Stellantis (STLA -3.92%) stock is down a staggering 70% over the past three years due to a plethora of problems spanning the globe.

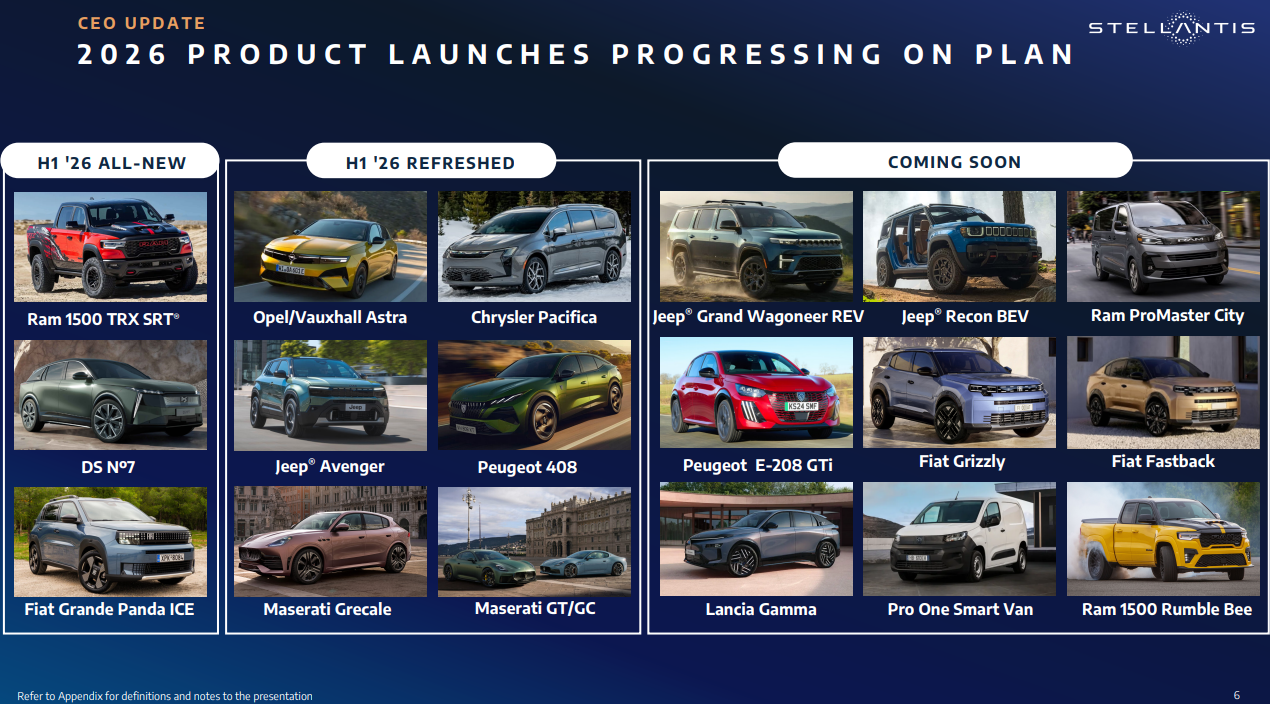

The beleaguered automaker has a $70 billion turnaround strategy it is calling "FaSTLAne 2030." Stellantis will focus on launching 60 new vehicles by 2030, aggressively cutting costs, and funneling 70% of its product investment into four primary global brands: Jeep, Ram, Peugeot, and Fiat. This focus on core brands, increased investment in core brands, and a slowdown in electric vehicle (EV) strategies will finally give the automaker an identity it has sorely lacked.

Stellantis' stock could certainly pop in the near term if this turnaround gains traction, but investors need to keep an eye on a near-term issue that could hinder margins.

Image source: Stellantis.

Shipments vs. sales

The different levels within the automotive industry can be a little tricky with wording, so let's sort that out. Shipments are not the same as sales. Rather, shipments count the vehicles delivered to dealers and distribution companies, while sales track the number of vehicles actually purchased by end consumers.

Stellantis' second-quarter 2026 results give us a prime example of why the distinction between shipments and sales matters. Stellantis' global shipments increased by 10% year over year during the second quarter to 1.6 million. That increase was driven in large part by a 38% surge right here in North America.

In contrast, Stellantis' North American sales rose only 5.7% during the second quarter, well below the 38% surge in shipments to dealers. This suggests a buildup of inventory on dealership lots.

In fact, according to recent data from Cox Automotive, core Stellantis brands Dodge, Jeep, and Ram all have over 140 days' supply of product in North America. That's a concerning inventory glut, given that the historical "healthy" level is around 60 days and the industry average is around 76 days.

Things to consider when it comes to Stellantis

Automakers typically have planned summer downtime to adjust manufacturing lines, among other things, and Stellantis defends its inventory as "stocking up" product ahead of those shutdowns. Despite that reasoning, the inventory glut is potentially problematic for one reason: The oversupply is expected to result in much higher consumer incentives and discounts to help push products off dealer lots and make room for newer models. Newer models are also important because fresh product simply sells faster and requires fewer margin-eroding incentives to do so -- which is why automakers and dealerships need to find an inventory equilibrium to optimize margins and sell rates.

NYSE: STLA

Key Data Points

What it all means

Stellantis offers investors an intriguing opportunity through 2030, when its stock could easily beat broader market returns, simply because it's been sold off so deeply over the past three years. If Stellantis' turnaround drives new, compelling, and more profitable vehicle options, the last thing the company wants is to have 140 days' supply of older models to clear the way.

Stellantis shares are poised to pop with its turnaround strategy, but investors should hope the inventory glut drops before the turnaround gains traction.