The Nasdaq Composite index has registered a gain of about 20% in 2025 so far, and that's quite impressive considering that the index endured a difficult start to the year and pulled back substantially in the first three months.

There is a good chance that the Nasdaq will carry its momentum into 2026. In an interview with CNBC, Ryan Detrick, chief market strategist of investment management firm Carson Group, pointed out that once bull markets hit three years, they tend to stretch to an average of eight years, based on historical trends going back to 1950.

The current bull market turned three years old last month, and the strong quarterly reports from major technology companies suggest that the Nasdaq's rally is indeed sustainable.

Let's say you have $250 to spare right now that you're ready to invest for the long term. You could consider buying one share each of Nvidia (NVDA 1.81%) and Applied Digital (APLD +8.66%) to capitalize on the potential for the tech sector to continue to surge, as these two tech stocks are likely to pop next year.

Image source: Nvidia.

1. Nvidia

The growth of artificial intelligence (AI) chip leader Nvidia isn't showing any signs of slowing down. Shares of the company are up 34% so far in 2025, trading at around $180 as of this writing, and they seem likely to head higher next year. That's because the demand for Nvidia's data center graphics processing units (GPUs) continues to exceed supply.

NASDAQ: NVDA

Key Data Points

As CEO Jensen Huang pointed out in the earnings release for its fiscal 2026 third quarter (which ended Oct. 26), "Blackwell sales are off the charts, and cloud GPUs are sold out." He added that the need for its hardware continues to increase thanks to the proliferation of artificial intelligence (AI) systems. The hyperscalers that deploy Nvidia's AI chips in data centers to run AI workloads have already indicated that they are likely to increase their spending on them next year.

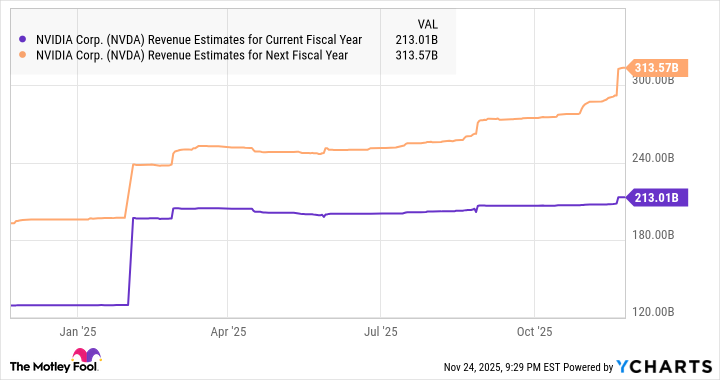

Nvidia can already count on some benefits from those higher data center capital expenditures. The company is yet to fulfill booked orders worth $307 billion in the five quarters through the end of 2026; that's significantly higher than the $187 billion in revenue that it has generated in the past four quarters. So it's easy to see why analysts have ramped up their growth expectations for Nvidia for its next fiscal year (which will begin toward the end of January 2026).

NVDA Revenue Estimates for Current Fiscal Year data by YCharts.

Given that Nvidia continues to get more orders for its AI chips, as management indicated on the latest earnings call, it may end up delivering even bigger revenue growth than currently expected. Moreover, it's building up inventory at a solid pace to satisfy its huge backlog. Its inventory was up by 32% last quarter, while supply commitments increased by 63%.

So, it is easy to see why analysts are forecasting a 58% jump in Nvidia's earnings in its fiscal 2027 to $7.43 per share. Nvidia is trading at just 23 times forward earnings right now, lower than the Nasdaq 100 index's price-to-earnings (P/E) ratio of 32. The market could reward Nvidia with a higher multiple in the coming year thanks to the incredible growth that it is expected to deliver, and that's likely to result in more stock price gains.

2. Applied Digital

Applied Digital stock has shot up by an impressive 211% in 2025 to around $24. But it's also down by about 33% from the high it hit in October. Buying the data center specialist's stock following its pullback could turn out to be a profitable move.

NASDAQ: APLD

Key Data Points

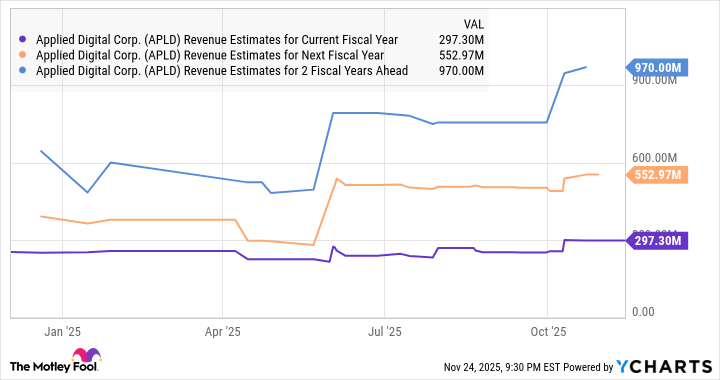

Applied Digital is in the business of designing, building, and operating data centers meant for AI and high-performance computing, and it's currently building two such complexes in North Dakota. The good part is that it has already leased out its data centers for 15 years to CoreWeave and another hyperscale provider. Applied Digital expects to have 700 megawatts (MW) of capacity online by 2027 as compared to its current capacity of 286 MW.

The existing five-year leases that it already has in its kitty represent potential revenue of $16 billion. Even better, Applied Digital has secured $5 billion worth of funding that will help it develop more than 2 gigawatts (GW) -- or 2,000 MW -- of data center capacity in the long run. The company's actual development pipeline, meanwhile, stands at over 4 GW.

Hence, it is easy to see why Applied Digital's growth is expected to take off.

APLD Revenue Estimates for Current Fiscal Year data by YCharts.

Moreover, the growing demand for AI data centers should pave the way for impressive growth at Applied Digital beyond the next couple of years. Of course, the stock is expensive right now at 28 times sales, but the ramp in its revenues should help it justify its valuation. In fact, even if Applied Digital trades at 8.4 times sales after a couple of years (in line with the U.S. technology sector's average sales multiple) and achieves $970 million in revenue that analysts are expecting, its market cap could jump to $8.4 billion.

That would be 27% above current levels, but don't be surprised to see it delivering bigger gains considering its rapid growth and the long-term opportunity in AI data centers, which could lead the market to reward it with a premium valuation.