Robinhood Markets (HOOD 2.02%) operates an investment platform where its clients can buy and sell stocks, options contracts, futures contracts, cryptocurrencies, and more. It's particularly popular with young, first-time investors because it offers commission-free trading, and a user-friendly interface.

Robinhood stock had quite a year in 2025. Not only did it soar by a whopping 200%, it was also added to the prestigious S&P 500 index, where it sits alongside some of the highest-quality names listed on American stock exchanges.

Unfortunately, the stock is now extremely expensive, which could limit further upside in the near term. Moreover, if history is any guide, the areas of Robinhood's business that fueled most of its revenue growth last year could soon run out of steam, which could even trigger a sharp correction in the stock during 2026.

Image source: Getty Images.

Unsustainable growth drivers

Robinhood has two main sources of revenue: Transaction revenue, which comes from processing trades for clients, and net interest revenue, which is the money the company earns on margin loans, and on its cash balances. Transaction revenue is usually the bigger piece, and its composition is increasingly concerning.

During the third quarter of 2025 (ended Sept. 30), Robinhood's transaction revenue totaled $730 million, which was up by a whopping 129% year over year. However, a significant portion of that growth came from its cryptocurrency segment, where revenue surged by 339% to $268 million.

Robinhood's crypto business is notoriously volatile. In fact, during the six-month period between the fourth quarter of 2024 and the second quarter of 2025, its revenue actually plummeted by more than 50%.

NASDAQ: HOOD

Key Data Points

In the last cryptocurrency boom four years ago, Robinhood's crypto transaction revenue rocketed higher by 4,560% during Q2 2021. But popular coins and tokens like Dogecoin, Shiba Inu, and even Bitcoin eventually turned south, and Robinhood's crypto revenue was down 75% by Q2 2022 just one year later.

Most of those cryptocurrencies have been sinking for the last few months, so I won't be surprised if Robinhood's crypto business took another hit during the final quarter of 2025. Unfortunately, the company is lapping a very strong transaction revenue number from Q4 2024, which will be hard to beat.

Therefore, I don't predict much (if any) growth, which won't be well received by Wall Street considering Robinhood's elevated valuation (more on that later).

Image source: Robinhood Markets.

Excitement about prediction markets might be overblown

In August, Robinhood signed a deal with Kalshi to bring prediction markets to its platform. That means that Robinhood's clients can now "bet" on football, basketball, hockey, and soccer games, in addition to elections, and even economic events like interest rate moves. This creates an entirely new revenue stream for the company, which is a key reason its stock rocketed higher in 2025.

But the hype might be a little excessive, because during Q3, Robinhood's prediction business was generating just $115 million in annualized revenue. Wall Street's consensus estimate (provided by Yahoo! Finance) suggests that the company's total revenue likely came in at around $4.5 billion in 2025 (the official results will be reported in late January), so the prediction business would be a paltry 2.5% of that figure.

Plus, Kalshi was valued at just $11 billion during its latest private funding round. So it's hard to believe that this partnership will have a game-changing effect on Robinhood, which is a $105 billion company. With that said, the U.S. sports betting industry is worth $20 billion annually (according to Grand View Research), so there is certainly room for prediction markets to grow.

Why Robinhood stock could move lower in 2026

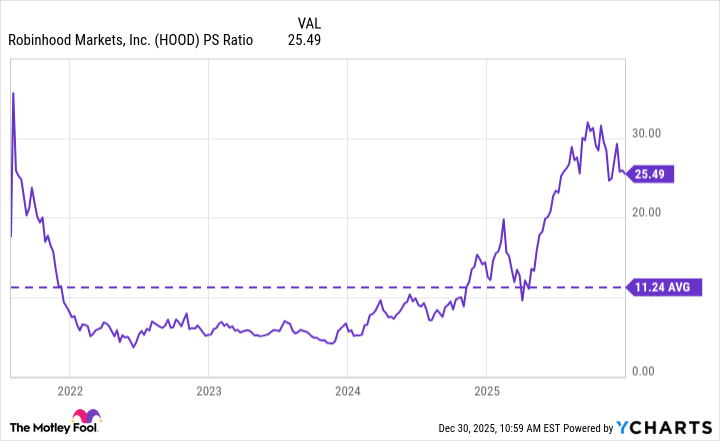

Robinhood stock is trading at a price-to-sales (P/S) ratio of 25.5 as I write this, which is more than twice its average of 11.2 since it went public in 2021.

HOOD PS Ratio data by YCharts.

Robinhood would have to generate significantly more revenue in a very short period of time to justify its current valuation. Failing that, there is a risk that investors will decide to revalue its stock. It would have to decline by a whopping 55% from here just for its P/S ratio to align with its long-term average of 11.2.

When we combine Robinhood's volatile crypto revenue and its hyped-up prediction markets business with its expensive stock, we could have a recipe for a significant correction in 2026. That is the outcome I'm predicting as the year progresses.