For the second year in a row, with one stroke of the pen, BreitBurn Energy Partners (BBEP +0.00%) blew past its annual acquisition target by announcing a big oil deal. This time, however, the company didn't just purchase one big asset, instead it announced this morning that it is buying the entirety of fellow upstream MLP QR Energy (NYSE: QRE) in a $3 billion deal. The deal is coming at a 19% premium to QR Energy's previous closing price.

Drilling down into the deal

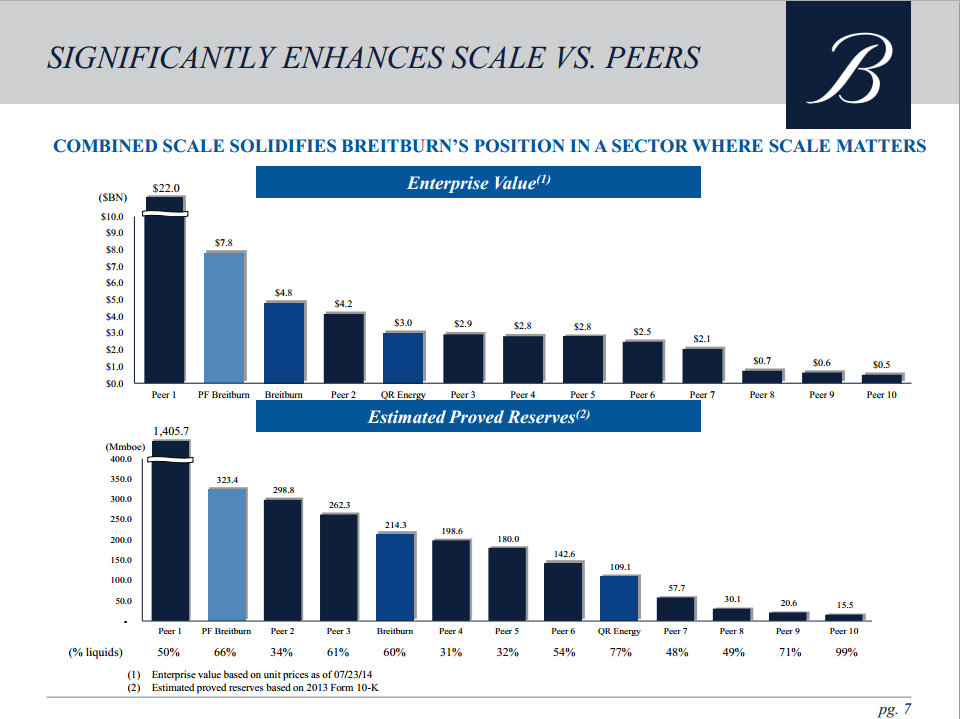

The unit-for-unit transaction will create the largest oil-weighted upstream MLP as the combined company will have an enterprise value of $7.8 billion. Further, the combined entity will have average daily production of 57,300 barrels of oil per day with reserves 67% weighted toward liquids.

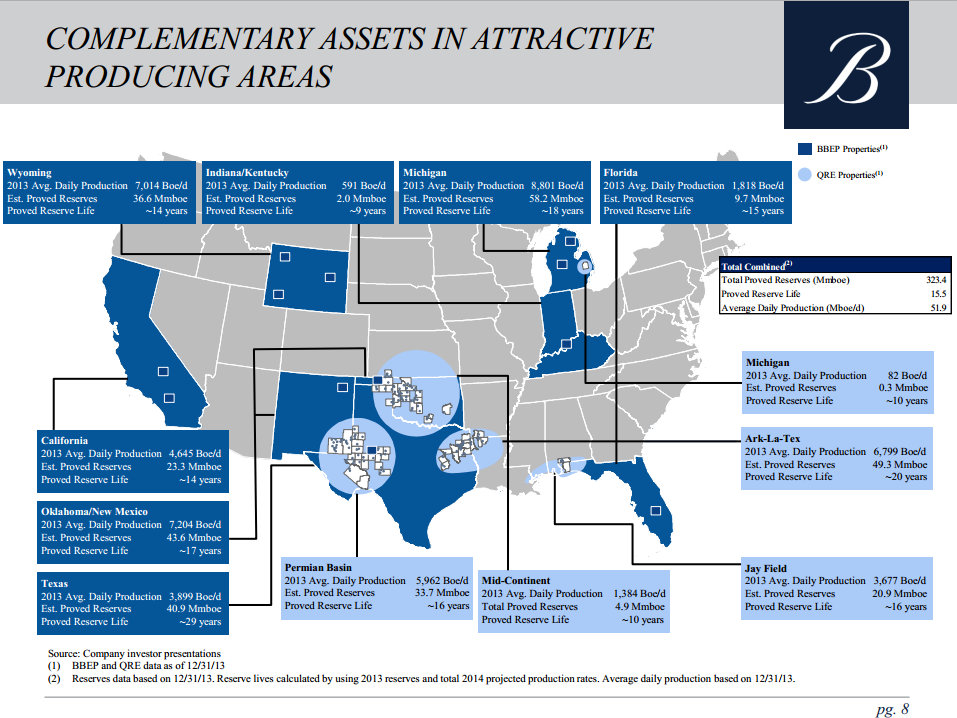

As the map on the following slide points out, the combination of BreitBurn Energy Partners and QR Energy is a highly complementary pairing.

As noted on that map, QR Energy adds overlapping assets in the Permian Basin and Michigan while extending BreitBurn Energy Partners' reach into the Mid-Continent and Ark-La-Tex region. Further, it adds the Jay Field along the Gulf Coast.

Because of the overlap, BreitBurn Energy Partners sees the deal immediately saving the combined company $13 million per year from synergies. Further, the company sees future upside from operational efficiencies, portfolio optimization, and cost of capital reduction.

These synergies, along with the accretive nature of the transaction, will provide an immediate boost to investors. BreitBurn Energy Partners plans to increase its distribution by $0.07 per share, or 3.5% upon closing. That boost also represents a 5% increase for QR Energy investors.

Getting bigger and better in one deal

The other really important aspect of this deal is that it solidifies BreitBurn Energy Partners' place as the second largest upstream MLP. That increased scale will enable it to better compete for deals in the future as it should lower the company's cost of capital while providing it with the scale it needs to be in the position to acquire larger asset packages.

Further, BreitBurn Energy Partners is adding scale where scale matters. It's becoming a much larger oil producer as QR Energy is among the most levered MLPs in the space, as noted on the following slide.

Source: BreitBurn Energy Partners Investor Presentation.

As the chart on the bottom of that slide notes, 67% of the reserves of the pro forma company will be in higher valued liquids. That's a meaningful boost from the 60% liquids weighting of reserves that BreitBurn Energy Partners had before the deal. Further, these reserves are heavily weighted toward oil as 58% of the reserves are oil and just 8% are natural gas liquids, compared to 53% oil for BreitBurn Energy Partners as a stand-alone entity. That oil weighting is a big deal given that NGLs are tough to hedge, which adds volatility to the cash flow stream, while natural gas isn't as valuable these days.

Investor takeaway

This really is a transformative acquisition for BreitBurn Energy Partners. The company is shifting its reserve mix further toward oil and is expanding its geographic reach, both of which should improve its cost of capital. That should make it even easier for the combined entity to grow in the future. Further, the deal boosts the company's cash distribution to investors while strengthening its ability to keep that payout both flowing and growing in the years ahead.