The pharmaceutical industry has rarely seen a stock rise as spectacularly as Novo Nordisk (NVO +0.58%) did during the GLP-1 boom, only for it to plummet and surrender more than two-thirds of its value from peak trading levels.

What was once hailed as a generational compounder fueled by the runaway success of Ozempic and Wegovy now trades at a price that forces investors to confront an uncomfortable question: Has the market overreacted to narrative-driven noise, or has Novo's underlying growth engine actually started to sputter in ways that could prove permanent?

Image source: Novo Nordisk.

To me, the answer won't be found in yesterday's euphoria but rather in assessing whether Novo's business model still possesses the durability and optionality to compound earnings for the next decade. In my view, Novo's sell-off is a genuine opportunity to buy the dip -- not a value trap -- because the crash is more reflective of investor panic over rising competition rather than legitimate fundamental erosion of the company's structural market position.

The anatomy of Novo's crash

Major sell-offs tend to follow the same blueprint, and Novo's 72% plunge is no exception. A few years ago Novo stock surged, supported by explosive demand for injectable GLP-1 therapies that simultaneously treated Type 2 diabetes and delivered clinically meaningful weight loss. Supply constraints were actually seen as a tailwind as physicians and patients raced to procure every available dose -- creating an impression of insatiable demand.

Once manufacturing capacity scaled and supply volumes normalized, the inevitable happened -- quarterly growth decelerated from triple-digit rates to merely double-digit figures. Wall Street, which was conditioned by Novo's hyper-growth phase, interpreted these results as a warning sign rather than a healthy maturation.

Layered on top of unsatisfying financial results was fear around new competitive forces. Eli Lilly emerged as a formidable rival with its dual-agonist molecule that, in head-to-head studies, appeared to edge out Novo on weight-loss metrics for among certain patient cohorts.

NYSE: NVO

Key Data Points

Meanwhile, smaller, speculative players such as Viking Therapeutics posted eye-catching early data on its own GLP-1 candidates -- raising the specter that the diabetes and obesity opportunity could eventually be commoditized or leapfrogged by alternative dosing.

The stock market hates uncertainty, and the combination of a plateauing growth profile plus credible competitive headwinds triggered a classic panic-sell reaction. The nuance most investors overlook is that the crash in Novo stock was only partly attributed to actual business results. In reality, the sell-off was also spurred by a shifting perception that the company was no longer an unstoppable force to be reckoned with.

Pipeline depth and industry tailwinds support Novo's outlook

A value trap materializes when a stock looks cheap because its core business is structurally impaired due to factors such as declining volumes, eroding pricing power, or no credible path to reacceleration. Novo Nordisk does not fit this profile. The company's broader pipeline is more differentiated and therefore less vulnerable than the headlines suggest.

Beyond its core semaglutide franchise, Novo has advanced combination therapies such as CagriSema that target multiple gut hormones -- potentially delivering superior efficacy while addressing side-effect profiles that currently limit patient adherence. The company has also invested heavily in oral formulations aimed at indications beyond weight loss -- heart failure, chronic kidney disease, and even neurodegenerative conditions.

Crucially, the total addressable market (TAM) for diabetes and obesity is nowhere near saturated. Taken together, these conditions affect hundreds of millions of people around the world. The blended penetration of GLP-1 therapies remains in the low double digits across most major geographies. Even if Eli Lilly captures meaningful market share or if an oral competitor succeeds, the overall pie is accelerating fast enough to accommodate multiple winners.

Valuation reset: Fear around Novo is a buying opportunity

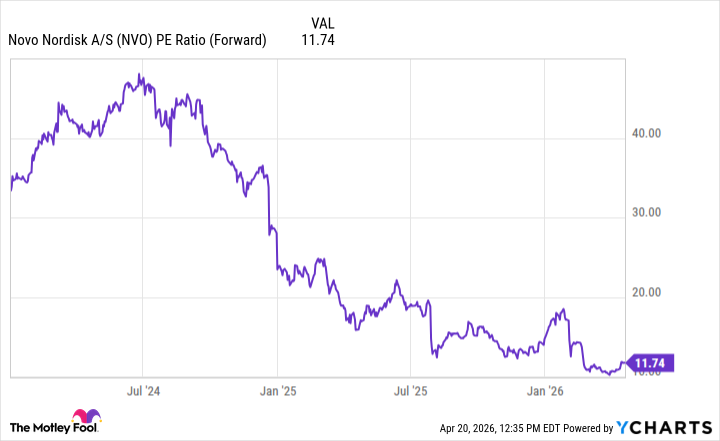

At current levels, Novo trades at a forward price-to-earnings (P/E) multiple that has compressed dramatically from its peak.

NVO PE Ratio (Forward) data by YCharts

A value trap would require Novo's growth to be more of an illusion because volumes are about to collapse or because competition will destroy the company's profitability. Neither scenario appears probable in my view.

Against this backdrop, Novo's sell-off looks overblown as investors have priced the stock for a scenario of rapid market share deterioration and prolonged growth deceleration that clinical and epidemiological data simply are not supporting. Novo is far from a one-trick pony on the brink of obsolescence.

The trends above illustrate that investors have already baked in an aggressive loss of market share and a harsh de-rating of growth. When the expectations are this low, any outcome short of a catastrophe could easily drive meaningful valuation expansion.

Novo Nordisk's crash has created the kind of dislocation that separates temporary negative sentiment from enduring headwinds to the company's long-term trajectory. For investors with a multi-year time horizon, this dislocation is an invitation, not a trap.