As one of the world's leading producers of advanced memory chips, Micron Technology (MU -1.89%) has emerged over the past year as a key player in the artificial intelligence (AI) build-out. The company designs and manufactures DRAM and NAND flash chips that are essential components in AI data centers, as well as in a host of consumer electronics applications.

Rising demand for data center infrastructure has already lifted Micron's profits and sales remarkably, but I think the AI megatrend could propel it into rarefied territory: the trillion-dollar club. While such a prediction may look aggressive at first glance, I think Micron has the optimal mix of market presence and secular tailwinds to fuel further market-beating gains.

Image source: Getty Images.

Why Micron matters in the AI race

To train and power large language models (LLMs) and generative AI applications, enormous amounts of data frequently must be transferred at lightning speed among whole fleets of processors. In order for them to access that data at the necessary speed, it needs to be stored in high bandwidth memory as close to those processing chips as possible. Micron's high bandwidth memory (HBM) solutions are engineered for this application, delivering the density and processing throughput required by clusters of AI accelerators.

Without sufficient HBM, even the most powerful GPUs can't work to their full potential. As the AI infrastructure build-out accelerates courtesy of the hyperscalers, Micron has swiftly become an indispensable supplier of chips for next-generation AI factories.

NASDAQ: MU

Key Data Points

Explosive revenue growth and expanding profit margins

Micron's recent revenue surge stems from the insatiable demand for its premium HBM products, which command significantly higher prices and margins than its legacy memory chips. AI-driven orders are well outstripping supply, allowing Micron to steeply boost its prices. It's also pouring money into boosting its production capacity for its most advanced manufacturing nodes, lowering its chip production costs in the long run.

Image source: Micron Technology Investor Relations.

A subtle theme worth pointing out from the table above is that sales in Micron's traditional markets in servers, PCs, and smartphones are showing signs of healthy recovery as remaining capacity flows downstream from hyperscaler workloads to consumer end markets.

The combination of higher average selling prices, operational efficiencies, and disciplined capital allocation has driven Micron's profit margins to new highs.

-- transforming what was once a cyclical memory and storage business into a much more profitable enterprise.

Can Micron realistically reach a $1 trillion valuation?

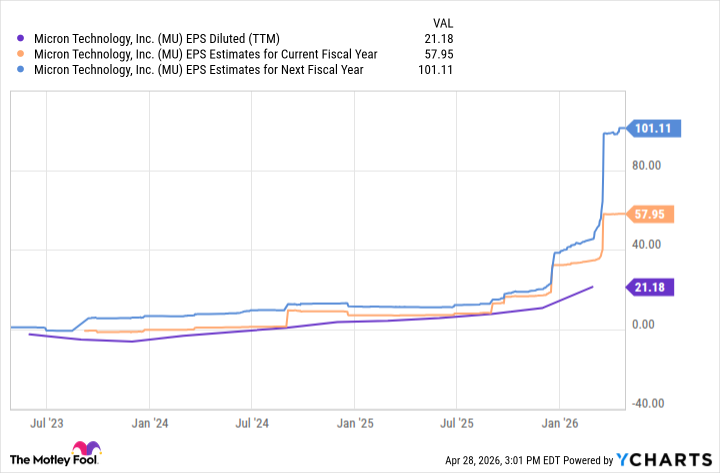

Over the next two years, Wall Street is predicting that Micron's earnings per share (EPS) will rise by nearly fivefold. Right off the bat, this level of growth signals that analysts see the dynamics of AI infrastructure spending as a multiyear catalyst. Furthermore, the pace at which Micron is forecast to expand its bottom line underscores how central memory and storage have become to the future of AI development.

MU EPS Diluted (TTM) data by YCharts.

Currently, Micron trades for about $508 per share while the company's market cap hovers around $574 billion. For it to reach a $1 trillion market cap, the stock would have to rise by roughly 74% to about $871 per share.

Micron trades at a forward price-to-earnings (P/E) ratio of 9. If the company achieves its 2028 estimates above and does not experience any expansion in its forward earnings multiple, Micron's stock would rise to over $900 -- lifting it well above a trillion-dollar market cap.

Here's the big takeaway: As long as Micron hits or lands near that consensus EPS estimate, it could still join the trillion-dollar club even if its forward P/E multiple contracts. So even if investors apply more modest valuation ratios to Micron than they apply to other hypergrowth semiconductor stocks, it still has a great shot of becoming a trillion-dollar company within the next couple of years.