President Donald Trump's $1.5 trillion budget request (comprising a $1.15 trillion base request and $350 billion in reconciliation) for 2027 is exciting defense industry investors, including those in Lockheed Martin (LMT +2.59%). It builds on the $1 billion enacted for 2026 and nearly $900 billion in 2025, and includes many elements (missiles, fire control, space and missile defense, and aeronautics) that are highly likely to improve the company's burgeoning backlog. Does that mean Lockheed Martin is now a stock to hold for life?

An evolving defense industry

To answer the question, it's a good idea to start with the fundamental pros and cons of investing in defense contractors. Traditionally, investors bought stocks like Lockheed Martin because they traded high growth in exchange for the security of a steady stream of income from the safest customers in the world: the U.S. government, other governments, and defense departments.

NYSE: LMT

Key Data Points

Defense stocks were seen as the ultimate "defense" stocks, offering the prospect of low-single-digit growth with some margin expansion thrown in. Theoretically, when you factor in the real prospect of a step change in growth driven by massive defense budgets and the Department of Defense's new Acquisition Transformation Strategy (ATS), it's a perfect recipe for growth. The ATS is a fundamental overhaul that, among many other things, will "Award companies bigger, longer deals, so they will be willing to invest more to grow the industrial base that supplies our weapons."

Image source: Getty Images.

Indeed, Lockheed Martin is an early beneficiary of this new strategy, with management lauding "the landmark seven-year framework agreement for PAC-3 MSE interceptors that we together announced earlier in January" on its earnings call in late January. PAC-3 missiles are surface-to-air missile defense systems.

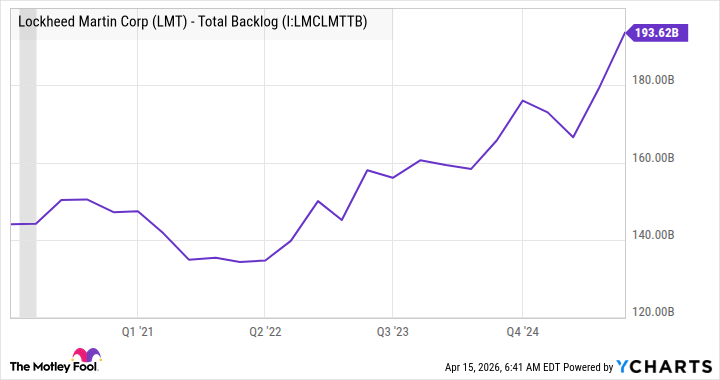

The long-term deal encourages investment by Lockheed Martin and secures revenue for it. It, and other deals under ATS and the proposed 2027 budget, are highly likely to increase Lockheed Martin's already record backlog.

Lockheed Martin Corp (LMT)-Total Backlog data by YCharts

All told, the combination of growing defense spending on long-term contracts, allied with traditional stability, is a perfect combination.

Why Lockheed Martin isn't a "never sell" stock

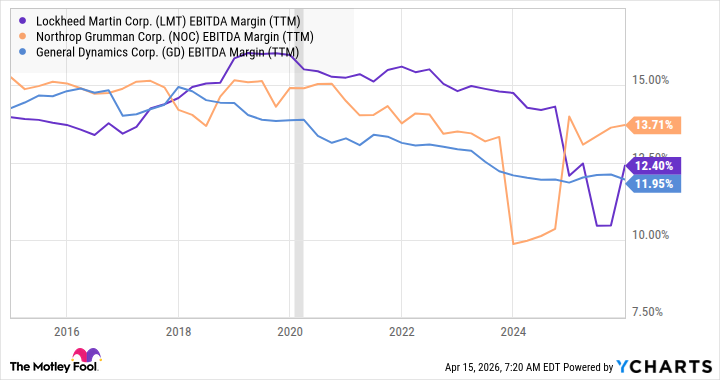

That said, it's important to note that defense stocks have struggled to improve profit margins over the last decade, as measured by earnings before interest, taxes, depreciation, and amortization (EBITDA) margins.

LMT EBITDA Margin (TTM) data by YCharts

The primary reason for margin challenges comes down to the increasingly complex and costly defense programs, notably fixed-price development programs, in which the U.S. government is flexing its monopsony power. These contracts have caused multibillion-dollar losses across many defense companies, including Lockheed Martin.

Indeed, the ATS also calls for the scrubbing of "every government investment deal to confirm it is the best deal for the warfighter to protect our national security," and companies like Lockheed Martin will be held to account for delivering on contracts, particularly if they are deemed to be failing to deliver on unprofitable work.

As such, the budget increase and ATS are a double-edged sword for Lockheed Martin, and investors need to keep a close eye on the company's margins.