Nvidia (NVDA -1.56%) is the world's largest company by market cap, and many investors are a bit worried that its stock may have reached a point where it can't grow fast for much longer. I think that's just not true, and expect that several tailwinds will push the stock to new heights over the next few years.

The biggest of those tailwinds is the tech sector's soaring spending on the data center build-out. If this trend keeps up as Nvidia projects, then it should be a great stock to own in the coming years.

Image source: Getty Images.

Nvidia isn't alone in its projections

On multiple occasions, Nvidia has made the bold assertion that global data center capital expenditures will reach $3 trillion to $4 trillion annually by 2030. For reference, the big four AI hyperscalers plan to spend around $650 billion on capex this year. That total doesn't include companies like OpenAI, Anthropic, xAI, or anything in China. So, the figure for the data center sector as a whole is likely several hundred billion dollars more. Next year, Nvidia expects the hyperscalers to spend around $1 trillion. It likely already has many of the orders for the AI processors they want on hand, giving it a privileged degree of insight into the pace of the growth trend.

Additionally, suppliers like Taiwan Semiconductor Manufacturing have already told investors to expect major growth for several more years, which is why they are spending big on increasing their production capabilities this year. One of the AI hyperscalers, Alphabet, told investors during its Q1 conference call that they should expect "significantly" higher capital expenditures in 2027 than the $180 billion to $190 billion it plans to spend in 2026.

NASDAQ: NVDA

Key Data Points

There simply isn't enough AI computing power to meet demand, and with everyone in the AI industry convinced that more computing power will solve problems, spending will trend that way, benefiting Nvidia. But just how much can Nvidia's stock rise by 2030?

Nvidia has major upside potential

For simplicity's sake, let's assume that 2026's total data center expenditures globally will total $900 billion. That means that spending will increase by about fourfold in 2030. But how much of that growth will Nvidia capture?

There are two trends, each pulling in a different direction. One that is pulling in Nvidia's favor is that data centers are being built all across the world. Right now, that includes a lot of land costs, permitting, infrastructure, and other things necessary to get a data center operational. However, a significant number of the chips that will eventually go into these facilities haven't been purchased yet. So, it's safe to assume that as we get closer to 2030, a larger slice of the capex pie will be devoted to chips.

On the flip side, many companies are starting to develop custom AI chips so that they don't have to rely so heavily on Nvidia's products. While the hyperscalers will never completely get away from Nvidia's powerful general-purpose GPUs, the application-specific integrated circuits they are designing can provide significant cost-performance benefits when deployed for the narrow AI workloads they are optimized to handle.

As a result, in the future, custom chips are likely to account for a growing percentage of the AI data center processors being sold. So Nvidia's market share will shrink.

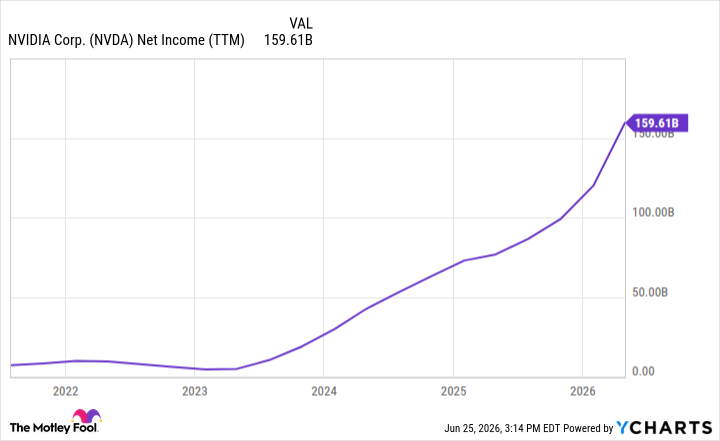

NVDA Net Income (TTM) data by YCharts.

Overall, I expect these two countervailing trends to nearly cancel each other out. If that proves to be the case, Nvidia should be able to increase its revenue and earnings fourfold between now and 2030. If Nvidia's earnings quadruple and it trades at that time at 20 times earnings (a pretty cheap valuation), that would give the company a $12.8 trillion market cap. That would be a 172% gain from today's stock price to about $530 per share.

Normally, to beat the market, a stock would have to double in less than seven years. Based on these premises, Nvidia could do that easily, making it a no-brainer stock to buy.