If the past 11 months have shown us anything about the mining industry, it's the critical place that rare-earth metal companies are starting to occupy.

Fueled by growing tensions between the U.S. and China -- the largest rare-earth metal miner in the world -- many metal companies in North America have seen their market values grow exponentially this year. Lithium Americas, for instance, is up roughly 75% on the year, while Trilogy Metals is up 280%. Even the VanEck Rare Earth and Strategic Metals ETF is up about 85%, an impressive gain for a metal exchange-traded fund (ETF).

Then, of course, there's MP Materials (MP 0.87%), which has grown 270% on the year. The company, headquartered in Las Vegas, owns and operates the Mountain Pass mine in California, one of the few operating rare-earth mines and processing facilities in the U.S.

NYSE: MP

Key Data Points

Over the past year MP's stock has climbed, slipped, and started up again. That raises the question: Does MP have room to grow in 2026, or has its next growth phase already been priced in?

MP: A year in review

MP Materials is heading into 2026 with a lot of momentum at its back. In 2025, the company signed three huge deals. The first was with the Department of Defense (DoD), which invested $400 million in MP and set a price floor of $110 per kilogram for neodymium-praseodymium (NdPr) products.

The DoD also agreed to give MP a $150 million loan, as well as guarantee a market for 100% of the magnets produced at its 10X Facility for a period of 10 years following its construction. Talk about a huge vote of confidence for MP.

About a week later came another deal, this one from Apple. The tech giant agreed to a $500 million multiyear agreement to buy high-performance magnets from MP, with a $200 million prepayment to help it expand its manufacturing arm.

The last big deal for MP came in November. MP teamed up with the DoD in a joint venture with the Saudi Arabian Mining Company to build a rare earth refinery in Saudi Arabia. Not only will MP hold a 49% stake in the venture with the DoD, but the project gives it a fairly capital-light way to expand its reach beyond Mountain Pass.

Why 2026 could look interesting for MP Materials

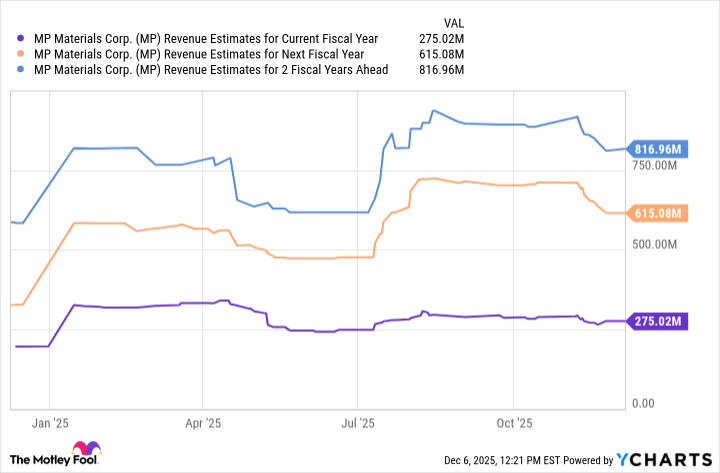

If dealmaking defined 2025 for MP, production progress could define the year ahead. Indeed, in its most recent quarter, MP reported record NdPr oxide output at Mountain Pass, as well as record metal production at its Fort Worth facility. That marks three consecutive quarters of record NdPr oxide.

The uptick in production is one reason the company now expects to turn a profit in the fourth quarter of 2025, after reporting a third-quarter net loss.

MP Revenue Estimates for Current Fiscal Year data by YCharts

Meanwhile, MP continues to expand its footprint. Construction of its 10X Facility is underway, which should greatly help the company scale output further. Later in 2026, MP also expects to commission its heavy rare-earth separation facility at the Mountain Pass mine.

Image source: MP Materials.

In a nutshell, this facility will help MP produce other rare-earth metals, like dysprosium (Dy) and terbium (Tb). These metals are added to high-performance magnets to prevent them from losing strength at high temperatures, which is crucial for EV motors, wind turbines, and defense systems.

Because China controls almost the entire supply chain of Dy and Tb, MP's ability to produce them domestically would not only strengthen its strategic importance, but likely expand its addressable market.

MP has room to run, but risks remain

MP's deal with the DoD was largely why this stock exploded in mid-2025. But investors should note that the partnership doesn't exempt MP from risk. Indeed, just as the DoD purchased equity in the company, it could just as easily sell it, should it find it fit to do so.

Likewise, its deal with Apple is contingent on its ability to build out its manufacturing power. It has capital and financing to do this. But any execution risks -- such as delays, unforeseen supply constraints, or even difficulty hitting Apple's quality threshold -- could slow down the company just as it was ramping up.

As such, MP is still a high-risk, high-reward play on the future of America's supply chain. The stock certainly has room to run, but investors should size positions according to their preferred level of risk.