Back in September, leading artificial intelligence (AI) start-up Anthropic reported that its Claude Code tool was used in a large-scale cyber-attack, which successfully harvested sensitive data from a handful of valuable companies. The most concerning part is that human attackers trained Claude to do their bidding, which allowed them to achieve their goals substantially faster and with much less manpower.

This marks a scary shift in the cybersecurity landscape. Palo Alto Networks (PANW 0.49%), which is the world's largest cybersecurity company, has been preparing its customers for these incidents over the last few years by embedding AI into its products and services, empowering them to neutralize threats with greater speed and accuracy than ever before. Demand is soaring for these advanced tools, and it's showing up in Palo Alto's financial results.

Unfortunately, cyber risks will only keep rising from here, especially with new technologies like quantum computing on the horizon, which could change the digital economy forever. But this could be an opportunity for investors, because it will only bolster demand for Palo Alto Networks' products. A single share in the cybersecurity giant trades for under $200 as I write this, and here's why it could be a great addition to a diversified portfolio.

Image source: Getty Images.

Preparing for the AI and quantum computing revolutions

Palo Alto operates three cybersecurity platforms covering cloud security, network security, and security operations, with dozens of individual products spread across them. The company is seeing a trend toward "platformization," which means businesses are abandoning fragmented cybersecurity stacks in favor of using one vendor like Palo Alto to fulfill all of their needs.

Platformization leads to better protection with faster incident response times, and it allows businesses to seamlessly integrate new products from the vendor. Take Palo Alto's Cortex XSIAM security operations tool, for example, which uses AI to automate threat detection and incident response. It processes 15 petabytes of telemetry data every day, helping over 60% of business customers reduce their median incident response time from days to just minutes. That outcome would be difficult to achieve with a fragmented cybersecurity stack.

But Palo Alto has identified a $10 billion addressable market in another, very early-stage industry: Quantum computing. CEO Nikesh Arora says this technology will soon be able to break all existing encryption methods, potentially creating the biggest cybersecurity threat in history, and businesses have less than five years to prepare. In August, Palo Alto launched a quantum readiness solution called PAN-OS 12.1 Orion, which helps businesses take inventory of their risk levels.

NASDAQ: PANW

Key Data Points

Palo Alto's revenue is growing quickly

Palo Alto generated $2.5 billion in total revenue during its fiscal 2026 first quarter (ended Oct. 31), which was up 16% from the year-ago period. That growth rate matched the fastest pace in almost two years (since the second quarter of fiscal 2024), highlighting the company's strong momentum.

The solid result was driven by Palo Alto's next-generation security (NGS) segment, which is home to many of the company's AI products, where annual recurring revenue (ARR) soared by 29% to $5.9 billion.

Palo Alto said platformization was another big driver of its first-quarter results. In the past, the company said platformed customers typically have a churn rate of almost zero, which means that once they commit to Palo Alto for all of their security needs, they tend to stick around for good.

Thanks to strong revenue growth driven by NGS and platformization, management increased its long-term ARR forecast to $20 billion by fiscal year 2030, up from $15 billion previously.

Palo Alto stock looks attractive relative to its main rival

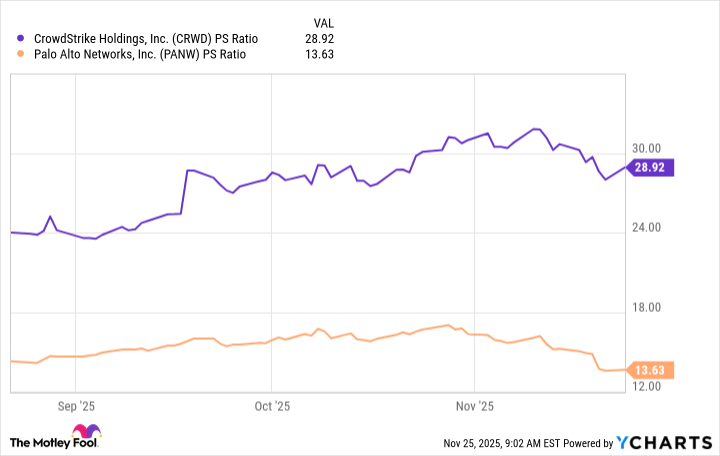

Palo Alto stock is trading at a price-to-sales (P/S) ratio of 13.6 as I write this. That's a steep discount to the 28.9 P/S ratio of its main rival in the AI-powered cybersecurity space, CrowdStrike (CRWD 2.11%):

Data by YCharts.

Investors typically assign higher valuations to faster-growing companies, and CrowdStrike's revenue increased by 21% during its recent quarter, beating Palo Alto's 16% growth. However, Palo Alto's NGS ARR alone is now higher than CrowdStrike's total ARR, and remember, it grew by a whopping 29% in the recent quarter.

As a result, it's very hard to justify the extreme difference in their P/S ratios. In my opinion, either CrowdStrike stock needs to come down significantly from here, or Palo Alto stock needs to move much higher. Even if the outcome is somewhere in the middle, Palo Alto shareholders are likely to experience a healthy upside from here.

Moreover, Palo Alto values its total addressable market at $300 billion over the next three years across all product categories, so even if it achieves $20 billion in ARR by 2030, it will still have captured a mere fraction of its opportunity.