't growing. In Q2, its revenue declined 18% to $32.5 million. This is an obvious red flag. If the company can't put up respectable growth in the golden age of AI spending, when will it be able to?

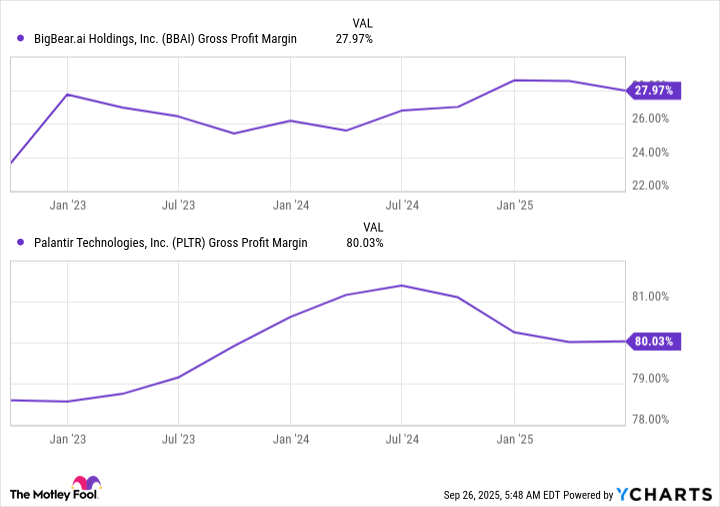

Furthermore, because it isn't developing a software platform to base other products on, it must develop custom solutions for each client. This expensive process eats into BigBear.ai's gross margin. Most software companies (like Palantir) have gross margins in the 70% to 90% range. BigBear.ai's is in the 20% to 30% range. That limits the upside for its profits for the foreseeable future.

BBAI Gross Profit Margin data by YCharts.

That second red flag makes it even more difficult to compare BigBear.ai to a successful company like Palantir.

But even ignoring both of the current conditions, what would it take for BigBear.ai to reach Palantir's valuation level in a decade? Assuming that Palantir's price stays flat (which isn't a terrible assumption based on how expensive its valuation is already), BigBear.ai would need to achieve a compound annual growth rate of 166% for 10 years to reach its market cap.

That's a pretty unrealistic goal. Indeed, I doubt that BigBear.ai will ever reach Palantir's current size. I also think there are far better AI investment options available, as BigBear.ai's growth rate and low margins are cause for concern. If BigBear.ai can't grow its revenue base when interest in AI is this hot, there's no reason to think it will be able to deliver acceptable growth levels when demand moderates.