On the surface, there are two good reasons for dividend-focused investors to prefer PepsiCo (PEP +0.20%) over Coca-Cola (KO 0.69%). While both stocks are Dividend Kings with over 50 years of annual dividend increases, PepsiCo offers a significantly higher dividend yield of 3.8% compared to Coca-Cola's 2.8%. PepsiCo has also been raising its payouts much faster than Coca-Cola in recent years, with its dividend rising by 39% since 2021, compared to 21% payout growth for Coca-Cola.

But unfortunately for PepsiCo, the favorable comparisons stop there. Coca-Cola has its rival beat in three metrics that make it a much more promising investment, both in terms of capital appreciation and income. These reasons are part of why I prefer Coca-Cola stock to PepsiCo.

Image source: Getty Images.

1. Coca-Cola's earnings growth is leaving PepsiCo's behind

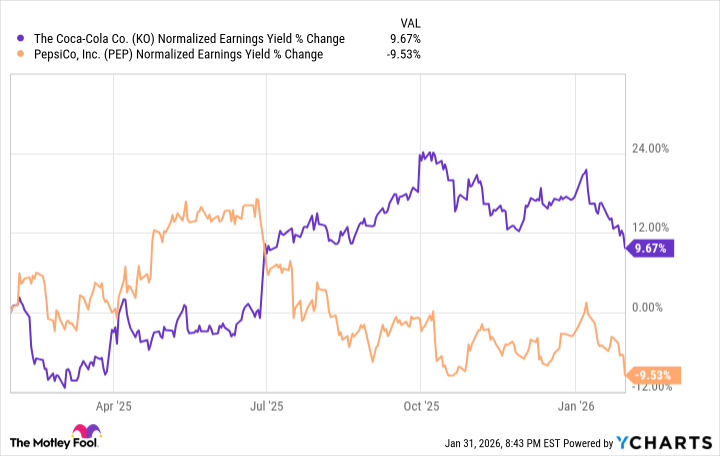

Last quarter, Coca-Cola reported adjusted earnings growth of 30%, compared to an 11% retreat in adjusted earnings for PepsiCo. Adjusted earnings, which portray earnings after excluding one-time expenses like acquisitions or litigation expenses, can offer a clearer picture of core operational profitability.

That's especially true of both PepsiCo and Coca-Cola, which have taken on a series of acquisitions to diversify their product lineup as fewer people drink soda.

NYSE: KO

Key Data Points

And last quarter wasn't a one-off result. Coca-Cola's adjusted earnings growth over the past year is up almost double-digits, while PepsiCo's has shrunk by almost the same amount.

Data by YCharts.

This is a sign that Coca-Cola's core operations are expanding profitability faster, and it is very bullish for the stock.

2. Coca-Cola's profit margin is higher (and growing)

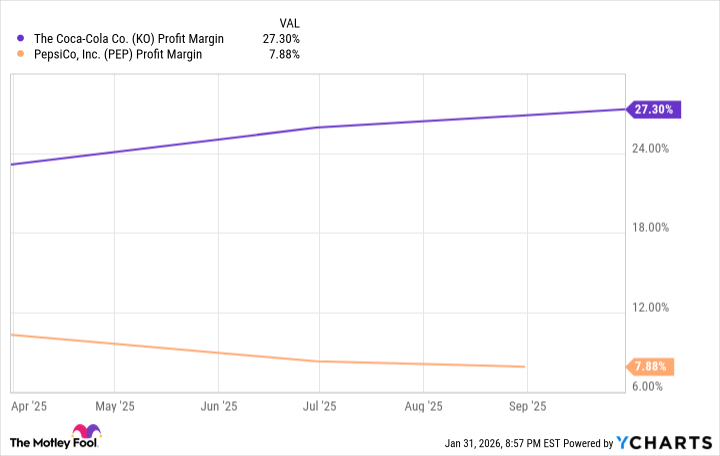

The soft drink industry's average profit margin is 13.4%, but Coca-Cola's towers above that at 27.3%. PepsiCo, by contrast, significantly lags at 7.8%.

As you can see, Coca-Cola's profit margin has climbed in recent months, while PepsiCo's has fallen.

Data by YCharts.

Growing profit margins in the consumer discretionary sector can indicate pricing power and efficiency, not to mention a superior brand.

3. Coca-Cola's dividend looks safer

Both Coca-Cola and PepsiCo are Dividend Kings -- rare companies tend to be resilient, well-run, and highly adaptable.

But when Dividend Kings fall, they fall hard. Take the flooring and furnishing company Leggett & Platt, which was forced to end its 52-year dividend-hiking run in April 2024. Share prices cratered over 60% in the following year.

NASDAQ: PEP

Key Data Points

With PepsiCo's dividend, one warning sign is flashing. Its payout ratio stands at 105%, meaning it's spending more to pay its dividend than it makes in net income.

Looking at PepsiCo's operating cash flow -- the amount of cash its core businesses generates -- the picture is brighter.

PepsiCo's $11.75 billion in operating cash flow is enough to cover the $7.84 billion in dividends it's currently paying each year on shares outstanding. But falling profit margins, if they're not reversed, may force the company to cut the dividend within a few years, costing PepsiCo its hard-won Dividend King status.

With a payout ratio of just 66%, Coca-Cola doesn't face this problem. Its growing profit margin, growing earnings, and stronger fundamentals as an income stock make it the better buy.