The 2011 film Moneyball popularized the saying, "How can you not be romantic about baseball?" -- a reference to the sport's timeless traditions, underdog stories, and hope. In investing, often the focus is on returns and the pure numbers. But there's a romantic side to building a financial portfolio, too.

Owning a piece of a business is an empowering feeling, no matter how small your stake. It means you have skin in the game and are willing to delay gratification by putting your hard-earned savings to work in a company rather than numerous alternatives. Investing is one of the most accessible paths toward achieving the American Dream. And a person can start with almost any amount of money, even a couple of hundred dollars.

Nvidia (NVDA 0.29%) is trading around $186 per share at the time of this writing. Here's why it's the perfect growth stock to buy with $200 right now.

Image source: Getty Images.

A not-so-magnificent few months for Nvidia

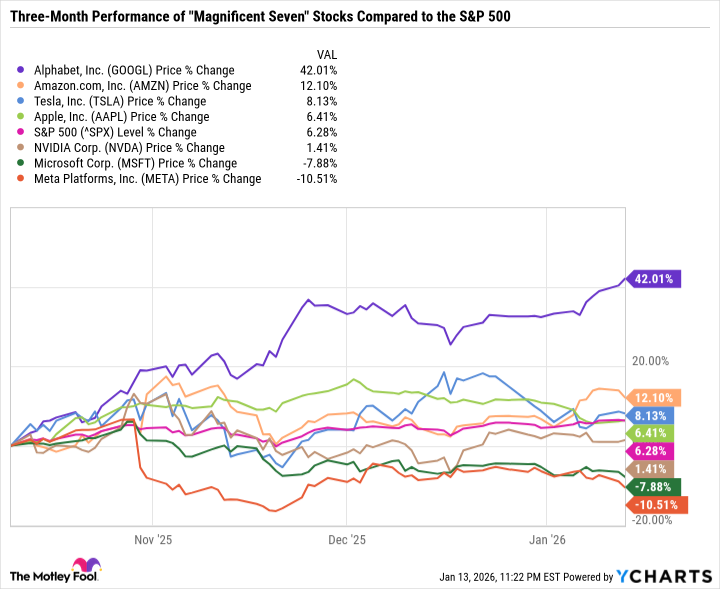

Nvidia is one of three "Magnificent Seven" stocks that have underperformed the S&P 500 (^GSPC 0.06%) over the last three months -- along with Microsoft and Meta Platforms.

Nvidia stock is still languishing despite the major updates the company presented at CES earlier this month. On Jan. 5, it announced that the successor to its Blackwell graphics processing unit (GPU) architecture is already in full production. Named after astronomer Vera Rubin, the Rubin-based products will start shipping to customers in the second half of 2026. Amazon Web Services, Microsoft Azure, Alphabet's Google Cloud, and Oracle Cloud Infrastructure are all scheduled to deploy Rubin hardware in 2026.

The Rubin platform isn't just a GPU -- it's actually six different chips that work together in a system specifically geared toward artificial intelligence (AI) applications, especially the new frontier of agentic AI, self-driving cars, and robotics. By contrast, the Blackwell line was mainly intended for large-scale generative AI and high-performance computing.

The new integrated platform consists of a Vera central processing unit (CPU), a Rubin GPU, a ConnectX-9 Spectrum-X SuperNIC for networking and security, a BlueField-4 DPU for data processing and storage, an NVLink 6 Switch for interconnections, and Spectrum-X Ethernet Co-Packaged Optics that allow GPU clusters to communicate faster with reduced power consumption.

In its CES presentation, Nvidia showcased how the Rubin platform will reduce costs and improve performance -- such as a five-fold improvement in inference power and 3.5 times the training power compared to Blackwell.

In the past, efficiency improvements primarily centered on Moore's Law -- a long-established pattern that predicts that chips' complexity and power will double roughly every two years, largely due to the industry's steadily advancing ability to pack more transistors onto each chip. The Rubin GPU has 60% more transistors than Blackwell, which began commercial shipments in 2024. So Moore's Law remains a driving force of chip advancement. But the real efficiency improvements come from Rubin's integrated design, which aims to reduce or eliminate AI workload bottlenecks.

Rack scale refers to integrating the entire server rack into a cohesive unit, rather than siloing functions such as memory, storage, and networking. Modern hyperscale data centers contain thousands, or even tens of thousands, of server racks. Rubin is built for rack scale -- providing a plug-and-play solution for data centers rather than selling GPUs and having customers figure out how to use them. Nvidia is maximizing efficiency and cost savings beyond the GPU -- allowing it to play an even bigger role in AI data centers.

NASDAQ: NVDA

Key Data Points

Nvidia's elite profitability

After Blackwell's monumental success, Nvidia could have easily rested on its laurels. But the company has a culture of relentlessly pursuing innovation. It's a core reason to own the stock for the long term, even if you're starting by buying just one share.

One of Nvidia's greatest competitive advantages is that it can afford to innovate quickly, even if that means it's cannibalizing sales for its existing product lines. Its hardware commands such high margins because of its rapid pace of innovation. It can justify charging sky-high prices for the next new thing -- in this case, Rubin -- and hyperscalers will line up to buy whatever is available.

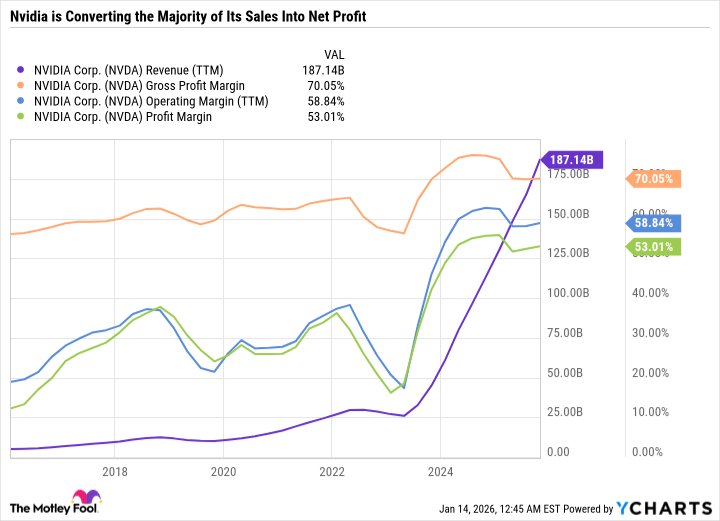

Nvidia's revenues skyrocketed in recent years as its key end markets shifted from gaming, professional visualization, and autonomous driving to data centers.

NVDA Revenue (TTM) data by YCharts.

Nvidia is converting around 70 cents of every dollar in sales into gross profit, 59 cents on the dollar into operating income, and 53 cents on the dollar into after-tax net profit.

One common challenge to Nvidia's investment thesis is that intensifying competition and moderating demand will eventually erode those high margins. But so far, that hasn't been the case, despite new chip developments from Advanced Micro Devices and the rising interest in Broadcom's custom AI accelerators.

Since Nvidia is so profitable, it doesn't need to grow sales by a high percentage to achieve impressive earnings growth. Its high margins justify a premium valuation -- with the stock commanding a price-to-earnings ratio of 45.9 based on trailing 12-month earnings, but just 24.4 based on analysts' consensus estimates for its fiscal 2027, which ends in January 2027. With Rubin shipping in the second half of this year, Nvidia's fiscal 2027 results could blow those expectations out of the water -- making the stock look even more reasonably priced now.

A growth stock to build your portfolio around

With a high-profile company like Nvidia, it's easy to assume that the investment thesis is played out because the stock is so popular. But that assumption couldn't be further from the truth in this case.

Nvidia is valuable because it is rapidly growing earnings while maintaining its margins -- not because of expectations about how it will fare down the road. There are plenty of AI stocks that are trading at levels that will require investors to have extreme patience and a high risk tolerance, but Nvidia isn't one of them. Rubin is here, and its impact will begin to show up in the coming quarters.

Add it all up, and Nvidia is a growth stock hiding in plain sight to plug $200 into right now.