Artificial intelligence (AI) infrastructure stocks have continued to soar this year as investors have flocked to companies that are benefiting from the rapid expansion of data center capacity.

CoreWeave (CRWV +2.65%) and Nebius Group are a couple of such stocks that have registered stunning gains so far in 2025. That's not surprising, as their customers have been doling out multibillion-dollar contracts to purchase dedicated AI cloud computing capacity from them.

So, it is easy to see how shares of Applied Digital (APLD 1.66%) have delivered similarly eye-popping gains of almost 350% in 2025 as of this writing. Yet this data center specialist has the potential to fly even higher over the long run.

Image source: Getty Images.

AI will supercharge Applied Digital's business

Applied Digital designs, builds, and operates data centers that are optimized for high-performance computing and for running AI workloads. Surging demand for such capacity explains why the company's revenue shot up by a stunning 84% year over year to $64.2 million in its fiscal 2026 first quarter, which ended on Aug. 31. On the earnings call for the period, management pointed out that Applied Materials received $26.3 million in revenue from the tenant fit-out of its data center capacity leased by CoreWeave.

NASDAQ: APLD

Key Data Points

Tenant fit-out refers to the process of customizing and building a data center facility to suit the tenant's requirements. And management also noted on the call that while the revenue it generates from fitting out data centers for tenants is a "one-time low-margin business, approximately mid-single digits, it is strategically important."

That's because once the fit-outs are complete, Applied Digital starts booking lease revenue from those data centers. The good part is that Applied Digital already has a solid revenue pipeline thanks to the potential lease revenue that it is likely to generate in the long run. On the earnings conference call, management said that it had expanded its partnership with CoreWeave to cover the full 400 megawatts (MW) of capacity that it is currently constructing at its Polaris Forge One complex.

The total size of its data center leasing contract with CoreWeave now stands at a whopping $11 billion for the next 15 years. It is worth noting that CoreWeave has asked Applied Digital to perform the fit-out of the first 100 MW of the 400 MW Polaris Forge One campus. It won't be surprising if CoreWeave expands that fit-out request to take the remainder of the capacity, considering that it has a massive revenue backlog.

Moreover, Applied Digital estimates that it can scale up the size of that campus to more than 1 gigawatt (GW) from 2028 onward. Meanwhile, it has started construction on a new data center campus dubbed Polaris Forge Two that will have an initial capacity of 300 MW. Applied Digital estimates that it can scale up that campus to more than 1 GW as well. In fact, Applied Digital has an active development pipeline of 4 GW of data center capacity.

The company expects to start construction on new projects in the next six to 12 months. There is a good chance that all that capacity could be quickly snatched up by cloud hyperscalers or neocloud providers such as CoreWeave, because demand for it is outpacing supply. And the imbalance could get sharper from here: According to a forecast from the Boston Consulting Group, the U.S. will have a shortage of 45 GW in data center capacity by 2030.

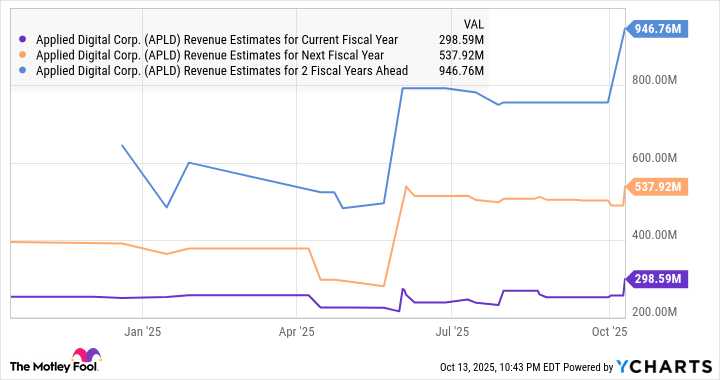

As a result, Applied Digital should witness strong growth in revenue from both tenant fit-outs and leasing revenue in the long run. Not surprisingly, analysts expect Applied Digital's business to grow at outstanding rates.

APLD Revenue Estimates for Current Fiscal Year data by YCharts.

But is the stock worth buying anymore?

Investors may be wondering if there is any more upside left for Applied Digital stock, considering that it has already jumped significantly this year. It certainly doesn't look cheap, trading at 37 times sales.

But investors should note that its rapid revenue growth and the size of its pipeline help justify its valuation. The company operates in a market where there is a clear gap between demand and supply, and one that's likely to persist in the coming years. Ideally, Applied Digital's focus on adding data center capacity should pave the way for it to achieve years of solid growth.

So investors would do well to look past this AI stock's currently lofty valuation, as it could outperform Wall Street's expectations thanks to the catalysts discussed above.