Microsoft (MSFT +1.15%) is a company that attracts a lot of attention during earnings season. As it is one of the largest and most influential tech companies in the world, its earnings not only provide a look into its business but also give a glimpse of broader tech trends.

Unfortunately, this latest earnings report was a tale of two different stories for Microsoft. On the one hand, it delivered an impressive financial performance. On the other hand, a less-than-stellar outlook caused its stock to decline nearly 10% on Jan. 28, one of the largest same-day declines in its history.

Stock price slump aside, here are five key takeaways from Microsoft's latest earnings report.

Image source: Getty Images.

1. Microsoft is still a cash cow

Making money has never been a real issue for Microsoft. It's a true cash cow that routinely beats expectations. This latest quarter was no different. Microsoft generated $81.3 billion in revenue, up 17% year over year and nearly $1 billion more than expected. Its earnings per share (EPS) of $4.14 was up 24% and $0.22 more than expected. Its net income grew the most, increasing by 60% to $38.5 billion.

Margins were slightly lower due to increased spending, but cash continues to flow. Xbox Content and Services was its only business unit that showed negative growth in the past quarter (down 5%).

2. A lot is riding on Microsoft's relationship with OpenAI

Microsoft's backlog (future revenue from contracts) is currently $625 billion. This would normally be a great thing, but the problem in Microsoft's case is that $281 billion of its backlog is from ChatGPT's creator, OpenAI.

If everything goes as planned, perfect. However, if OpenAI can't fulfill its contracts for whatever reason, Microsoft would lose a nice chunk of guaranteed future revenue. The signs don't point to that being the case, but if predicting the future in business were easy, many of us would avoid foreseeable issues.

NASDAQ: MSFT

Key Data Points

3. Azure's growth could hit a speed bump

Cloud services aren't like social media, where you can virtually add as many customers as you'd like without needing more physical space for them. To bring on new Azure customers, Microsoft has to make sure it has the computing capacity to host and power everything those companies need.

Unfortunately, it currently has more demand than available capacity, which is partly why its backlog is so high. It's not the worst problem to have, but it will likely slow Azure's growth a bit.

That said, its revenue grew 39% this past quarter. Even if its growth slows (which seems likely), that still leaves room for impressive growth, especially given its size.

4. Microsoft's capex continues to increase

In the latest quarter, Microsoft spent $37.5 billion on capital expenditures (capex), which, compared to other megatech companies, isn't that big a deal by itself. What is noteworthy, though, is what this spending is going toward.

Microsoft is spending heavily on building out its artificial intelligence (AI) infrastructure, including data centers, graphics processing units (GPUs), and central processing units (CPUs). The issue with investing heavily in GPUs and CPUs is that they become outdated fairly quickly as newer, more advanced versions become available. And if Microsoft wants to stay ahead of the competition, it'll need to keep up with the latest AI hardware.

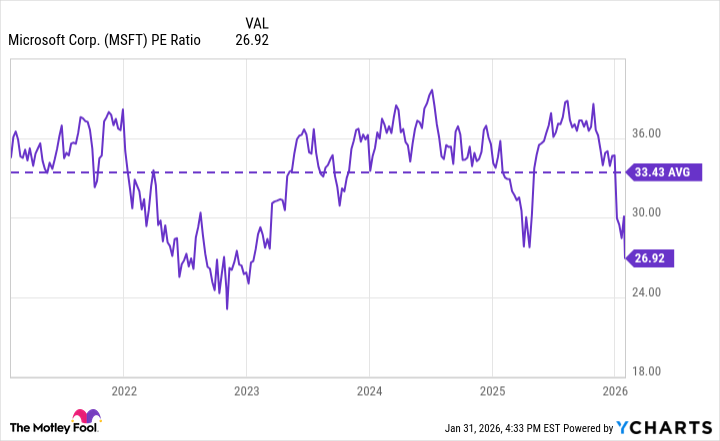

5. Microsoft is a much more attractive investment now

As of market close on Jan. 31, Microsoft's stock is trading at around 27 times its earnings. That's the lowest out of the "Magnificent Seven" stocks and well below its average of around 33.4 over the past five years.

MSFT PE Ratio data by YCharts. PE Ratio = price-to-earnings ratio.

Nobody can say with 100% certainty whether or not Microsoft's stock will continue to fall, but one thing is clear: It's at a much more attractive price now than it was before the drop. It began the year trading at over 30 times its earnings. The drop alone doesn't make Microsoft a buy, but it provides much more upside than downside potential today.