Finding surefire artificial intelligence (AI) winners isn't hard when companies are spending as much as they are. There are several investment opportunities to cash in on the massive spending in AI, and I think two at the heart of this spending are Taiwan Semiconductor Manufacturing (TSM 4.45%) and Micron Technology (MU +0.62%). Both of these are at the core of all artificial intelligence technology, and without them, AI wouldn't look the same.

I think these two are clear winners in 2026, and investors should ensure they have proper exposure to them.

Image source: Getty Images.

Taiwan Semiconductor

Taiwan Semiconductor is the world's leading provider of logic chips. It generates the most money of any chip foundry in the world, as it has risen to become a prominent partner with two of the largest tech giants in the world, Nvidia and Apple. Without Taiwan Semiconductor, generative AI wouldn't be the same. Furthermore, without its production capabilities, the world would be in a massive chip crunch, which would shift how tech operates.

NYSE: TSM

Key Data Points

This makes Taiwan Semiconductor among the most important companies in the world. Its chip production capabilities are unmatched, and with its logic chips powering nearly every high-tech device, it plays an important role in nearly every emerging market trend.

Taiwan Semiconductor is seeing incredible chip demand from AI-related sources. For the five years from 2024 to 2029, Taiwan Semiconductor expects that AI chip growth will increase at a mid- to high-50% compound annual growth rate (CAGR). That's an unheard-of growth rate for a time period that long, and it showcases how important AI is becoming to TSMC's business model.

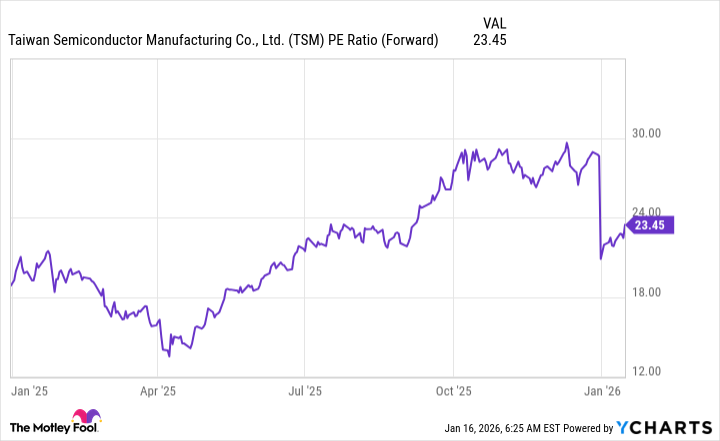

There is huge momentum in this field, and Taiwan Semiconductor is a key part of it. Yet it trades at a discount to many of its peers despite its superior growth rates.

TSM PE Ratio (Forward) data by YCharts

At 23 times forward earnings, it's far cheaper than most of its big tech peers that trade for about 30 times forward earnings despite slower growth rates. I think this discount is an excellent opportunity for investors, and they should scoop up shares due to its strong 2026 potential.

Micron Technology

Micron is on a different side of computing. Instead of making logic chips like Taiwan Semiconductor, it makes memory chips. This is an important piece of AI computing, and AI has consumed all of its capacity. The biggest product AI investors need to focus on is Micron's high-bandwidth memory (HBM), which is used in many leading computing units, like Nvidia's graphics processing units (GPUs). If these memory chips become the bottleneck for AI computing capacity, memory prices could soar, benefiting Micron.

We're already seeing this happen, which is why Micron is doubling its revenue each quarter and is projected to do so again in fiscal year 2026. While there is a significant memory demand bottleneck right now, this isn't always the case. Memory is known to be far more cyclical than logic chips, which is why Micron's stock appears far cheaper than Taiwan Semiconductor's.

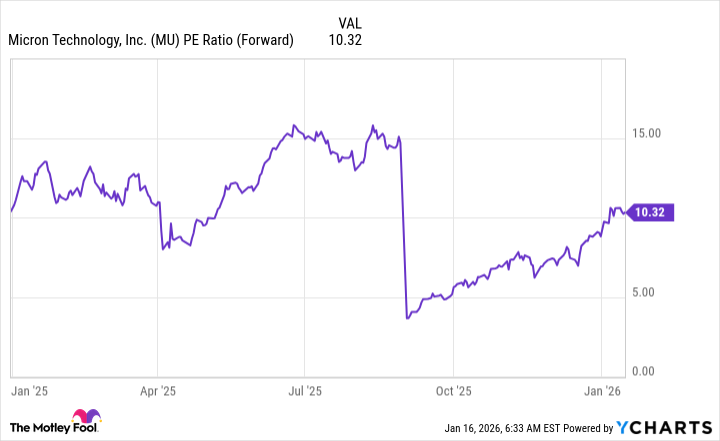

MU PE Ratio (Forward) data by YCharts

At a mere 10 times forward earnings, Micron looks like one of the cheapest AI stocks. This price could be absolutely worth paying if the memory bottleneck extends over the next few years. However, if it is resolved quickly, then investors shouldn't be surprised to see memory prices crash, dragging Micron's stock down.

Still, I don't think investors need to worry much about that. During its Q1 earnings call, Micron's chief business officer noted that the company is "more than sold out." He also noted that this demand will rapidly increase. Micron believes that the HBM market will grow at a 40% CAGR through 2028, and it's in an excellent position to capture that market opportunity.

NASDAQ: MU

Key Data Points

As a result, I think that Micron could be an excellent stock pick for 2026 and beyond, as this crisis hasn't been solved yet.