In the opening months of 2026, shares of Meta Platforms (META +0.22%) have dropped sharply -- erasing roughly 14% of their value year to date and trading about 28% below all-time high prices near $780 in late 2025.

Interestingly, Meta's sell-off is not rooted in waning demand for the company's core advertising products. Instead, investors have recoiled from a one-two punch featuring management's aggressive capital expenditure (capex) plans coupled with fresh regulatory headaches that inspire comparisons to Big Tobacco.

Smart investors are wondering whether the market is overreacting to temporary noise or correctly pricing in structural decline. A thorough analysis of Meta's business, its artificial intelligence (AI) ambitions, and valuation trends suggest recent price action in the stock is far more of an opportunity to buy the dip than avoid a falling knife.

Image source: Getty Images.

Meta's business profile is rock-solid

Meta's climbing engagement metrics provide the company with unmatched pricing power in the digital advertising world.

Data source: Investor relations.

For the full year 2025, Meta's revenue reached $201 billion -- up 22% from the prior year. This growth was fueled by improved monetization from AI-enhanced ad targeting across the company's Family of Apps, including Facebook, Instagram, and WhatsApp.

Operating margins were steady at 41%, while free cash flow generation remained strong at roughly $44 billion. Meta's ability to command robust profitability demonstrates the company can endure heavy costs related to its AI infrastructure.

While margins may take a near-term hit due to rising legal bills, Meta's underlying flywheel of attention across multiple platforms, gold mine of user data, and algorithmic distribution at global scale is both intact and compounding. Taken together, this recipe is not the profile of a business in decline.

Meta's $135 billion bet on AI superintelligence

The headline worry around Meta is the company's capex explosion -- forecast up to $135 billion in 2026. With this level of spend, bears point to a replay of the company's metaverse flop: enormous capital outlays with uncertain payback.

Smart investors understand that the context of AI is far different, though. Unlike the speculation adoption curve of the metaverse, today's AI-related spending is directly supercharging Meta's existing ad empire.

AI tools launched from the company's new Advantage+ suite have already lifted click-through rates and honed creative efficiency for ad campaigns. This improves content moderation feeds, thereby keeping users stickier to Meta's ecosystem for longer durations.

History shows Meta's valuation setup could fuel outsized gains for patient investors

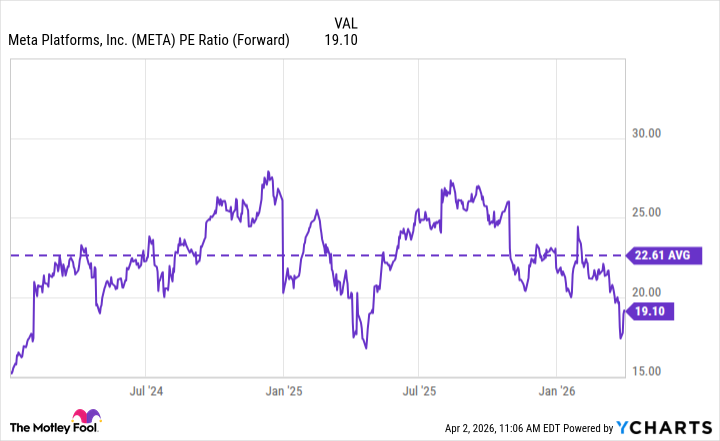

The market has repeatedly punished Meta stock during prior spending ramps -- only to reward patience once incremental revenue gains become obvious. At a forward P/E hovering near 19, Meta trades at its cheapest level since last summer and well below its long-term average of roughly 23×.

META PE Ratio (Forward) data by YCharts

Meta's valuation currently embeds a healthy margin of safety -- one that discounts worst-case outcomes related to legal hoopla and elevated AI spending

Nevertheless, history shows the company's large-scale, focused investments -- Reels in 2020 and the efficiency push in 2022 -- tend to deliver outsized returns once the technology matures. So while the company's 2026 guidance may sting upon first glance, it's far from reckless spending.

Meta is far from a falling knife; rather, the company is a high-conviction compounder on sale. Patient investors should see the 2026 pullback as a long-awaited entry point.