With the S&P 500 (^GSPC 1.52%) hovering around an all-time high, some investors may be more interested in cutting-edge artificial intelligence (AI) stocks than a stodgy fast food giant like McDonald's (MCD 0.34%). After all, selling burgers and fries may lack the glitz and glamour of a high-octane growth story, but it can be just the ticket for powering your passive income stream in 2026 and beyond.

By investing $40,000 into McDonald's, you can expect to earn at least $1,000 per year on dividends, and likely more over time if McDonald's continues boosting its payout.

Here's why McDonald's is a top Dow Jones Industrial Average (^DJI 1.56%) component to buy in January.

Image source: Getty Images.

A Dividend King in the making

Last October, McDonald's raised its dividend for the 49th consecutive year -- putting McDonald's on track to become a Dividend King in 2026.

Dividend Kings are companies that have raised their payouts for at least 50 consecutive years. To pull off that feat, companies must consistently grow earnings so they can afford the higher dividend expense. The dividend becomes a key priority for returning capital to shareholders and managing investor expectations.

However, plenty of Dividend Kings are stodgy, slow-growing consumer staples and industrial companies. Unlike Dividend Kings that are past their prime, McDonald's is an ultra-high-margin cash cow with a track record of rewarding shareholders with solid returns on top of the dividend -- with McDonald's producing a 229% total return over the last decade. But McDonald's has cooled, with the stock up just under 15% in the last three years compared to a nearly 80% gain in the S&P 500.

NYSE: MCD

Key Data Points

An industrywide slowdown

The restaurant industry has been under pressure because it depends on consumer discretionary spending. Sit-down restaurants that rely on experiences have been struggling the most, whereas restaurants that cater to convenience and value are doing relatively better.

In McDonald's latest quarter, which was the third quarter of 2025, comparable sales increased by 3.6% and systemwide sales grew by 8% year over year. Systemwide revenue refers to McDonald's restaurants that are corporate-owned or franchised.

Similarly, Restaurant Brands International (QSR +0.11%), which is a quick-service restaurant conglomerate that owns Tim Hortons, Burger King, Popeyes, and Firehouse Subs, grew systemwide sales by 6.9% in the third quarter of 2025, including 4% comparable sales growth.

For context, Chipotle Mexican Grill (CMG 3.87%) grew sales by 7.5% year over year in the third quarter of 2025, but that was mainly due to new store openings. Comparable store sales grew by a paltry 0.3%. Meanwhile, Starbucks (SBUX 1.24%) went six consecutive quarters without producing positive comparable store sales before breaking the streak in its latest quarter.

So in this vein, McDonald's is holding up better than some of its more premium-priced restaurant peers.

McDonald's secret sauce for high-margin growth

Chipotle and Starbucks are down big off their highs and could be excellent turnaround plays for patient investors. But folks looking for stable passive income may want to take a closer look at McDonald's.

Like Burger King, Popeyes, Tim Hortons, and Firehouse Subs, McDonald's relies heavily on its franchise model. Roughly 95% of McDonald's 44,000 locations in more than 100 countries are owned and operated by independent business owners -- not McDonald's.

Franchisees benefit from McDonald's brand, supply chain, marketing, and proven business model, in exchange for paying McDonald's a down payment, licensing fees, rent, royalties, and other expenses. The hands-off approach makes McDonald's far more insulated from pullbacks in consumer spending and also much higher margin than restaurants that own all of their locations.

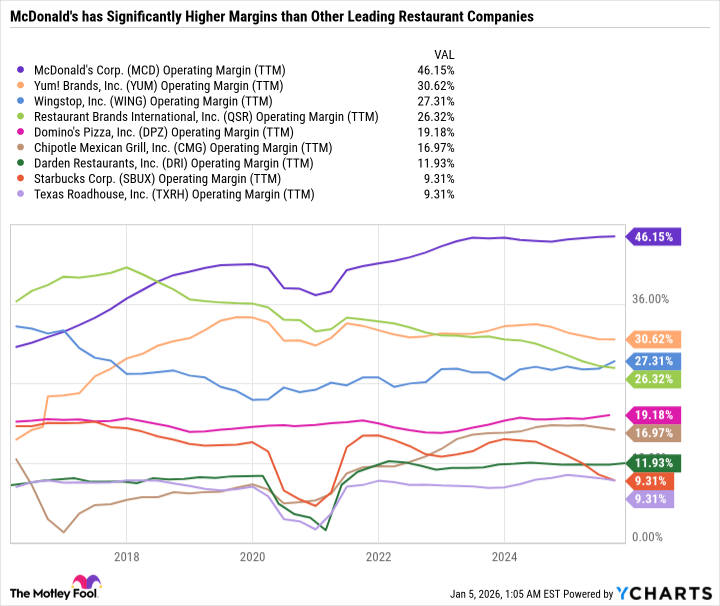

The vast majority of McDonald's, Yum! Brands (which owns Taco Bell, Pizza Hut, and KFC), Wingstop, Restaurant Brands, and Domino's Pizza locations are franchised. As you can see in the chart, these companies have higher operating margins than non-franchise-reliant restaurant companies like Chipotle, Starbucks, Texas Roadhouse, and full-service dining specialist Darden Restaurants.

MCD Operating Margin (TTM) data by YCharts

McDonald's international success makes it less dependent on a single region. So with consumer spending under pressure in the U.S., McDonald's can turn to underserved markets for growth. For example, Japan and Germany are thriving markets for McDonald's right now, even as more established regions like the U.S. and China face challenges.

On its November earnings call, McDonald's reiterated plans to grow to 50,000 stores by the end of 2027 -- a target it set in December 2023. With roughly 4% to 5% annual store growth, McDonald's is undergoing one of its fastest expansions in history, opening at an annual pace of about five new stores around the world every day. That rate of growth would seem risky. But under the franchise model, a lot of the risk falls on the franchisees, not McDonald's.

Investing in dividend quality over quantity

At 22.9 times forward earnings with a 2.5% dividend yield, McDonald's is a reasonable value with a quality yield. There are plenty of other dividend stocks with higher yields. However, McDonald's stands out among other passive income opportunities due to the quality of the business and its ability to grow steadily, regardless of economic cycles.

McDonald's may appeal to risk-averse investors seeking to supplement their retirement income or those looking to diversify a growth stock-heavy portfolio with a quality blue-chip dividend stock.