Occidental Petroleum (OXY 0.86%), commonly known as Oxy, fell 7.3% on Oct. 2 in response to news that it is selling its petrochemical division, OxyChem, to Warren Buffett-led Berkshire Hathaway (BRK.A 0.30%) (BRK.B +0.00%) for $9.7 billion. Here's why the deal is better for Berkshire than Oxy, and if the energy stock is worth buying on the dip.

Image source: Getty Images.

Oxy is improving its financial health

Oxy is mainly an exploration and production (E&P) company operating in the upstream segment of the oil and gas value chain. But unlike some pure-play E&Ps, Oxy also had a massive downstream division called OxyChem, which makes chemicals for several industries -- from construction to water treatment, healthcare, and consumer goods.

OxyChem generated $428 million in pre-tax income in the first half of 2025 and $1.1 billion in 2024. The business has very high margins, making it a stable cash cow that helps offset some of the volatility of Oxy's E&P business. So Oxy's move to sell OxyChem to Berkshire for less than 9 times 2024 earnings may come as a surprise.

NYSE: OXY

Key Data Points

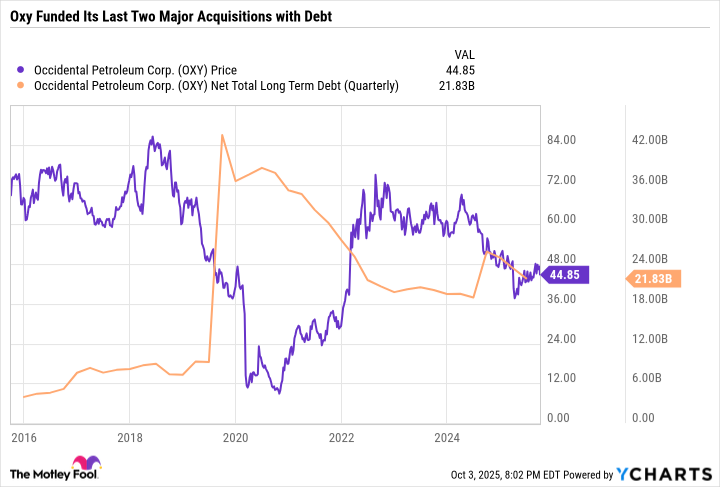

The decision likely comes from Oxy's goal to improve its balance sheet. With the help of Berkshire, Oxy bought Anadarko Petroleum in 2019 -- levering up its balance sheet in the process. The pandemic and subsequent decline in oil and gas prices crushed Oxy's margins and pushed the stock price below $10 a share. Oxy was bleeding cash and undergoing serious financial stress.

But then, the industry recovered and Oxy was able to hold on long enough to begin raking in the free cash flow (FCF) in 2022 and 2023. Oxy paid down debt. But its insatiable risk appetite couldn't be quelled.

On Aug. 1, 2024, it completed its acquisition of CrownRock L.P. for $12 billion -- expanding operations in the Permian Basin. Oxy planned to sell $4.5 billion to $6 billion of assets within 18 months of the deal to pay down debt and ensure its balance sheet didn't become overleveraged. But few expected that meant unloading OxyChem.

A good deal for Berkshire Hathaway

As you can see in the following chart, Oxy's debt spiked after its acquisition of Anadarko in 2019, and then again after CrownRock in 2024.

It's important to note that the CrownRock deal was magnitudes smaller than the Anadarko acquisition. And Oxy has been reducing its net debt over the past year since the deal was completed. So history isn't repeating itself, but it is rhyming in the sense that Oxy is betting big on the Permian Basin, even if it means letting go of OxyChem.

Investors may be wondering why Oxy would buy CrownRock at the expense of selling OxyChem and why Berkshire would buy OxyChem outright instead of just investing more in Oxy directly. After all, Occidental Petroleum is Berkshire's seventh-largest public equity holding -- with Berkshire owning 26.9% of Oxy's common stock. The answer is most likely that Oxy wants to become more of a pure-play Permian E&P, and Berkshire is looking for steady cash cows outside of its exposure to oil and gas.

Not only does Berkshire have a lot of Oxy stock, but it also owns 6% of Chevron, which is its fifth-largest holding. Buffett has repeatedly stated during Berkshire's annual meetings that he doesn't intend to acquire Oxy outright because he likes what the management team is doing. Still, Berkshire's decision to buy OxyChem rather than more Oxy showcases a clear preference toward the company's chemical business over its upstream assets, which is a bit of a red flag for Oxy shareholders.

Oxy is taking a hit from lower oil prices

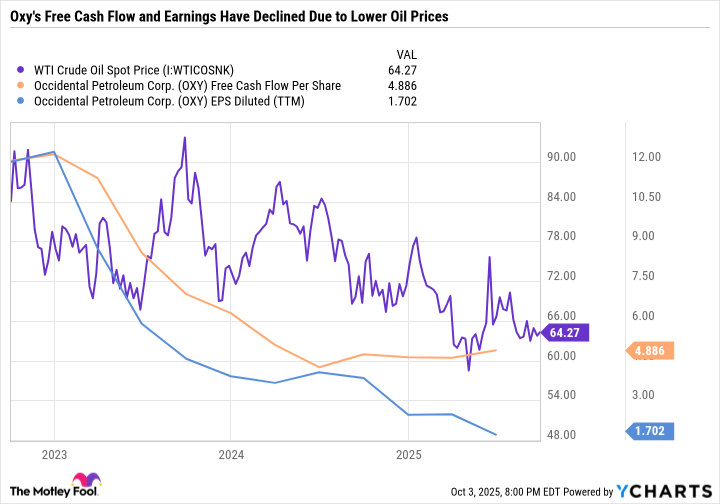

Oxy is well-positioned to rake in the FCF when oil prices are high, which is why it did so well during the pandemic-era recovery. Although it can still break even at low prices, its profitability declines substantially in the current pricing dynamic, which is characterized by West Texas Intermediate crude prices in the low- to mid-$60-per-barrel range.

As you can see in the following chart, Oxy's earnings and FCF have fallen over the last three years as oil prices have come down.

WTI Crude Oil Spot Price data by YCharts

Despite the decline, Oxy is still a great value. It sports a price-to-FCF ratio of just 9.2, a price-to-earnings (P/E) ratio of 26.4, and a forward P/E of 19, which is remarkable considering how much its earnings have fallen in recent years.

Betting big on U.S. oil and gas

If Oxy's decision to double down on the Permian pays off, the stock will become too cheap to ignore. And even now, Oxy is a good value for investors who are optimistic about oil prices maintaining current levels or ticking higher. However, Berkshire got the better end of the OxyChem deal. And Oxy will become less diversified without the steady FCF from OxyChem.

The good news is that Oxy's balance sheet will be in impeccable shape. So if there is a downturn in oil and gas, Oxy should be able to ride it out, even as a pure-play E&P. Oxy is a good buy for investors seeking a pure-play Permian E&P. Folks looking for less risky ways to bet on oil and gas may want to consider integrated oil and gas majors like ExxonMobil and Chevron or a safer, more diversified E&P like ConocoPhillips.