The large mortgage buyer and government-sponsored entity (GSE) Federal Home Loan Mortgage (FMCC 3.10%), also known as Freddie Mac, is not your typical stock. While the company is actually extraordinarily profitable and runs a strong business, its future performance currently depends more on factors beyond its control than on its own operations.

Freddie Mac, along with Federal National Mortgage Association (Fannie Mae), was taken into government conservatorship during the Great Recession. Both companies purchase mortgages from banks and other financial institutions, then package them into securities that can be sold to investors, serving as a vital source of liquidity in the mortgage market.

This allows financial institutions to remove mortgages from their balance sheets, enabling them to meet all consumer demand.

Image source: Getty Images.

During the Great Recession, both Freddie and Fannie purchased too many subprime mortgages. When the market started to unravel, they faced the risk of collapse, forcing the government to inject hundreds of billions of dollars into both entities.

In return, the U.S. Treasury Department received a significant number of warrants, equaling nearly 80% of outstanding common shares, as well as senior preferred stock.

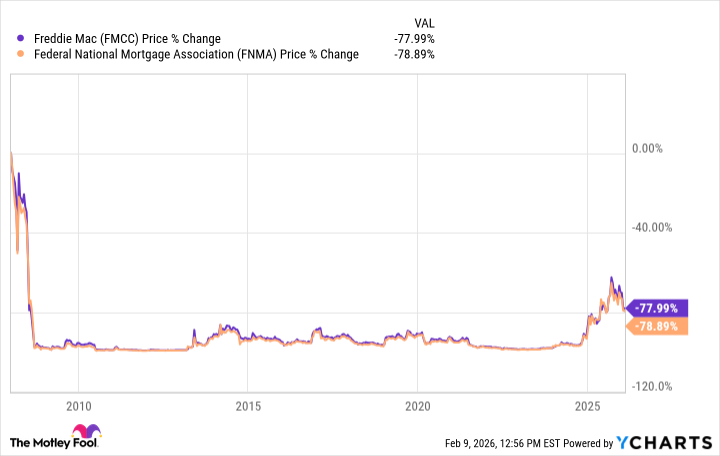

Fannie and Freddie had also been operating under a net worth sweep agreement with the Treasury Department until about 2019, during which they handed all of their profits each year to the Treasury. While Fannie and Freddie have not been great stocks since the Great Recession, here's how they can beat the market from here.

OTC: FMCC

Key Data Points

A real chance to exit conservatorship

As I mentioned above, both Freddie and Fannie actually have good businesses, primarily because they operate as monopolies in the secondary mortgage market. However, their stocks won't perform until it is clear they are exiting government conservatorship.

Since President Donald Trump took office in 2016, there has been momentum to do this and allow Freddie and Fannie to trade publicly. When the net worth sweep agreement ended in 2019, Fannie and Freddie were allowed to retain their profits to build capital to meet new regulatory capital requirements, which they would need to exit conservatorship.

The two GSEs have built capital quickly, but there are other issues to resolve, including significant dilution from both the government's warrants and senior preferred stock.

Some are also concerned that mortgage rates could rise if Freddie and Fannie are no longer in conservatorship, arguing there would be less of a government guarantee than when the Treasury had a significant stake in both companies. However, Fannie and Freddie would remain GSEs even when released from conservatorship and their role in the mortgage market effectively makes them too important to fail.

If the Trump administration can work through all these details and conduct initial public offerings for Freddie and Fannie, both stocks would likely be worth multiples of their current prices. They are both highly profitable entities, but trade at much lower prices because of all the dilution risk and the risk of never exiting conservatorship.

Investors should understand that Freddie Mac is a risky investment, not only because of the issues above, but also because the matter is in regulators' hands and has historically been political, given its origins. If Freddie is not released from conservatorship, the stock is likely to decline and have no upside.

Still, given the multibagger potential, I think Freddie is worth a small investment. Investors can also purchase junior preferred shares of Freddie Mac, which face less dilution risk, but also less upside. The common shares offer the greatest reward but could, in theory, be wiped out or significantly diluted, depending on how the government handles the senior preferred stock and warrants.