The market seems to be piling into Elon Musk-related entities with enthusiasm. With the SpaceX initial public offering (IPO) imminent, Tesla (TSLA +8.49%) shares had rallied before this week's price drop, hitting a market cap of $1.5 trillion (it has since dropped to $1.25 trillion). SpaceX is reportedly pricing its IPO at a valuation of somewhere between $1.75 trillion and $2 trillion.

That would put Musk's empire at a combined valuation of $3 trillion to $3.5 trillion. However, when looking at the fundamentals of these two businesses, there seems to be much more hope in science fiction projects like the Optimus robots and space data centers, and less actual profit being generated today from these Musk-related businesses.

For this reason, any investor buying into the Musk complex may be setting themselves up for disappointment. Here's one stock I think will be worth more than Tesla and SpaceX combined a year from now that investors should buy instead.

Image source: Getty Images.

Massive cloud growth

While SpaceX and its new artificial intelligence (AI) subsidiary, xAI, have grand plans to build data centers on land and in orbit, Amazon (AMZN +3.23%) is already the largest data center and cloud provider in the world today, with plenty of momentum.

Huge spending plans, contracts for its internal computer chips, and partnerships with the likes of Anthropic are propelling Amazon Web Services (AWS) -- Amazon's cloud division -- to some of its fastest growth in years. Revenue was up 28% year over year last quarter to $37.6 billion, with more growth projected in the quarters ahead.

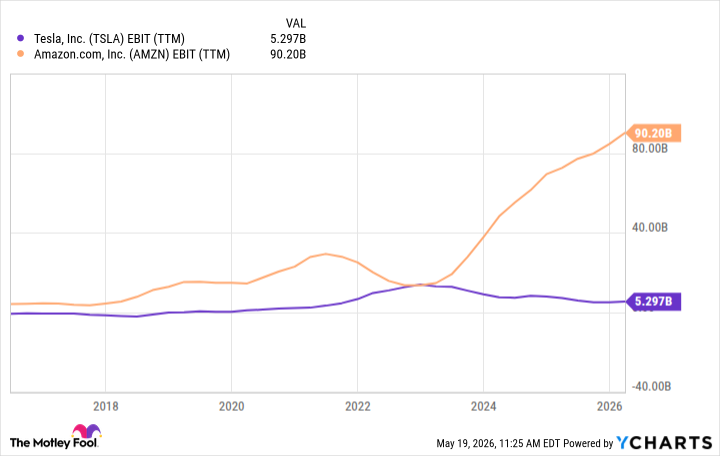

At the same time, AWS' operating margin has remained high at 35% over the last 12 months, with operating income of $48 billion. If revenue grows by 28% again over the next 12 months, operating earnings will reach $61.5 billion. SpaceX and Tesla are nowhere near this level of earnings power, even when combining the two businesses.

NASDAQ: AMZN

Key Data Points

Huge opportunity left in retail

Amazon is not just AWS, either. It has its massive e-commerce division in North America and internationally, along with other bets, such as satellite internet services to rival Starlink, that can provide long-term value to shareholders.

Its North American retail segment and its profit potential are likely to have the largest impact on Amazon's earnings power in the next 12 months. Net sales in Amazon's North American division accelerated to 12% year over year last quarter, one of its highest growth rates in years, indicating it continues to take market share from overall retail spending in the United States and Canada.

Net sales over the last 12 months were $438 billion. Given its investment in rapid delivery and a wide selection for customers, Amazon should continue to grow its North American revenue by about 12% over the next 12 months. That would bring revenue to $491 billion.

The bigger question is where the division's profit margin will be. Operating margin hit a record 7.3% over the last 12 months, a figure that should steadily expand in the years ahead as fast-growing segments like advertising and subscriptions continue to grow. It doesn't take a herculean estimate to peg North American operating margin at 8% 12 months from now, or $39 billion in operating earnings based on my revenue estimates.

Data by YCharts.

Why Amazon is superior to Tesla and SpaceX

Combined, Amazon's cloud division and North American retail may generate roughly $100 billion in earnings a year from now. Add in international retail, and consolidated earnings power should be well above its trailing $90 billion level. Assuming Amazon's earnings multiple stays steady, its market cap should rise from $2.77 trillion today to $3.25 trillion or more in 12 months.

The same attractive proposition cannot be said of Tesla, or any buyer of SpaceX at its reported IPO price of $1.75 trillion. Tesla itself generated just $5.3 billion in operating earnings over the last 12 months and may move further into the red with its ambitious projects in autonomous vehicles and robotics, which have shown little to no financial return so far.

SpaceX's financials are not fully reported today, but revenue of $16 billion was disclosed for 2025. It's unlikely that the combined businesses will even sniff Amazon's $100 billion-plus in operating income over the next 12 months.

The stock may pop on the IPO due to the excitement around space and AI stocks, but SpaceX -- along with Tesla -- is liable to disappoint investors who buy right now. Stick with Amazon instead.