Target (TGT +1.78%) just reaffirmed its commitment to its long-standing dividend by approving the 55th consecutive annual increase. Thanks to the 1.8% hike in the payout, its dividend is now $4.64 per share annually.

That dividend increase also amounts to its smallest hike in 55 years, which may disappoint some investors. However, other investors who take a closer look at the company's condition may perceive it as one of the top Dividend King stocks to buy in June. Here's why.

Image source: The Motley Fool.

Target and its Dividend King status

Admittedly, Target has struggled in recent years, particularly when compared to rivals such as Walmart and Costco. Challenges such as high inventories, a less desirable product mix, messy stores, and controversial political stances have contributed to declining sales and a falling stock price.

When former Chief Operating Officer Michael Fiddelke became CEO in February, he changed direction by pledging to invest $5 billion to upgrade stores, improve its technology, and change its product mix.

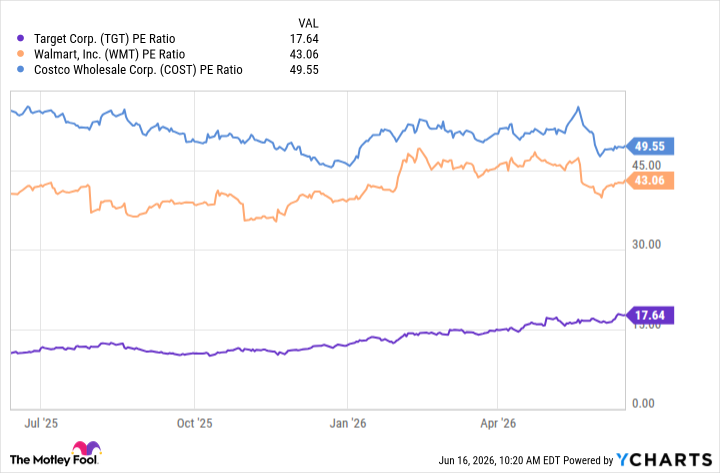

On some levels, Target stock may have been waiting for a catalyst. The aforementioned dividend offers a yield of 3.4%, far above the 1% average of the S&P 500. Also, its P/E ratio of almost 18 appears modest compared to Walmart and Costco, which each sell for well above 40 times earnings.

TGT PE Ratio data by YCharts

Now, with its earnings for the first quarter of fiscal 2026 (ended May 2), Target just gave its investors some great news.

Net sales surged by almost 7%, a stark contrast to the 2% pullback in sales levels during fiscal 2025. The fiscal Q1 profit of $781 million was down 25%, but that occurred as investments in the company led to a 21% increase in selling, general, and administrative expenses.

Additionally, those higher costs may help explain the more modest 1.8% dividend hike. In fiscal Q1, negative free cash flow was $319 million, a concerning development since dividend expenses for the quarter were $516 million.

Still, investors should remember that Target holds $3.5 billion in liquidity, meaning it can cover these dividend payments in the near term. Moreover, free cash flow was $2.8 billion in fiscal 2025, and that covered the nearly $2.1 billion cost of the dividend during that period.

Furthermore, abandoning a 55-year streak of payout hikes would cost Target its Dividend King status, as Dividend Kings are companies that have annually raised their payouts consistently for at least 50 years. That would likely damage its reputation, making a dividend cut highly unlikely, though given the investments Target needs to make, it could mean payout hikes remain modest for now.

Target as a top dividend stock

Despite Target's struggles and modest dividend increases, it looks like a buy in June.

Indeed, Target stock has struggled in recent years, primarily because of the company's missteps.

Fortunately, sales have recovered, and the new CEO has worked to get the company back on track. Considering the need for Target to invest in itself, investors are more likely to accept modest payout hikes and even negative free cash flows if that gets the company back on track in the long term. Furthermore, the fact that its stock sells at a considerable discount to Walmart's and Costco's earnings multiples only bolsters the buy case.

Ultimately, since Target is unlikely to abandon its Dividend King status, its high-yielding, rising dividend should continue to help drive investor returns.