I own Eaton (ETN +3.09%) stock, and I have no intention of selling it. I'm going to follow Warren Buffett's advice and hold for the long term to benefit from the company's growth over time. But would I buy it now? The answer is likely no. Here's why.

What does Eaton do?

Eaton is a more than 100-year-old industrial giant. With a market cap of more than $140 billion, it is one of the 10 largest publicly traded industrial companies on the planet. When it started out, it focused on the auto sector, making truck axles. Today, however, after decades of shifting its business with the world around it, Eaton's primary focus is on products that manage electricity.

Image source: Getty Images.

Its last big change came in 2012, when Eaton acquired Cooper Industries. Today, its electrical business sales in the Americas provide 47% of total revenue, and the segment's sales in the rest of the world account for another 25% of the top line. The company still makes auto products, and it also has a sizable aerospace business, but the clear driver of its results is its electricity-focused business.

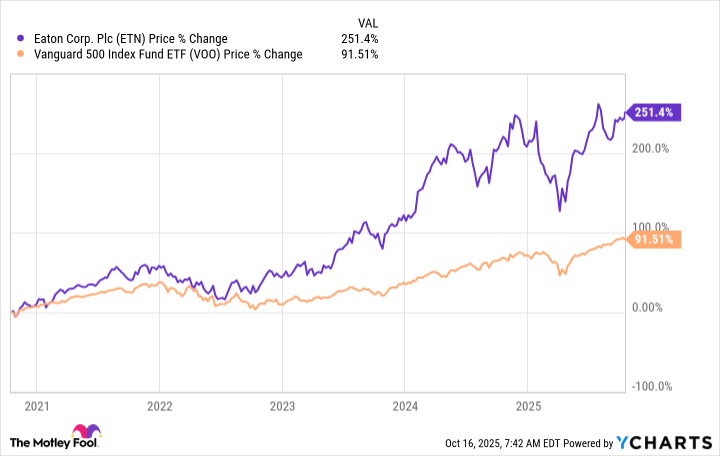

The industrial giant looks like it has positioned itself well to take advantage of the ongoing global trend toward electrification, which is why I'm not going to sell my shares, despite a material increase in their value. In fact, over the past five years alone, Eaton's stock price is up more than 250%, handily outdistancing the more than 90% gain of the S&P 500.

Data by YCharts.

The opportunity has passed

That said, I'm not interested in buying any more shares of Eaton at current price levels. Earlier in 2025, when the stock tumbled by roughly 30%, I might have had a different view. But now that it has recovered and is flirting with all-time highs, I think its valuation has become too lofty.

To put some numbers on that, Eaton's price-to-sales ratio is currently around 5.8 compared to its five-year average of 3.7. The price-to-earnings ratio is roughly 38 today compared to a long-term average of about 32. And its price-to-book-value ratio is nearly 8 right now compared to a five-year average of 4.5. All of these traditional valuation metrics scream that the stock is overpriced.

NYSE: ETN

Key Data Points

I'm a dividend investor, so there's one more metric I look at. Although dividend yield is a less traditional valuation tool, I find historical yield ranges to be a reliable, though rough, guide to valuation. Right now, Eaton's yield is a miserly 1.1%. While that's above the 0.9% yield of the average industrial stock, using iShares U.S. Industrials ETF as a proxy, it is below the 1.2% yield of the S&P 500 index. More to the point here, however, Eaton's yield is at the low end of the company's own historical yield range. Taken together, those yield metrics here suggest an expensive stock, backing up the view provided by more traditional valuation tools. So I just can't justify buying the stock at current levels.

Eaton is a growth stock, but an expensive one

Based on its well-positioned business, I can see why growth investors would find Eaton interesting. But given its current valuations, anyone buying it today is paying a hefty premium. However, that's also why its 30% price drop earlier this year is so interesting. Drawdowns like that have actually been fairly common in Eaton's history. So if you are interested in the stock, you might be better off keeping it on your watch list. Then, if there's another big sell-off, you will be able to step in and buy while everyone else seems to be selling.