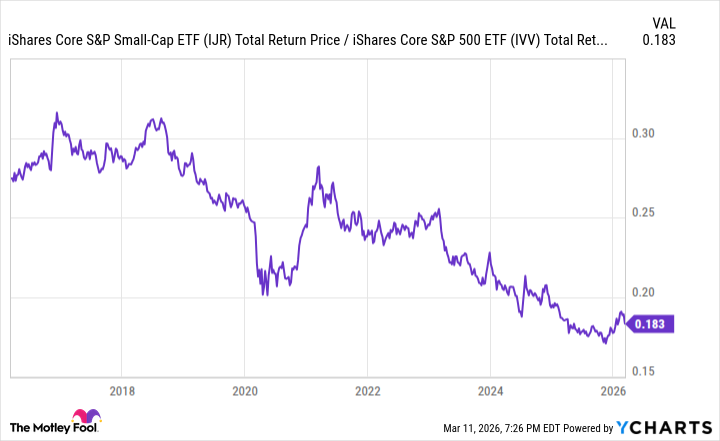

It goes without saying that megacap tech has been the dominant U.S. equity strategy for the past several years. Small caps, often touted as diversifiers and stocks with above-average return potential, have been consistent laggards since 2021. They last peaked relative to the S&P 500 (^GSPC +0.70%) about a decade ago. The chart demonstrates this, using the iShares Core S&P Small Cap ETF (IJR -0.03%), which tracks the S&P 600, and the iShares Core S&P 500 ETF (IVV +0.69%).

Fundamental Chart data by YCharts

One of the core drivers of this trend has been earnings growth. If the S&P 500 were to deliver on its current forecast of 11% earnings growth in the first quarter of 2026, it would mark the 11th consecutive quarter of positive year-over-year earnings growth and the sixth straight quarter of double-digit earnings growth.

The S&P 600 Small Cap Index, however, has been on the opposite end of the spectrum. From Q1 2023 to Q2 2024, it produced year-over-year earnings growth of -10% or worse in six straight quarters. It only just turned positive again in Q2 2025.

But the momentum may only be starting to pick up for small caps.

Image source: Getty Images.

Small caps are about to outpace large caps in earnings growth

If the S&P 600 can deliver on current forecasts, it will generate 29% year-over-year earnings growth in the fourth quarter of this year. The Nasdaq-100, the benchmark for megacap tech, is expected to produce 28% earnings growth over the same period.

In other words, small-cap earnings growth could soon begin to outpace that of the tech sector.

That's important because small-cap performance and valuations have been a product of subpar earnings. The iShares Core S&P Small Cap ETF, which tracks the S&P 600, trades at a price/earnings (P/E) ratio of 18. The iShares Core S&P 500 ETF trades at a P/E ratio of 28.

That kind of valuation gap is understandable when the S&P 500 is delivering such better earnings growth. But when earnings growth rates are similar, the valuation gap should be much tighter. The P/E ratio on small caps has moved modestly higher over the past few years, but the discount relative to the S&P 500 still hasn't budged much. It certainly hasn't repriced to the level it should, given forward earnings growth expectations.

I wouldn't expect large caps and small caps to be trading at similar P/E ratios anytime soon. But I also believe there's a level of value in the S&P 600 that hasn't been unlocked yet. Once it does, I think there's a good chance we see an extended stretch of outperformance for small caps relative to large caps.

Over the next couple of years, I think small caps are the better bet in the U.S. equity category.