There are juggernauts on the stock market, and then there's Palantir Technologies (PLTR +3.06%). The AI-based deep data analytics company has jumped a remarkable 2,970% since the start of 2023, blowing out nearly every mega-cap stock on the market, including Nvidia.

During that period, Palantir has gone from an unprofitable company with modest growth to a highly profitable, differentiated software engine that is now growing revenue by nearly 50% year over year.

What's changed has been the emergence of artificial intelligence (AI) and the launch of Palantir's artificial intelligence platform (AIP), as well as a push under the Trump administration for government agencies to embrace Palantir's platform, and greater adoption among U.S. corporations.

To determine whether Palantir is a buy, it helps to first understand how Palantir got where it is today.

How Palantir became a (nearly) $500 billion company

Palantir offers its customers services on three major platforms, Gotham, Foundry, and Apollo.

Gotham represents the original core of the business, focused on government, defense, and intelligence agencies. Palantir got its start in the wake of 9/11, helping counterterrorism agencies connect hard-to-find dots hidden in silos of data to prevent the next terrorist attack. Its technology is also rumored to have helped the U.S. find Osama bin Laden.

Foundry helps commercial businesses and civil government agencies solve similar problems, analyzing their data to make improvements to their operations or find new ways to do things.

Apollo acts as the backbone for these two platforms, ensuring continuous delivery and software updates for Gotham and Foundry.

Palantir now considers AIP, which it launched in 2023, to be its fourth platform. AIP takes generative AI and large language learning models to multiply the power of Gotham and Foundry, allowing users to search and get answers more easily, and turn unstructured data into actionable intelligence.

Palantir CEO Alex Karp has repeatedly touted the tailwind and the competitive difference that AIP has provided. It's clearly a major driver of the company's success, and has possibly been the biggest driver of its growth.

The company's U.S. business has been on fire lately as it has been embraced by both the U.S. government under the Trump administration and the commercial sector. In the second quarter, U.S. revenue jumped 68% year over year to $733 million. That was made up of 93% growth in U.S. commercial to $306 million, and 53% growth in U.S. government to $426 million.

Palantir has been a preferred contractor under the Trump administration, and it's made a push to get more agencies on Palantir's platforms so that they can share and more easily manage information.

The company also says that it has no close competitors and that it is competing with the in-house efforts of its customers, which gives it a competitive advantage, especially as its technology evolves with new products like AIP.

NASDAQ: PLTR

Key Data Points

Is Palantir stock still a buy?

Investing in Palantir has clearly paid off for early investors, but the growth of the business isn't the biggest reason for the stock's success. Most of the stock's explosive growth owes to multiple expansion, or its valuation increasing. Some of that is warranted based on the improvement in the underlying business, but it's not a sustainable way for a stock to grow over the long term.

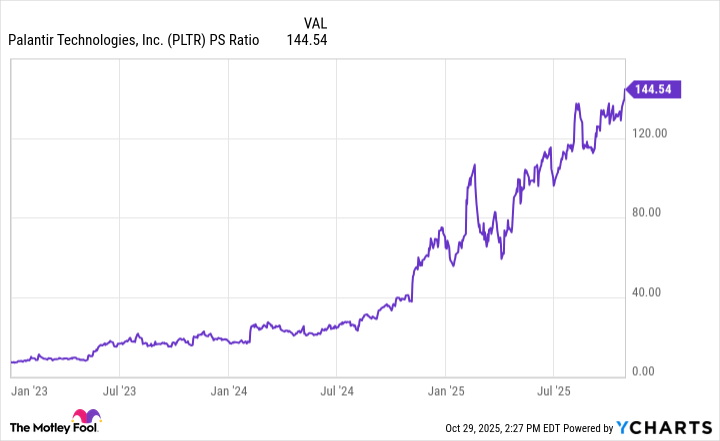

As you can see from the chart below, the stock's price-to-sales ratio has jumped just over 14x, from around 10 to 144, since the start of 2023.

Data by YCharts.

In other words, nearly all of the stock's growth has come from investors placing a higher premium on the stock, while revenue has roughly doubled during the time. At a P/S ratio of 144, Palantir is at an unprecedented altitude for a $466 billion company. That valuation is typically reserved for development-stage biotech and emerging technology companies with barely any revenue, like those in quantum computing. At that price, the stock could get cut in half, and it would still be the most expensive stock on the S&P 500 by far.

Palantir's performance over the last few years has been commendable, but the stock price is simply too frothy at this point, and it looks like further evidence of a bubble forming in the market. A sharp pullback, if not a full-on crash, seems more likely than not to be in Palantir's future, and it could happen without warning.