After years of decline, Intel (INTC -5.53%) appears to be on track for a dramatic comeback. Under the leadership of Lip-Bu Tan, investors are becoming increasingly confident that Intel can remain a player in the semiconductor industry.

Nonetheless, Intel stock has risen by about 425% over the past year, taking its stock price and valuation to elevated levels. Thus, the question for investors is whether that stock price growth will undermine the chip stock's performance over the next five years.

Image source: The Motley Fool.

The Intel comeback

Without question, Intel had been on the decline since the early part of the last decade. Innovation began to slow after the retirement and passing of its founders. That created openings for its longtime rival Advanced Micro Devices to overtake it technically and for Taiwan Semiconductor Manufacturing (TSMC) to surpass it as a manufacturer.

Moreover, even when the previous CEO Pat Gelsinger attempted to make it a market leader in central processing units (CPUs) and third-party manufacturing, Nvidia's development of AI accelerators appeared to push it further behind.

Fortunately, Tan, the CEO who transformed Cadence Design Systems, appears poised to make Intel more competitive. As previously mentioned, Intel has mastered the 18A manufacturing process, which can produce chips as small as 1.8 nanometers (nms), allowing it to pioneer next-generation AI processors.

With that, he has begun to transform Intel into a company that could compete in manufacturing with TSMC on some levels, helping to reassert America's relevance in chip manufacturing.

Additionally, CPUs have become increasingly critical in data centers for managing workflows for CPUs. With Tan revamping Intel's business, this development bodes well for the company, particularly since Grand View Research projects a compound annual growth rate (CAGR) of 29% for the AI chip market through 2030.

NASDAQ: INTC

Key Data Points

Intel by the numbers

Unfortunately, even after Intel's massive AI rally, the aforementioned stock gains appear largely based on speculation. Its $13.6 billion in revenue for the first quarter of 2026 was up 7% year over year. That improved over the 4% revenue decline in 2025 but is a far cry from the massive revenue growth of Nvidia and TSMC.

Moreover, its $3.7 billion net loss in Q1 follows its $0.6 billion net loss in 2025. Also, even though growth should improve, analysts forecast 11% revenue growth in 2026, with only a marginal improvement projected in 2027. Thus, it will likely take years to match the growth rate of competitors, if it gets there at all.

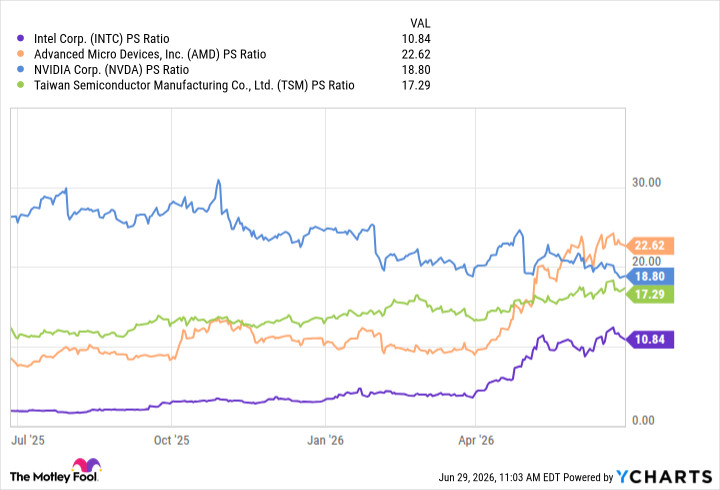

Furthermore, Intel has no price-to-earnings (P/E) ratio on a GAAP basis. Still, even after its considerable stock gains, Intel's 11 price-to-sales (P/S) ratio lags its largest competitors. That indicates that investors should probably not sell Intel stock on valuation concerns.

INTC PS Ratio data by YCharts.

Still, as previously mentioned, much of the stock gains are likely tied to speculation. Hence, with Intel's comparatively modest revenue growth, the lower sales multiple does not necessarily reflect a discount when considering its peers' revenue growth.

Intel in five years

Ultimately, it is probably too early to tell where Intel will be over the next five years, but I think the stock will outperform the market over that time frame.

Admittedly, five-year projections on stock prices are speculative by their nature. This is especially true for Intel, since the recent financials and near-term projections point to considerably more modest growth than its nearest competitors are likely to report.

Nonetheless, Tan has earned a reputation for orchestrating turnarounds in his industry, and the breakthrough with the 18A process technology confirms that success. That advancement also serves as a tangible indication that Intel can better compete with AMD in the CPU market and with TSMC in manufacturing. That means investors should expect accelerated revenue growth if Grand View's projected CAGR is any indication.

When it comes to individual investors, Intel probably remains too speculative for the risk-averse. However, with an appetite for risk, one has an excellent chance of outperforming the market with Intel stock over the next five years despite the recent run-up in the stock price.