Serve Robotics (SERV +1.75%) develops autonomous last-mile logistics solutions. It has a major deal with Uber Technologies (UBER +0.56%) that will see thousands of its latest robots deployed into the Uber Eats food delivery network. But this is more than just a commercial partnership, because Uber is also one of Serve's largest shareholders.

Uber acquired a company called Postmates in 2020, and in 2021, it spun Postmates' robotics division out into a new company that became Serve Robotics. Serve is still relatively small with a market capitalization of just $890 million, but at the time of this writing, its stock has soared by 67% over the past year alone.

Serve has identified an enormous addressable market for its delivery robots, so should investors join Uber and buy the stock?

Image source: Getty Images.

A potential $450 billion opportunity

Existing last-mile logistics networks are quite inefficient, because they rely on cars with human drivers to deliver relatively small commercial loads from restaurants and retail stores. Serve is betting those workloads will increasingly shift to autonomous robots and drones, creating a potential $450 billion opportunity by 2030.

Serve's latest Gen 3 robots have achieved Level 4 autonomy, meaning they can safely operate on sidewalks in designated areas without any human intervention. This makes them ideal for transporting small food orders, which is why 2,500 restaurants in five U.S. cities have used them to make 100,000 deliveries since 2022.

The Gen 3 robots use Nvidia's Jetson Orin platform, which includes all of the computing hardware and artificial intelligence (AI) software they need to operate autonomously. Having such a powerful technology partner will help Serve scale as quickly as possible, which is key to bringing costs down to management's target of just $1 per delivery. At that point, using robots will be substantially cheaper than using human drivers.

Serve has a contract with Uber Eats to deploy 2,000 robots across Los Angeles, Miami, Dallas, Atlanta, and Chicago before the end of 2025. The company rolled out its 1,000th robot on Oct. 6, meaning its capacity will double in just the next few months.

But it won't stop there, because last week Serve announced a new multiyear deal with DoorDash, which operates the largest food delivery network in the U.S. The two companies are yet to provide firm numbers, so it's unclear how many more robots Serve will have to deploy.

NASDAQ: SERV

Key Data Points

Scaling a robotics business is not cheap

Despite its status as a publicly traded company, Serve is still very much a start-up. Its revenue tends to be quite lumpy, which is typical when a product is in the early stages of commercialization. The company brought in just $642,000 in revenue during the second quarter of 2025 (ended June 30), which is a tiny amount relative to its $890 million market cap.

But Serve's business could scale extremely quickly. Management thinks the company will generate up to $80 million in annual revenue once all 2,000 Gen 3 robots are up and running, which bodes well for 2026. Wall Street predicts Serve will generate $3.6 million in total revenue this year (according to Yahoo! Finance), so $80 million would be a monumental jump.

But so far, the road to commercialization has been paved with substantial losses. Serve lost $33.7 million on a generally accepted accounting principles (GAAP) basis during the first half of 2025, so it's on track to exceed its 2024 loss of $39.2 million by a very wide margin. The company spent $16 million on research and development alone during the first half of this year, so based on its minuscule revenues, its losses are no surprise.

Serve had $183 million in cash on hand as of June 30, and it raised a further $100 million from investors in October, so it has enough cushion to sustain its losses for the next few years (assuming they don't materially increase). However, if the company doesn't chart a pathway to profitability by then, it might have to raise even more money, which will dilute existing shareholders.

As a result, there is a lot riding on the successful commercialization of Serve's 2,000 Gen 3 robots.

Serve stock trades at a sky-high valuation, but is it a buy?

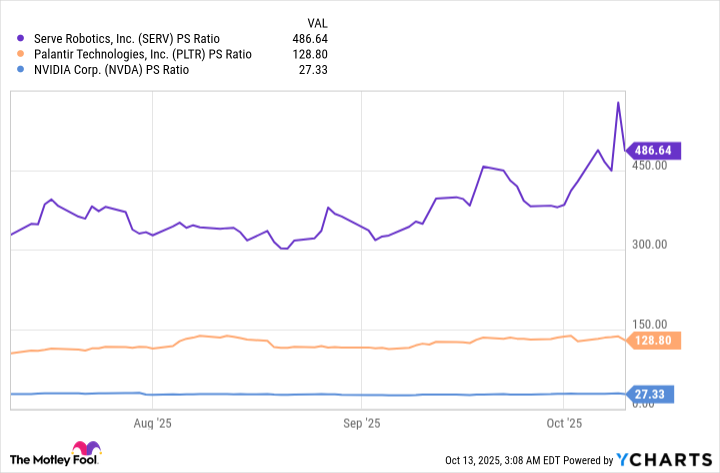

Serve stock is extremely expensive right now. Its price-to-sales (P/S) ratio is a mind-boggling 486, making it substantially more expensive than any other major AI stock. Palantir Technologies, which also trades at a sky-high valuation, looks cheap by comparison because its P/S ratio is 128. For some further perspective, Nvidia stock has a P/S ratio of just 27.

SERV PS Ratio data by YCharts

With that said, if we assume Serve will generate around $80 million in revenue next year, its forward P/S ratio is just 11. In other words, it almost looks like a bargain.

But investors can't always rely on management's guidance, especially in this case because it assumes a perfectly smooth transition to commercialization for the Gen 3 robot. As with any new product, there will probably be bumps in the road, and we simply don't know if it will scale successfully.

As a result, investors might be better off waiting a few more quarters to see if the rollout of the robots actually translates into as much tangible revenue as management expects. If it doesn't, Serve stock could suffer a sharp correction because of its current valuation.