As artificial intelligence has exploded in popularity and use, so has big tech's spending on it. The four major hyperscalers plan to spend hundreds of billions of dollars on data center infrastructure this year, with Amazon (AMZN +0.81%) projecting the largest budget. At the time it delivered its Q4 2025 earnings report in February, it said it anticipated capital expenditures of $200 billion for 2026.

For perspective, fewer than 30 public companies worldwide have generated more than $200 billion in revenue over their past four quarters combined. Less than 60 countries have GDPs of over $200 billion. So, with Amazon planning historic AI capex, should investors be worried? Wall Street seems to be conflicted on the issue.

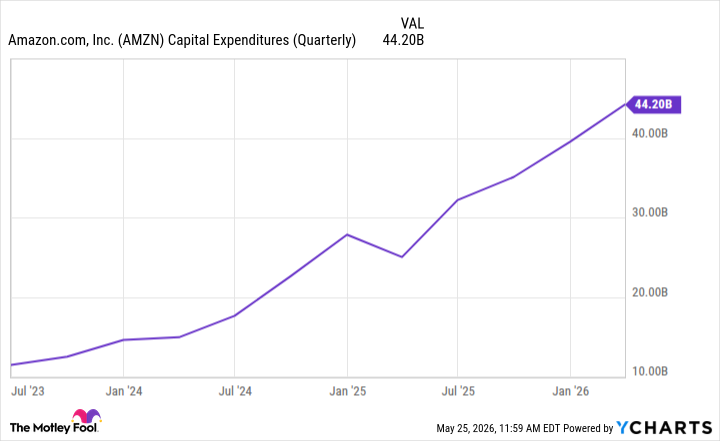

Image source: The Motley Fool.

Where is the money going?

Not all of that $200 billion will go toward AI (Amazon still needs to invest more in its warehouse robots and other e-commerce logistics, for example), but most of it will surely go toward building data centers and other AI infrastructure, such as its in-house AI chips.

Most people know (and care) about AI and the cloud only as far as they interact with them. However, behind the scenes, tons of physical hardware, real estate, and power sources must be in place for it to work. That's why many companies that make hardware for data centers have also seen unprecedented success recently (Nvidia, Sandisk, etc.).

Amazon didn't say how much of the $200 billion will go directly toward AI initiatives, but I wouldn't be surprised if it's at least three-fourths of it.

AMZN Capital Expenditures (Quarterly) data by YCharts.

What does Wall Street think of Amazon's spending plan?

Investors have noticeably advanced from the hype phase of the AI investment cycle to the "show me this can make money" phase.

Those who are bullish about Amazon's spending plan point to the size of AWS' current backlog -- $364 billion at the end of the first quarter, and that didn't include the over $100 billion deal it announced with Anthropic in late April. The growth of that backlog shows that rising demand for cloud services is outpacing what Amazon can reasonably take on right now.

NASDAQ: AMZN

Key Data Points

Those who are bearish (or at least more cautious) on the massive spending plan point to how much it will reduce Amazon's short-term free cash flow and to the lack of an end goal in sight. Both are fair worries, especially the latter. Nobody questions whether Amazon can afford this spending (it generates more revenue than any public company in the world), but data center hardware must be steadily replaced as older chips reach the end of their useful lives and as the state of the art continuously improves. This could potentially put Amazon in a situation where high levels of capex spending must be maintained indefinitely.

Amazon is spending a lot, yes, but I'm more on the side of this being worthwhile spending. Considering the current size of its backlog and its growth rate, Amazon must expand its data center capabilities. If it doesn't, the result could be AWS customers jumping ship to other platforms such as Microsoft Azure or Google Cloud.

Even if we consider it overspending, in this case, I think it's much better to overspend and be overprepared than to underspend and be underprepared.