At first glance, Eli Lilly's (LLY -4.55%) current share price of $903 feels like a psychological barrier. Most investors fixate on the absolute dollars and assume anything this expensive must be priced for perfection. But valuation is never about the sticker price alone; it's more about what you are buying per dollar invested.

Once you strip away the noise of nominal dollars and focus on Lilly's underlying business, a compelling case emerges that the stock is not only reasonably valued but carries attractive upside for long-term investors.

NYSE: LLY

Key Data Points

Share prices are arbitrary when it comes to valuation

Stock prices are not measurements of expensiveness. Companies that compound earnings over decades naturally trade at high per-share prices if they've avoided stock splits or paid significant dividends.

When it comes to valuation, what matters most are trends across a company's price-to-earnings (P/E) ratio or other metrics such as the price-to-free-cash-flow multiple or the enterprise-value-to-EBITDA (earnings before interest, taxes, depreciation, and amortization) ratio.

Investors who fixate solely on share price overlook this distinction. Said differently, a $50 stock with stagnant earnings can be far more "expensive" than a $900 stock whose earnings are set to grow by double-digit percentages. Lilly falls squarely into the latter category.

Image source: Getty Images.

Lilly's GLP-1 leadership meets a diversified pipeline

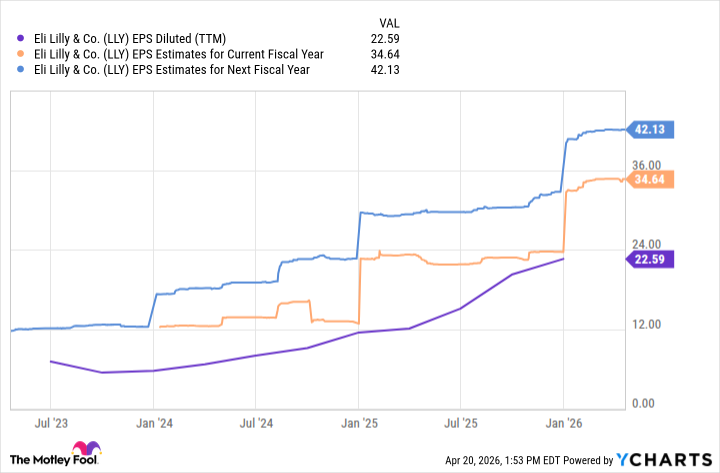

Lilly's revenue and earnings outlook are primarily weighted by the explosive adoption of its dual GIP/GLP-1 agonists, Mounjaro and Zepbound. However, this growth is not a one-trick pony.

Lilly's pipeline has matured into a portfolio well beyond obesity and diabetes. In Alzheimer's disease, the company's anti-amyloid antibody, Kisunla, offers a disease-modifying option in a field long starved for progress. Moreover, the company's recent dermatology and immunology programs add further layers to Lilly's depth.

While each new launch carries its own ramp-up curve, Lilly's diverse ecosystem helps reduce the risk narrative that any single molecule will define the company's trajectory. Wall Street's consensus earnings forecasts reflect this picture as analysts model sustained double-digit profit growth driven by volume expansion from existing segments, complemented by meaningful contributions from newer assets still in early commercialization.

Data by YCharts.

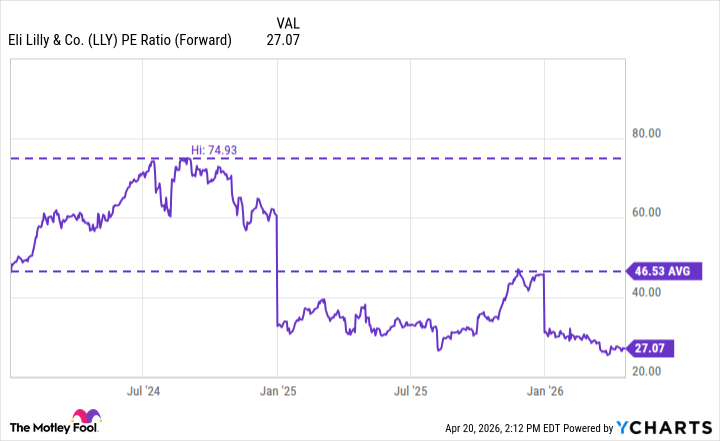

Lilly's forward earnings multiple represents a discount to fair value

Over the last few years, Lilly's portfolio has broadened. In theory, this reduces the risk to the company's ability to generate sustained, robust cash flow going forward. Another way of saying this is that a diversified pharmaceutical giant with multiple blockbuster franchises should command a higher valuation multiple than a single-product business.

Nevertheless, at current levels, Lilly's forward price-to-earnings (P/E) ratio sits at a meaningful discount from the euphoric peaks of the initial GLP-1 hype cycle. In valuation terms, this means investors are paying less per dollar of expected future earnings than they were when Lilly's story was narrower and more binary a few years ago.

Data by YCharts.

As the company's newer drugs shift from clinical promise to billion-dollar commercial realities, Lilly's earnings base is positioned to expand. In turn, the company's valuation multiples are poised to rerate higher. Viewed through this lens, $925 today might prove to be a bargain entry point for investors with a multiyear time horizon.