Since March, the conflict in Iran has driven oil prices through the roof, with Brent crude skyrocketing to over $120 per barrel in late April. This surge has propelled oil stocks, including oil and gas giant ExxonMobil (XOM -0.24%), which rose as much as 13% in March alone.

Oil prices have subsided in recent weeks amid a fragile ceasefire, and oil stocks have followed. However, even if the conflict ends soon, there are discussions that reopening the Strait of Hormuz, a critical oil shipping channel for the Middle East, might not be straightforward.

With oil trading around $100 per barrel and ExxonMobil down 12% from its recent high, now might be the time to buy the dip. Here's why.

Image source: Getty Images.

ExxonMobil owns low-cost, high-quality production assets

ExxonMobil is a giant in the oil and gas industry and is the second-largest oil company in the world, trailing only Saudi Aramco. The company operates an integrated business model, meaning it has operations across the oil production chain, including upstream production and downstream refining. This integrated approach provides stability for ExxonMobil amid highly volatile oil and gas prices.

Over the past decade, ExxonMobil has undergone a structural transformation and adopted a strategic, technological, and efficient approach to drilling. A key part of this is Exxon's advantaged assets in the Permian Basin, Guyana, and liquefied natural gas (LNG) that provide it with high-performing, low-cost production assets.

In the Permian, Exxon utilizes a "cube development" approach and proprietary lightweight proppant, which was used in 25% of wells in 2025 and is targeted for 50% of new wells by the end of 2026.

In Guyana, the company is leveraging artificial intelligence (AI) to enable a fully autonomous well section through rig automation and automated downhole steering tools. Over 50% of Exxon's current production comes from assets with a breakeven price below $35 per barrel.

NYSE: XOM

Key Data Points

The Iran conflict has had mixed effects on Exxon's first-quarter results

The conflict in Iran has impacted ExxonMobil, disrupting some shipping routes. Exxon reported a 6% hit to its global oil-equivalent production, and missile strikes in Qatar impacted LNG production lines in which ExxonMobil has an interest.

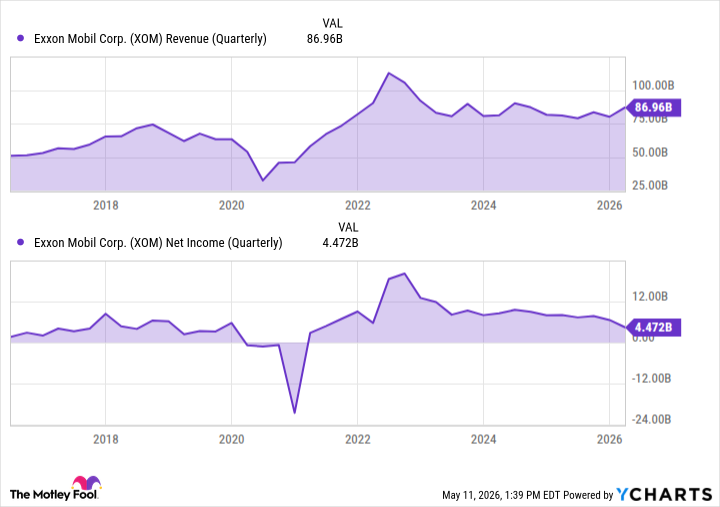

In the first quarter, it saw unfavorable estimated timing effects of $3.9 billion due to the mismatch between the valuation of financial derivatives and physical transactions. As a result, its net income fell to $4.5 billion.

Data by YCharts.

The ongoing conflict in the Middle East is affecting a large portion of its oil production. However, ExxonMobil's global supply chain and focus on advantaged assets position it well to navigate supply disruptions. Its acquisition of Pioneer Natural Resources a couple of years ago added domestic production in the U.S. Permian Basin, where it expects to produce 1.8 million barrels per day, up from 1.4 million barrels per day last year.

ExxonMobil has transformed over the years and has delivered $15.6 billion in cumulative structural cost savings since 2019. Not only that, but the company consistently rewards shareholders, having returned $9.2 billion in the first quarter alone, including $4.3 billion in dividends. Given the ongoing turmoil in the Middle East and oil supply shortages, the recent dip in ExxonMobil looks like a buying opportunity for long-term investors today.