If there was ever a time to buy shares of D-Wave Quantum (QBTS +4.56%), that time could be now. The quantum computing company recently made a key move that strengthened its position amid the competition.

On Jan. 7, D-Wave announced it will acquire Quantum Circuits, which also develops quantum computers. The merger enables D-Wave to accelerate its efforts to launch a quantum machine with broad market applicability. While quantum computers can complete complex calculations in minutes that would take centuries with a classical supercomputer, the tech is still nascent, limiting its widespread use. Quantum Circuits can advance D-Wave's solutions, boosting adoption.

Let's unpack D-Wave's latest achievements to understand if its stock is a worthwhile investment.

Image source: Getty Images.

How D-Wave's acquisition helps

D-Wave's acquisition is significant because Quantum Circuits works on superconducting gate-model quantum computing systems. This technology differs from D-Wave's approach, which focuses on annealing quantum computers. These machines are particularly good at solving optimization problems. For instance, D-Wave's devices can help logistics businesses identify the best vehicle routes.

However, annealing quantum computers are not ideal for general computational tasks, limiting their practical application. That's because the quantum components performing calculations, called qubits, are difficult to control in a quantum annealing system. By contrast, the qubits in gate-based quantum computers can be manipulated with great precision, allowing these types of machines to be used universally. By acquiring Quantum Circuits, D-Wave has now gained the capabilities for its tech to be applied more broadly.

NYSE: QBTS

Key Data Points

D-Wave's other recent accomplishment

In addition to the Quantum Circuits acquisition, on Jan. 6, the company announced what it called an "industry-first milestone" when it integrated cryogenic controls onto its quantum computer chip. This is important because, traditionally, controlling qubits required encasing them in large cryogenic enclosures that kept temperatures colder than outer space, necessitating complex wiring, and limiting system scalability.

D-Wave's breakthrough means its quantum machines are more practical to use and support easier scaling of the technology. This combined with a more holistic product offering, thanks to the addition of Quantum Circuits, can help it produce more revenue, which is something it sorely needs. For example, in the third quarter, D-Wave delivered a 100% year-over-year increase in sales. While that sounds impressive, it amounted to Q3 revenue of $3.7 million. Meanwhile, its Q3 operating expenses totaled $30.4 million, resulting in an operating loss of $27.7 million.

To raise the funds needed to keep operations going, the company executed multiple equity offerings in 2025. Consequently, D-Wave exited Q3 with the largest cash balance in its history with over $836 million in cash and equivalents, although $250 million will go toward the Quantum Circuits acquisition, along with $300 million in stock.

To buy or not to buy D-Wave shares

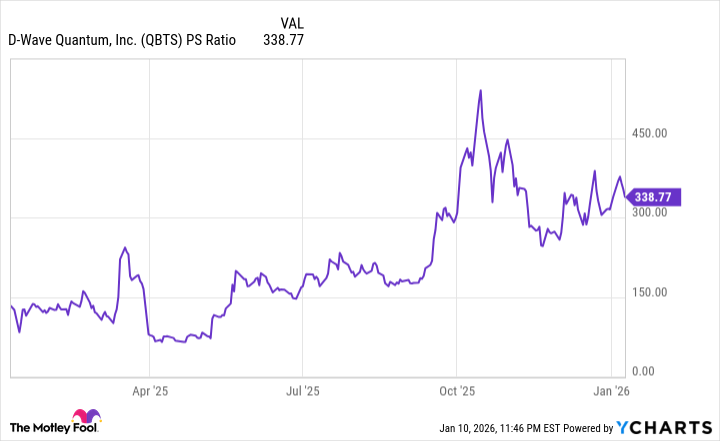

D-Wave is off to a strong start in 2026 with a new technological achievement and a key acquisition. This makes the company a compelling investment. However, one factor to consider is its share price valuation. This is high, as illustrated by the stock's price-to-sales (P/S) ratio, which indicates the cost to investors for every dollar of revenue the company generated over the past 12 months.

Data by YCharts.

The chart shows D-Wave's sales multiple is down from its October high over the past year but remains above 300 as of Jan. 10, suggesting shares are pricey. Contrast this with International Business Machines, which is developing its own gate-model quantum computers, and sports a P/S ratio of about 4.

That said, as a pure-play quantum computing company, D-Wave trades more on its potential to deliver game-changing technology than its financial performance. To consider an investment worthwhile, you have to believe that D-Wave's advances in 2026 now position it to produce innovative quantum technology that can increase revenue.

Even so, given the lofty share price valuation, low sales, and high operating expenses, only investors with a substantial risk tolerance should consider buying D-Wave stock. For others, it would be prudent to wait until the company can prove it's on a path to greater revenue growth than it's managed to date.