One way to earn great returns over the long run is to invest in one of the companies worth more than $1 trillion, such as Nvidia, Meta Platforms, Amazon, Alphabet, and a few others. Almost every single member of this highly exclusive club looks likely to perform relatively well during the next decade and beyond.

Another way is to buy shares in companies that are still far from the $1 trillion market cap, but have the potential to get there. That, in my view, describes Robinhood Markets (HOOD 5.12%), a fintech company.

This popular online trading platform is firing on all cylinders. With a market cap of $112 billion, it needs a compound annual growth rate (CAGR) of at least 11.6% to become a trillion-dollar company within 20 years. That's no easy task, but here is why Robinhood can pull it off.

Image source: Getty Images.

Bringing Wall Street into Main Street

The financial industry has evolved considerably. Various services, including stock trading, have become easier and cheaper to access. Some of the changes making that possible include commission-free trading on easily downloadable and highly interactive mobile apps, access to fractional shares that allow investors to buy stocks at almost any price, no minimum balance requirements for basic accounts, and more.

Robinhood helped pioneer the commission-free trading model and offers all those other perks. It was built with the idea that certain services shouldn't be available only to the wealthy or well-connected -- hence the company's name.

This isn't just fun history. It goes to the heart of what has driven Robinhood's success in recent years. The company's platform is particularly popular among younger investors for at least two reasons.

First, they have a preference for accessing all kinds of services through mobile apps compared to older generations. Second, millennials have a complex relationship with traditional financial institutions, with many of them having come of age during the 2008 financial crisis. This popularity with younger people has helped power the company's financial results -- and its stock price -- during the past two years.

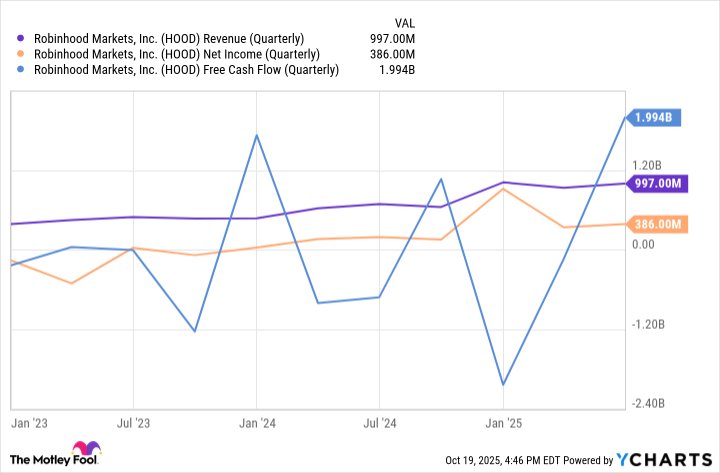

HOOD Revenue (Quarterly) data by YCharts

Beyond revenue and earnings numbers, Robinhood's business has expanded considerably. It ended the second quarter with $279 billion in total platform assets, almost double compared to the year-ago period. The company's funded customers (who are, roughly speaking, active account holders) increased 10% year over year to 26.5 million, while the number of subscribers for its premium Gold service came in at 3.5 million, up 76% from the year-ago period.

NASDAQ: HOOD

Key Data Points

The financial institution of the future

Robinhood made its name thanks to its attractive stock trading feature. Though the company was criticized for its role in the meme stock phenomenon and making risky trades available to newbies, its recent run is vindicating its business model.

But we are arguably still in the early innings of Robinhood's growth story. The advantages that made the company popular among millennials aren't disappearing. Robinhood has also significantly expanded its offering and now competes with traditional financial institutions across many categories, all on the same user-friendly app that made it popular. Millennials are just now entering their peak earnings years (mid-40s to mid-50s).

Meanwhile, Gen Z and Gen Alpha are still some ways away from that. In the next 20 years, they will all become wealthier and increase spending on all the services Robinhood offers, granting the company significant long-term growth opportunities.

True, other banks have adapted to the modern model Robinhood helped pioneer. Still, the company has (or is in the process of building) important competitive advantages.

First, it has built a brand name synonymous with commission-free trading, making it one of the first options new investors are likely to turn to. Brand power counts for something.

Second, as Robinhood's ecosystem deepens and people invest more in various plans -- including things like retirement accounts -- the company will develop high switching costs, meaning customers will be reluctant to jump to competitors.

The bears will argue that Robinhood's shares look too expensive. The company is trading at an eye-popping 71 times forward earnings, a high number by almost any standard, especially when compared to the average of 16.3 for financial stocks.

These reservations are reasonable, but, in my view, the stock remains highly attractive. Robinhood is helping change financial institutions and the way we interact with them, and it could cash in on that during the next two decades, a (more than) long-enough period for the company to grow into its valuation. Robinhood appears in a good position to generate the CAGR it needs through 2045 to become a trillion-dollar stock.