Business has been booming for data analytics company Palantir Technologies (PLTR 3.85%) in recent years. Its artificial intelligence (AI) platform has won over numerous commercial and government customers alike. Its growth rate has been solid, as have its margins.

The one sticking point with many investors these days is the valuation. The tech stock simply isn't cheap. But for a top company, particularly one that is growing at such a fast rate as Palantir, a premium is warranted -- it's just a question of how much is too much. Currently, it's trading at well over 200 times its trailing earnings. Is that too expensive for the stock, or could it be justified given its incredibly impressive results?

Image source: Getty Images.

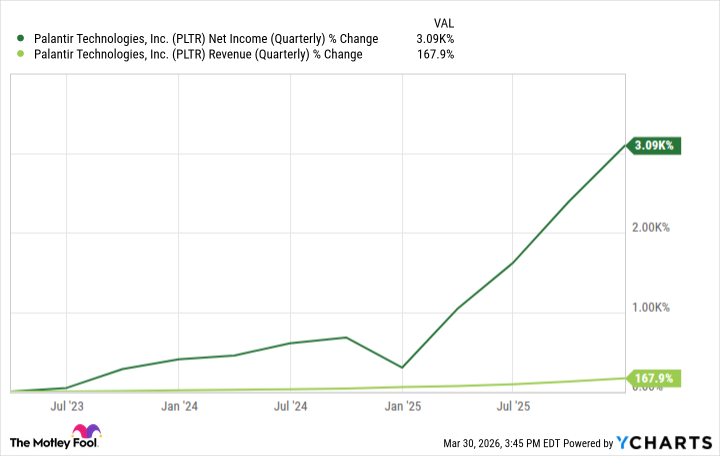

Palantir's top and bottom lines have been skyrocketing

AI has been a tremendous growth catalyst for Palantir in recent years. Not only has it been growing its government business, but it's also generating fantastic numbers on the commercial side. In its most recent quarter, which covered the last three months of 2025, its U.S. commercial revenue rose by 137% -- a far faster rate than the 66% increase in U.S. government revenue.

Palantir has also generated incredible profit growth over the years, but that has been overshadowed by its spectacular top-line growth.

PLTR Revenue and Net Income (Quarterly) data by YCharts

It's not often you see a company generate this kind of growth, and CEO Alex Karp frequently boasts about the company's Rule of 40 score, which is now 127%. It's a combination of revenue growth and its adjusted operating margin.

The business is impressive, but is the stock worth its hefty price tag?

Palantir's market cap is roughly $330 billion today. Its valuation is steep given that the business has generated less than $5 billion in revenue over the past year. But with strong growth on the top and bottom lines, and plenty of excitement around its growth prospects, it's not hard to see why retail investors have been captivated by it.

The danger, however, is that the growth may start to inevitably slow down. Palantir's sales rose by 70% last quarter, which is an incredibly difficult level to sustain for any company. This year, the stock is already down 23%, potentially in light of its sky-high valuation, which leaves no margin of safety for investors if the business slows down. While the company may look unstoppable today, that doesn't mean it'll always be that way.

NASDAQ: PLTR

Key Data Points

While I can understand the excitement around Palantir's stock, I don't think its impressive growth numbers are enough to justify such an inflated valuation. And you should think twice about that high price tag before buying the stock, as doing so could result in limited returns or even losses on your investment.