Annaly Capital Management's (NLY +0.29%) eye-popping 10.4% dividend yield is unquestionably attractive, but it's important to remember that a dividend is only as strong as the company supporting it.

That's why I dug into what factors are driving Annaly forward to find three of the best reasons to buy this high-yield stock.

3. Management

Mortgage real estate investment trust, or mREITs, are managed portfolios of debt. Because debt is far from exclusive to Annaly -- or any other company, for that matter -- who is managing that portfolio should be among your chief concerns.

I have had my issues with Annaly's management in the past, namely the exorbitant $35 million followed by $25.8 million in compensation CEO Wellington Denahan received in 2011 and 2012, a salary that 72% of shareholders took issue with. Annaly's response to investor concern was to externalize management.

The change has not significantly affected operations, but did change transparency and management incentives. For instance, management no longer has to disclose executive compensation, and instead of being paid for performance, management receives a flat 1.05% of shareholder equity. This means if management want to up their pay, all they need to do is issue new shares of stock.

However, none of my major concerns have come to fruition. While Annaly's management could sell new shares and increase their compensation, they haven't. In fact, over the first nine months in 2014, average total diluted shares outstanding are down 4.8% compared to the same time in 2013. Moreover, I would argue that performance-based compensation could encourage excessive risk taking, while earnings a flat fee incentivizes a more balance approach.

Lastly, and most importantly, whether or not you agree with how management is compensated, it is hard to argue with results. Since around 1997 Annaly has navigated through a number of difficult environments, and, according to Denahan, created a total return for shareholders "three times that of the S&P 500." Ultimately, investing with a management team that has proven its versatility is a big advantage.

2. Commercial real estate

Another one of management's highly criticized decisions was its move into commercial real estate with its acquisition of CreXus in January of 2013, an issue that has become more topical following its acquisition of 11 grocery-anchored shopping centers earlier this month.

The chief concern is that commercial real estate and debt is exposed to credit risk, while Annaly's bread and butter investment, residential mortgage-backed securities, is guaranteed against loss of principal. The company's strict focus on residential mortgages has served it well in the past, but I'm firmly of the opinion that diversifying efforts will make Annaly a more stable business in the long-term.

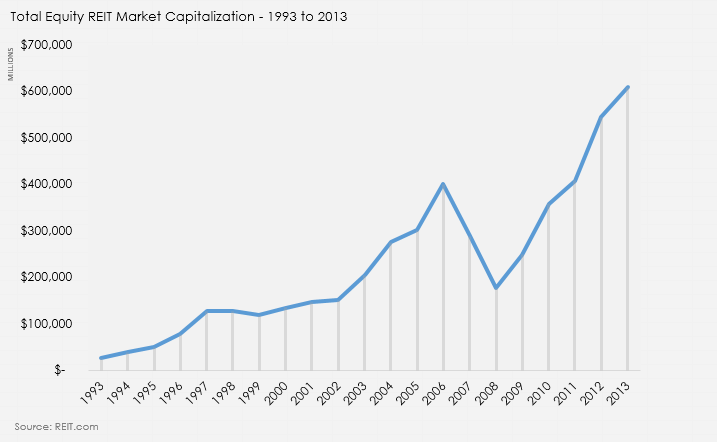

As shown in the chart above, equity REITs -- companies that invest in physical properties -- have been consistently strong over the past decade. In fact, despite the financial crisis from 2007 to 2009, equity REITs' collective market cap is up more than 2200% since 1993.

Also, Annaly's commercial investments can earn yields of over 9%, three times the yield on residential mortgages. Lastly, Annaly will keep commercial investments to 25% of equity or less. This gives Annaly the ability to seize new opportunities without straying away from what it does best.

1. A need for private capital

The best long-term investments are in companies that fill a void; and up until recently I was not sure how Annaly fit into the larger picture. But that has changed.

In a roundtable discussion conducted by Andrew Davidson & Co. in 2012, it was suggested that "There are currently about $10 trillion dollars of mortgages outstanding. Fannie Mae and Freddie Mac currently bear the credit risk of almost 50% of those loans."

As government sponsored entities, GSEs, taxpayers are on the hook for significant credit losses taken by Fannie Mae and Freddie Mac. For that reason, the FHFA has made it a top priority to "reduce taxpayer risk by increasing the role of private capital in the mortgage market."

Unfortunately, the original credit-risk sharing deals designed to solve this problem were not direct investments in real estate, and therefore not a good fit for Annaly. But according to Annaly's head of agency portfolio David Finkelstein, this is changing, and "now it's on the radar."

Moreover, Annaly's president, Kevin Keyes, noted that "[W]hen you see the latest risk sharing deals that are getting done... we just think that it's going to grow and... I think there is a big opportunity for us in our industry."

Also, through the Federal Reserve's massive bond buying program (quantitative easing), the Federal Reserve is currently holding $1.7 trillion in mortgage-backed securities. This creates two separate, and yet equally massive, forces with the same need. Whether it is Fannie Mae and Freddie Mac looking to reduce credit risk, or the eventual shrinking of the Federal Reserve's balance sheet, there will be a long-term need for private capital, like Annaly, to fill the void.