With the S&P 500 (^GSPC 0.73%) hovering around an all-time high, investors may be more interested in growth stocks with market-beating potential than high-yield dividend stocks. But long-term investors know that the true value of dividend stocks is the passive income they provide, no matter what the market is doing.

Building a passive income stream is especially useful for investors looking to supplement income in retirement or for folks incorporating passive income into their financial planning.

Here's why Clorox (CLX +2.92%) is an excellent high-yield dividend stock to buy for investors looking to power their passive income stream.

Image source: Getty Images.

A long overdue recovery

Clorox is in prove-it mode as investors wait to see if its turnaround is the real deal or riddled with overpromises.

Sales and earnings soared during the onset of the COVID-19 pandemic. But Clorox overestimated demand, which crushed its margins. Then came a cyberattack in 2023 that disrupted Clorox's operations and led to product shortages.

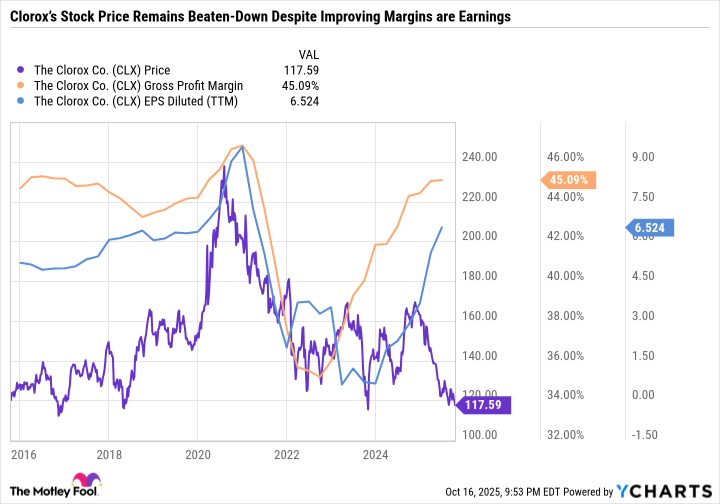

As you can see in the chart, it took years for Clorox to recover. And investors lost patience, as Clorox's stock price is now below pre-pandemic levels.

Far from business as usual

Clorox will report its first-quarter fiscal year 2026 results on Nov. 3. Guidance for the fiscal year is weak, as organic sales are expected to decrease between 5% and 9%. Adjusted earnings per share are expected to decline between 18% and 23%. That doesn't sound like a successful turnaround at first glance. But Clorox has already pegged fiscal 2026 as a transition year due to the rollout of its new enterprise resource planning (ERP) system.

Clorox expects the new system to improve internal operations, supply chain, finance, and data management. It will upgrade a decades-old system to a cloud-based platform, which should lower costs and improve efficiency.

But in the near term, the transition is taking a sledgehammer to Clorox's results. To prepare for the transition, Clorox shipped extra product to retailers, which artificially boosted fiscal 2025 sales. With additional inventory, retailers won't need to buy as much from Clorox, which will allow it to execute its ERP transition without letting customers down. A smooth transition is especially important given that Clorox left its retailers hanging during its cyberattack.

Clorox's fiscal 2026 guidance points to a big down year because the ERP transition threw a wrench in retailer order volumes. In its guidance, Clorox said that it expects about an $0.85 to $0.95 impact on adjusted EPS related to the ERP transition. In addition to the impact on retailer inventories, the ERP transition and associated digital technologies are expected to cost $570 million to $580 million in total.

A good time to turn around

Clorox's results are messy because of these one-time investments. But they could pay off long-term, as Clorox clearly needed a tune-up after its blunders during the pandemic and cyberattack.

Pulling forward demand in fiscal 2025 due to the ERP transition may work out in Clorox's favor. The consumer staples sector as a whole is getting hit hard by inflationary pressures and consumers dealing with higher costs of living. The stock prices of leading household and personal care companies, from Procter & Gamble to Colgate-Palmolive, are also hovering around 52-week lows. So now is a great time for Clorox to make long-term investments, even if they disrupt operations.

Clorox has fallen far enough

Clorox is a great buy for investors who don't mind waiting years for its turnaround to play out. Warren Buffett famously said that "You pay a very high price in the stock market for a cheery consensus." But the opposite is true, too. The consensus on Clorox is anything but cheery due to the company's ERP transition and broader industry challenges with consumer demand and economic uncertainty. Long-term investors are getting the chance to buy Clorox for around its lowest level in a decade, which could end up being a bargain if Clorox returns to growth in fiscal 2027.

What's more, Clorox pays an ultra-high-quality dividend. It has increased its payout for 48 consecutive years -- having raised its quarterly payout to $1.24 or $4.96 per year in July. Clorox's languishing stock price, paired with consistent dividend increases, has pushed its yield up to 4.2% -- which is its highest in a decade. The high dividend yield provides a worthwhile incentive for investors to hold the stock while the turnaround plays out.

Time to load up on this passive income powerhouse

Clorox hasn't had a normal year since before the pandemic. And investors are tired of dealing with uncertainty, overpromising, and underdelivering. But fast-forward a year or two, and Clorox could look a lot more appealing. The company has an excellent portfolio of brands, including its flagship Clorox, Burt's Bees, Pine-Sol, Hidden Valley, Brita, and Kingsford.

Clorox doesn't have to acquire new brands. It just needs to get the most out of what it already has. If operational and supply chain improvements accomplish that goal, then Clorox's investment thesis could improve in the coming years.

All told, Clorox is a great contrarian pick for patient investors to buy in October.