For a quarter-century, Plug Power (PLUG -2.78%) has faced an uphill battle with its hydrogen business. During that time, the company has failed to report a full-year annual profit. But there is a renewed sense of optimism, as management is taking steps to be more efficient and setting an ambitious goal of achieving positive operating income by next year.

Recent moves by the company are showing some signs of progress. With shares trading below $4, is now the time to pounce on Plug Power stock? Let's dive into its turnaround efforts to find out.

Plug Power's turnaround effort to achieve profitability by 2028

Last year, Plug Power announced Project Quantum Leap, a major restructuring plan to turn it from a cash-burning, investor-diluting operation into a fully profitable one that can finally generate positive cash flow and reward shareholders. The company hopes to achieve positive earnings before interest, taxes, depreciation, and amortization (EBITDA) by the fourth quarter of this year, positive operating income next year, and full profitability by 2028.

It is taking several steps to reach these ambitious targets. For one, it's looking to automate more of its assembly process, redesign its machinery to use fewer parts, and implement robotic assembly lines as it scales up its manufacturing.

NASDAQ: PLUG

Key Data Points

And after several years of buying hydrogen from third parties at high market prices and selling it to customers at a loss, Plug Power is finally producing hydrogen in-house. This enables it to produce fuel at about one-third the cost, saving it significant money from buying it in the open market, which had been a huge drag on earnings. Now the company is producing hydrogen in its Georgia, Louisiana, and Tennessee plants.

Image source: Plug Power.

It recently scored a huge deal

Plug Power has upside potential given the current state of the energy market and robust demand from industrial operators, and is leaning into its on-site hydrogen production technology. In April, Plug Power was selected as a supplier of a 275-megawatt GenEco PEM Electrolyzer system for Hy2gen's Courant project in Québec, Canada.

As part of this deal, Hy2gen will use hydroelectric power from the Hydro-Quebec grid to run Plug Power's electrolyzer, and the hydrogen produced will be converted to green ammonia and then further processed into renewable ammonium nitrate, a primary ingredient for explosives used in the mining industry. Construction is set for 2027 with full commissioning by 2029.

Is Plug Power a buy right now?

Management is taking steps to improve its efficiency and, ultimately, its margins and bottom line to achieve profitability. As an investor, this is exactly what you want to see. Higher profits mean not diluting shareholders to raise capital, which it has done plenty of, and a chance for the company to reward investors with dividends or share buybacks down the road.

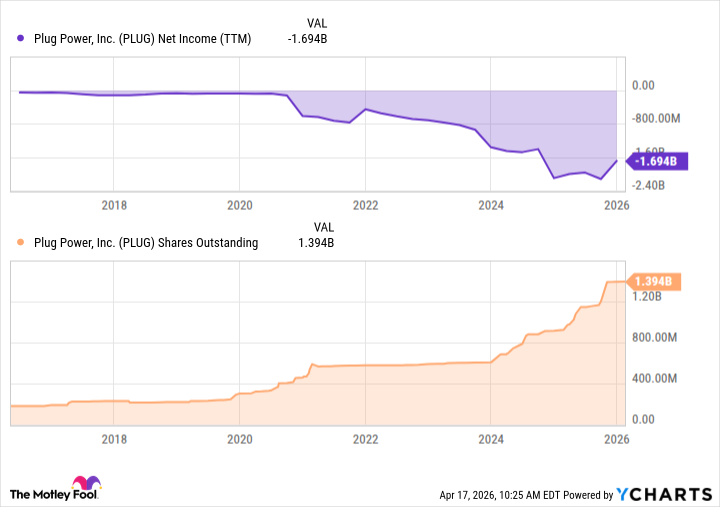

PLUG Net Income (TTM) data by YCharts; TTM = trailing 12 months.

An investment in Plug Power is a bet on the company successfully becoming the hydrogen powerhouse it had set out to become when it was founded decades ago. That said, the stock remains risky at this point, and I'd like to see more tangible results in the coming quarters before investing in this turnaround story.