A couple of years ago, when Nvidia began churning out quarters of triple-digit revenue growth, it almost seemed too good to be true. In hindsight, it was the beginning of the artificial intelligence (AI) boom, and investors who stayed on the sidelines probably wish they hadn't.

History doesn't repeat, but it often rhymes. Funnily enough, it didn't take long. Micron Technology (MU 0.49%) recently turned in an eye-popping earnings report, with sales exploding to more than $23.8 billion for the quarter, up from just $8 billion a year ago.

Is this likely to continue, and does Micron stock still have upside?

Image source: The Motley Fool.

Why Micron's business is going bananas

Micron is selling high-bandwidth memory (HBM), used on Nvidia's GPU AI accelerator chips. The HBM is crucial because AI chips need sufficient, fast memory to process as much data as they do, as quickly as they do. More advanced AI chips require more and faster memory. Micron is seeing a similar tidal wave of demand, similar to Nvidia earlier in the data center boom.

This isn't a fluke, either. The AI boom has created a global memory shortage. Micron noted in its recent earnings call that it can currently meet only one-half to two-thirds of customer demand, indicating the backlog will likely continue to grow. Nvidia's Blackwell AI architecture is still going strong, and its successor, Rubin, has entered full production in anticipation of launch.

NASDAQ: MU

Key Data Points

What does that mean for investors now?

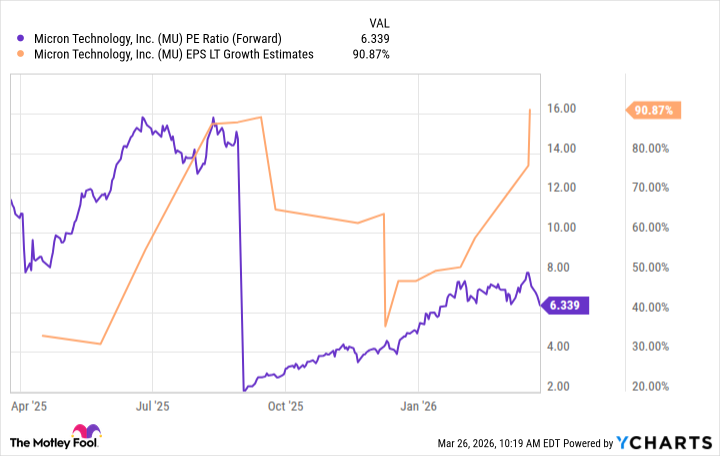

Micron's surging earnings growth makes the stock look very inexpensive. Shares now trade at less than 7 times 2026 earnings estimates, and analysts expect Micron's earnings to grow by an average of 90% annually over the next five years. Micron is clearly benefiting from a supercycle, much like Nvidia has with its GPUs.

MU PE Ratio (Forward) data by YCharts

There are some risks. Micron's pricing power and profit margins could erode a bit as supply catches up. Additionally, the stock fell after Alphabet's Google Research published a paper outlining how algorithms could drastically reduce the size of KV caches in AI models, raising the possibility that efficiencies could ultimately reduce chip memory requirements.

Here's why Micron looks like a buy

Surging earnings growth makes the stock look cheap on a P/E basis, but the supercycle driving that growth looks durable. The leading AI hyperscalers are poised to spend roughly $700 billion this year, and Nvidia's Rubin should set the stage for a strong 2027.

In all, it's hard to ignore the compelling value in Micron stock at its low valuation amid a seemingly sustainable growth spurt.