While most of the investing attention in the artificial intelligence (AI) realm is directed toward Nvidia (NVDA 1.32%), Broadcom (AVGO 1.07%) is starting to gain momentum. Both companies are competing in the AI computing unit field, but Broadcom's product represents the next iteration that could really take off over the next few years.

But is it worth a $1,000 investment right now?

Image source: Getty Images.

Broadcom's approach to AI computing is specialized

Nvidia makes graphics processing units (GPUs), which can be deployed in many applications beyond AI, like cryptocurrency mining or drug discovery. Broadcom is taking a more direct approach and designing a custom AI chip for each of its clients. So, any company that has partnered with Broadcom is getting an application-specific integrated circuit (ASIC) chip suited directly for its workload. This means that a chip designed for Google won't look the same as one for OpenAI; however, each company benefits because their interests are being tailored to.

NASDAQ: AVGO

Key Data Points

Furthermore, by partnering with Broadcom, companies don't have to pay a high premium for its services as they do with Nvidia. Nvidia's profit margin tops 50%, so more than half of the cost of an Nvidia GPU goes to its bottom line. AI hyperscalers are well aware of this, and getting a cheaper alternative through Broadcom that can provide comparable results is the way the market is shifting.

In the first quarter, Broadcom expects its AI semiconductor division to double year over year.

For reference, Nvidia's data center division, which encompasses most of its AI hardware, saw revenue growth of 66%. While Nvidia's growth is impressive, Broadcom's is better. This shows the direction that the industry is headed and makes Broadcom a worthwhile investment.

However, Broadcom isn't a pure play like Nvidia has become. AI semiconductor revenue still makes up less than half of Broadcom's total, although that could shift by the end of the year if its AI semiconductor growth rate continues at its rapid pace. This drags the overall growth rate down, although Wall Street analysts still expect over 50% revenue growth for Broadcom during fiscal year 2026.

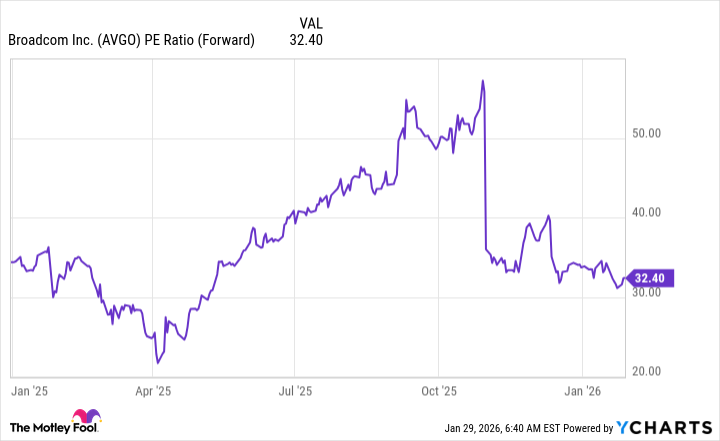

The last consideration for Broadcom's stock is its valuation. At 32 times forward earnings, Broadcom isn't a cheap investment.

AVGO PE Ratio (Forward) data by YCharts

This is about where the big tech companies trade, so it isn't that expensive. Furthermore, the AI spending spree is expected to last through at least 2030, and if Broadcom's computing units continue to gain market share, this is a reasonable price to pay now.

I think Broadcom is well worth a $1,000 investment, and it will be among the best performers in the stock market over the next five years.