If you bought Nvidia (NVDA 0.88%) at the start of 2023, you're very happy. The stock is up more than 1,100% since then, for a phenomenal return in a short time frame. However, after a run like that, investors would be forgiven if they thought they were too late to buy.

This thought process is called price anchoring, where your mind anchors itself to what the stock price was, making you think that you've missed the boat. However, the more appropriate (albeit difficult) way to think is to picture where it is going. If you can do that with Nvidia stock, it's clear that it has a huge growth runway, and that even after its monstrous run, it still has plenty of steam to keep going.

Management believes data center capital expenditures will rise dramatically

Nvidia makes graphics processing units (GPUs), which are the semiconductors of choice for training and processing artificial intelligence (AI) models. GPUs can perform multiple calculations in parallel, making them ideal for workloads that require vast computing power, like AI. While there are a handful of competitors in this space, Nvidia is by far the preferred option and has a 90% market share in the data center realm.

Because its market share is so dominant and demand currently is greater than supply, the company's biggest customers are working closely with it to ensure that there are enough GPUs available for them to outfit their data centers when construction is complete. So, when management makes a bold projection about the direction of the industry, investors should listen.

This year, Nvidia expects data center capital expenditures to reach $600 billion globally. By 2030, that figure is expected to reach $3 trillion to $4 trillion. That's monstrous growth, and if that pans out, the company clearly has more room to run.

While I think huge projections like that should be met with some amount of skepticism, the reality is that the chipmaker has more information than anyone else in the industry because of its close ties with its customers. Even if the forecasts are wrong on the total amount, they are likely correct on the general direction, which makes Nvidia an intriguing stock to consider buying now, even after its strong run.

The stock is a no-brainer buy if management is correct

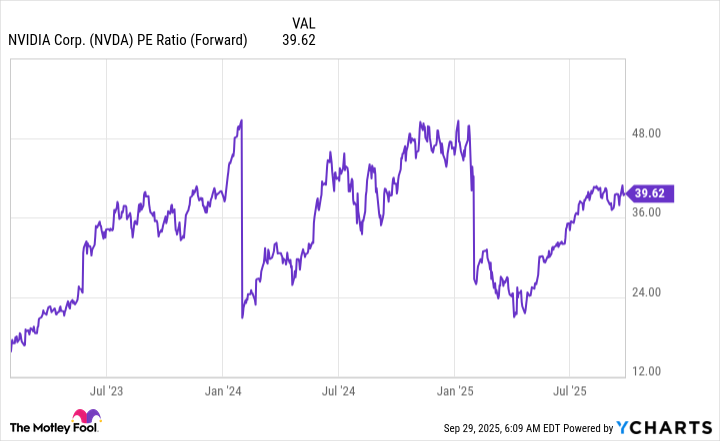

At its current price tag, the stock doesn't look cheap. At 40 times forward earnings, it's at the high end of the range it has traded at over the past three years. However, it's roughly in line with its level at about this time last year, so it is staying pretty true to its historical data.

NVDA PE Ratio (Forward) data by YCharts; PE = price to earnings.

Should Nvidia's market projection pan out, this will actually be a fairly cheap price to pay, since it could result in revenue more than tripling over the next five years.

However, if AI spending ends up nowhere near where management projects, this could prove to be too high a price to pay, making it a poor investment. Considering all of the recent spending announcements and Nvidia's track record of success, I'd say there's a low probability of this happening.

The market tends to double every seven years, and if Nvidia's revenue growth is correlated to its stock growth, this makes it a worthy investment now because it will likely outperform the market if the demand turns out to be as strong as management projects it will be.

There is a ton of money flowing into AI infrastructure, and Nvidia grabs the largest slice of the pie of anyone operating in this space. This makes it a no-brainer buy right now, and investors should be happy to have paid today's price years down the road.