Palantir (PLTR 0.33%) and Nvidia (NVDA +0.90%) have been two of the best-performing AI stocks since 2023. Palantir is leading Nvidia, rising about 2,640% versus Nvidia's 1,130% rise. Investors would have been thrilled to own either one of those since 2023, but we can't go back and capture those unbelievable returns. We can only look toward the future.

Heading into 2026, each stock has challenges to overcome. But which one is the better buy?

Image source: Getty Images.

Palantir's business model is facing fewer challenges than Nvidia's

Palantir's artificial intelligence-powered data analytics software has found widespread adoption by commercial and government clients alike. It has grown massively since the launch of its AIP platform, which allows generative AI agents to assist its human counterparts.

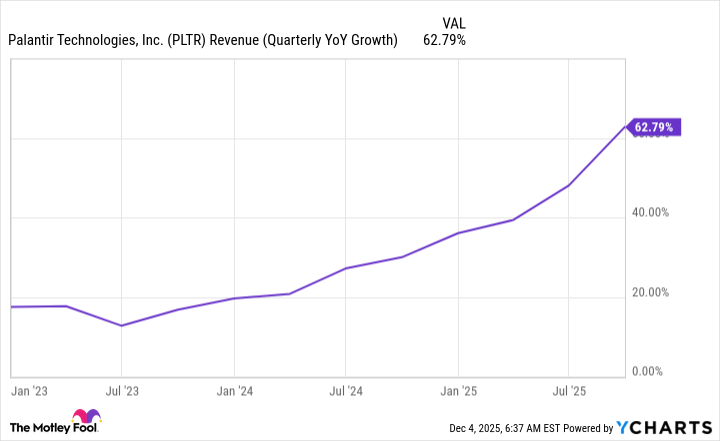

Palantir is nearly unchallenged in its industry and is capturing several big-name clients. Its dominance in an important industry has resulted in impressive growth levels, with revenue rising 63% year over year to $1.12 billion during the third quarter. The most impressive fact about Palantir is that its revenue continues to accelerate, and it consistently outperforms management's expectations.

PLTR Revenue (Quarterly YoY Growth) data by YCharts.

This is almost the exact opposite of Nvidia, which is starting to see challengers arise in its segment.

Nvidia makes graphics processing units (GPUs), which are the most popular computing units for AI workloads. At one point, Nvidia owned an estimated 90% of the data center computing unit market, but that dominance is being challenged.

Rival AMD is stepping up its game. AMD recently partnered with OpenAI to provide it with 6 gigawatts of computing power. Another challenger recently entered the market, with Alphabet potentially offering its Tensor Processing Units (TPUs) to Meta Platforms. These units were designed in collaboration with Broadcom, which has also partnered with several other clients to design custom AI chips that perform better at a lower price than Nvidia's GPUs.

NASDAQ: NVDA

Key Data Points

Challengers are rising all around Nvidia, and this poses a risk for its stock. However, Nvidia's CEO and founder, Jensen Huang, gave investors incredible news during Q3: Cloud GPUs are "sold out." This shifts the narrative from Nvidia is losing ground to its competitor to Nvidia can't produce enough computing units to satisfy demand, so alternative products are growing in popularity.

Investors should focus on the latter mindset, as Nvidia is still posting incredible results, with revenue rising 62% year over year in Q3 fiscal year 2026 (ending Oct. 26). That's nearly the same growth rate as Palantir's 63%. So, despite the rising competition, Nvidia is still hanging in there with a smaller company that has nearly no competition.

While I'll give the nod to Palantir's business due to its dominance and fairly unchallenged nature, Nvidia is still a force to be reckoned with. But there is one thing that's holding Palantir's stock back from being a no-brainer buy.

Nvidia has a reasonable valuation for its growth levels

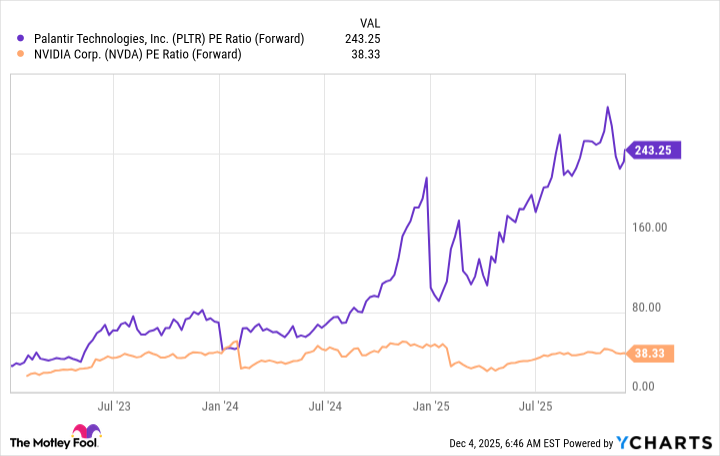

With both companies growing at the same pace with similar margin profiles, they should trade for about the same valuation. However, that's not reality. Palantir has a far greater premium on its stock than Nvidia, and this could hamper future stock performance for Palantir.

PLTR PE Ratio (Forward) data by YCharts. PE = price-to-earnings.

At 243 times forward earnings versus Nvidia's 38 times forward earnings, Palantir is a far more expensive stock. This indicates that there are multiple years' worth of growth already baked into Palantir's stock price, and this could hamper Palantir's stock potential.

On the other hand, 38 times forward earnings for Nvidia isn't historically cheap, but it's not a bad price to pay for a stock whose revenue is rising at a 60% or greater pace. While I'm a bigger fan of Palantir's business state, there are just far too many years of growth priced into its stock already. As a result, I think that Nvidia will be the better investment option in 2026.